DeFi

11 min read

Key Takeaways

Hyperliquid leads at 67/80 under our institutionally-weighted scorecard, reflecting dominance in volume, ecosystem breadth, and builder adoption, while October 10 exposed concrete limits: $2.1B closed via ADL in 12 minutes, ~50% OI loss in subsequent weeks, and the first full exhaustion of the three-tier liquidation waterfall in production.

Paradex (57/80) is the only production venue with architectural position confidentiality, combining zero-fee execution, RPI price improvement (28-61% tighter spreads), and Ethereum settlement via STARK proofs. But 0.99% market share and -78.48% 7d volume decline during its incentive transition highlight the gap between architectural quality and current adoption.

Capital stickiness separates real positioning from incentive churn. OI-to-30d-Volume ratios reveal a tiered market: Hyperliquid (0.021) leads by a wide margin, Paradex and Variational (both 0.014) form a second tier, while the bottom four cluster at 0.005-0.007.

Fee-adjusted execution cost reshuffles the rankings. When trading fees are included in total cost for a $100K BTC order, zero-fee venues move from mid-tier on raw spreads to top-three on total cost, while sub-basis-point spread venues charging 4.5+ bps become the most expensive.

Privacy is emerging as the institutional unlock. Dark pools handle 40-50% of U.S. equity volume; onchain equivalents must exist for institutional adoption to scale. Paradex, GRVT, and EdgeX are the venues where liquidation hunting is structurally impossible, with Paradex leading the charge in terms of tech-level implementation of a comprehensive privacy system.

The programmability spectrum carries long-term defensibility implications. Hyperliquid's builder ecosystem at this point routes 40%+ of DAU through third-party frontends with $31M+ in captured fees; while most competitors have no programmability layer at all.

No platform has all four main requirements today (extensible infrastructure, position confidentiality, execution quality, and sustainable economics), but the direction of convergence is clear.

Executive Summary

In 2024, onchain perpetual futures were a niche experiment processing roughly $1.5 trillion in annual volume. Twelve months later, they had become a $7.9 trillion market, a 427% expansion that compressed what might have been a decade of infrastructure maturation into a single calendar year. By late 2025, monthly volumes were consistently exceeding $1 trillion, with DEX-to-CEX perpetual volume share reaching 15-20% in peak months. The question confronting institutional capital is no longer whether onchain derivatives matter. It is which infrastructure will absorb the next wave of allocation.

This report provides an institutional-grade comparative analysis of the eight most architecturally significant perpetual DEX platforms: Hyperliquid, Paradex, Lighter, EdgeX, Extended, GRVT, Variational, and Aster. We evaluate technical architecture, market microstructure, fee economics, funding mechanics, liquidation design, privacy infrastructure, programmability, product breadth, and adoption data as of February 2026.

The central thesis: raw volume is a lagging indicator of infrastructure quality. Total execution cost, funding rate divergence, capital stickiness, position confidentiality, and ecosystem composability are the dimensions that will determine which venues capture institutional flow over the next 12 to 24 months.

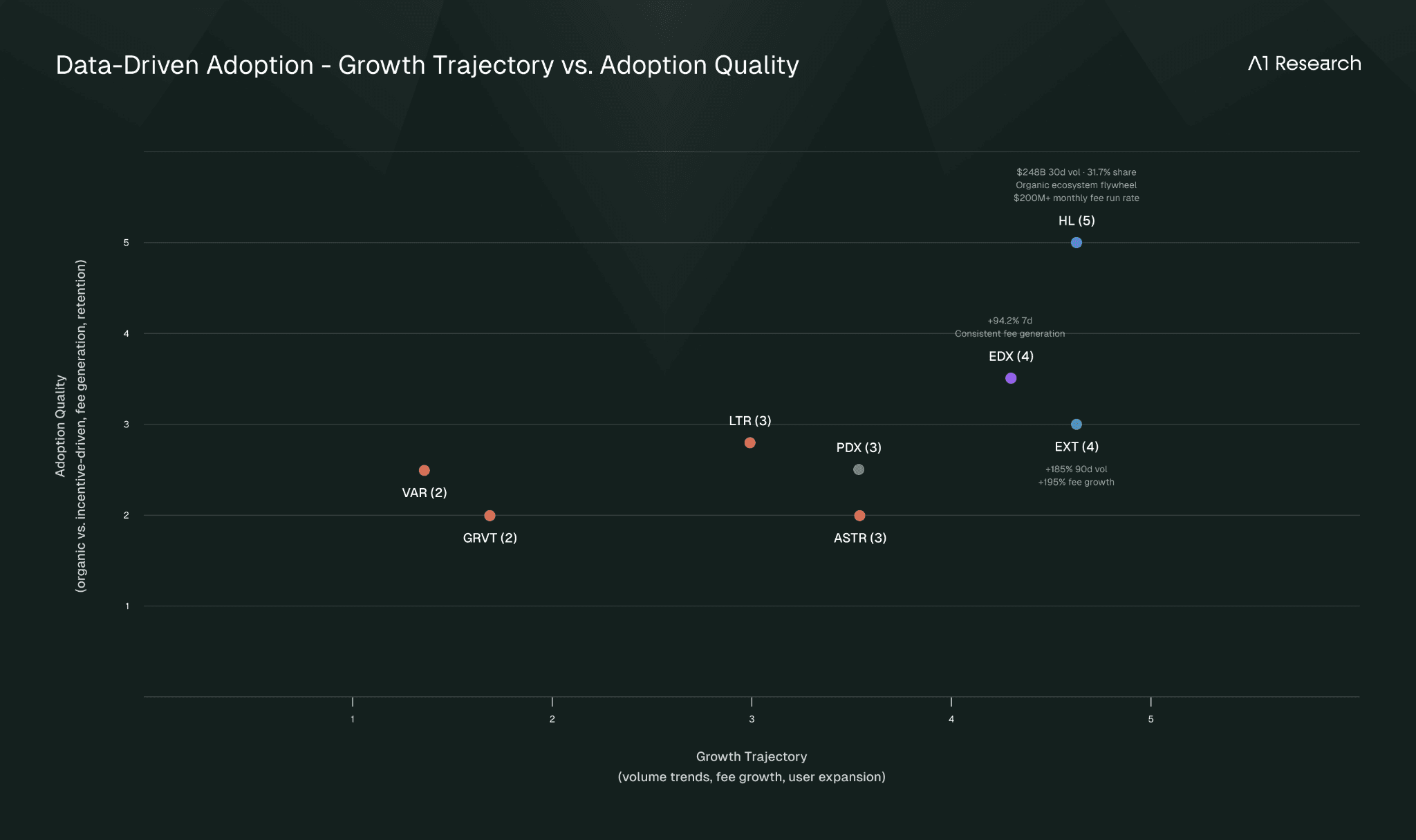

Key findings: Hyperliquid dominates at $248B in 30-day volume (31.7% share) but has compressed from roughly 80% peak share in mid-2025, reflecting rapid competitive fragmentation rather than decline as its absolute volume continues to grow. Capital stickiness analysis using OI-to-30d-Volume ratios reveals a tiered market: Hyperliquid (0.021) demonstrates the highest position retention by a wide margin, with Paradex and Variational (both 0.014) forming a second tier alongside Aster (0.013), while the remaining platforms cluster between 0.005 and 0.007, suggesting genuine institutional position-holding at the top versus incentive-driven churn at the bottom. Fee-adjusted analysis from our prior proprietary orderbook study shows zero-fee venues rank materially higher than raw spread metrics suggest. The programmability spectrum, from Hyperliquid's builder ecosystem routing over 40% of daily active users through third-party frontends to entirely closed architectures, carries significant implications for long-term defensibility. Privacy infrastructure is emerging as a critical institutional differentiator, with Paradex currently the only production venue offering comprehensive position confidentiality, while GRVT's zkSync appchain Validium architecture and EdgeX's StarkEx deployment provide meaningful but operator-dependent privacy as a structural byproduct. And the October 10, 2025 crash, which liquidated $19.1 billion across 1.6 million traders in a single day, stress-tested every architectural assumption in this report, producing sharply divergent outcomes across platforms and exposing fundamental design trade-offs that were previously theoretical.

Methodology

Data in this report reflects a snapshot taken on February 6, 2026. Volume and open interest figures are sourced from DefiLlama, which aggregates self-reported and on-chain data with known limitations around wash trading and incentive-driven activity. The scorecard in Section 9 uses institutionally-weighted scoring across eight dimensions, with three tiers of weighting (×3 for non-negotiable infrastructure, ×2 for core differentiators, ×1 for long-term considerations), scoring production capabilities only with no credit for roadmap items. Fee-adjusted execution cost analysis references our prior A1 Research orderbook study, which used 328 independent snapshots across seven platforms over January 13-16, 2026.

1. The $7.9 Trillion Inflection Point

To appreciate the velocity of what happened in 2025, we have to consider the trajectory. In Q1, onchain perpetual DEX volumes were running at roughly $500-600 billion per quarter, meaningful but still a rounding error against Binance's perpetual volumes alone. By Q3, monthly volumes were clearing $300 billion. By Q4, they were consistently above $1 trillion per month, driven not by a single platform's dominance but by the simultaneous maturation of multiple competing architectures.

Several macro forces converged to produce this inflection. The institutional trauma of FTX's collapse continued reverberating through capital allocation decisions, transforming self-custodial execution from an ideological preference into a fiduciary requirement for an increasing share of professional allocators. L2 scaling solutions matured to the point where onchain execution could credibly compete with centralized venues on latency and throughput: Hyperliquid's sub-200ms median finality and 200,000 orders per second demonstrated that the performance gap had effectively closed. Meanwhile, a wave of new entrants, each staking a claim on a different architectural philosophy, expanded the design space in ways that made the market competitive rather than monopolistic.

The result was fragmentation, and it was healthy fragmentation. Hyperliquid's market share compressed from approximately 80% in May 2025 to roughly 31% by February 2026. But this compression masked an important structural reality: Hyperliquid's absolute volume continued to grow throughout. What changed was that aggregate market growth, driven by Lighter, EdgeX, Extended, Aster, and others, outpaced any single platform's capture rate. The perp DEX market had entered a multi-venue era, and the institutional question shifted accordingly: not whether to access onchain derivatives, but which infrastructure to build on and route through.

The addressable opportunity demands realistic framing. Global asset managers control approximately $128 trillion in AUM as of 2024, per BCG's Global Asset Management Report. Even a conservative 0.1% allocation to onchain derivatives over the next three to five years, our own illustrative estimate rather than a BCG projection, would represent $120 billion in potential flow, dwarfing the current onchain infrastructure that processes $50-100 billion monthly across all venues. Pension funds, sovereign wealth allocators, and family offices are beginning to explore tokenized exposure not because they are crypto-native, but because the cost structure of traditional derivatives intermediation, from clearing fees and margin inefficiencies to settlement lag and counterparty risk capital charges, creates a genuine economic incentive to consider alternatives. The platforms that capture this capital will not be those with the highest volume today, but those that best resolve the trade-offs between execution quality, position confidentiality, and ecosystem composability.

The Eight Contenders

This analysis covers eight platforms selected for meaningful volume, differentiated architecture, and institutional relevance:

Hyperliquid operates a custom L1 with HyperBFT consensus, a fully onchain orderbook, and the most developed builder ecosystem in the space. Paradex runs a private Starknet appchain settling to Ethereum, the only production perp DEX with comprehensive position confidentiality, a zero-fee model with Retail Price Improvement (RPI), and future Paradigm integration. Lighter is a ZK-Rollup on Ethereum with zero retail fees, the fastest asset catalog expansion (500+ markets), and the most aggressive RWA push via Chainlink integration. EdgeX is a StarkEx-based Validium transitioning to a modular multi-VM architecture (V2), with strong fee revenue relative to peers and inherent position privacy via off-chain data availability. Extended builds on Starknet with a unique vision: embedding unified margin logic at the base layer as a network-level primitive. GRVT is a sovereign, ZK-powered appchain built on zkSync’s ZK Stack, operating in Validium mode within the ZKsync Elastic Network and settling to Ethereum L1, with a focus on institutional readiness. Variational deploys on Arbitrum with an RFQ (Request-for-Quote) model, the structural outlier in a CLOB-dominated field, featuring zero trading fees and a Robinhood-style spread capture model. Aster takes a multi-chain deposit contract approach (BNB Chain primary, plus Arbitrum, Ethereum, Solana) with off-chain orderbook logic and broad asset coverage including tokenized stocks. Aster was temporarily delisted from DefiLlama for wash trading concerns; while now reinstated, its reported metrics might warrant additional scrutiny.

2. Technical Architecture: Six Philosophies, One Market

The technical architecture of a perp DEX is not a backend implementation detail. It is the upstream decision that constrains and enables everything downstream: what privacy guarantees are possible, how fast execution can be, what products can be built on top, whether third-party developers can compose with the exchange, and how decentralized the system can ultimately become. These eight platforms represent six fundamentally different approaches to resolving the core tension between performance, security, and composability.

Custom L1 (Hyperliquid). The most vertically integrated approach in the cohort. Hyperliquid controls the consensus layer, execution layer, and application layer within a single system, running HyperBFT, a custom consensus algorithm inspired by HotStuff that achieves median end-to-end latency of approximately 200 milliseconds and 99th percentile latency under 0.9 seconds. The system processes up to 200,000 orders per second, benchmarked performance that places it in the same operational class as major centralized exchanges. The fully onchain orderbook means matching, margining, and liquidation all occur within consensus itself, with every trade finalized on-chain in a single block. The dual-layer architecture (HyperCore for the high-performance orderbook plus HyperEVM for general-purpose smart contract composability) introduces complexity but enables the platform to function simultaneously as a trading venue and a programmable financial stack. The trade-off is well-defined: Hyperliquid's validator set, while expanding, remains concentrated, and the custom L1 offers no Ethereum settlement fallback, meaning ultimate recourse in a catastrophic failure scenario depends entirely on the integrity of Hyperliquid's own consensus rather than Ethereum's security.

Private Starknet Appchain (Paradex). Architecturally distinct from both custom L1 and shared rollup deployments. The appchain model provides Paradex with dedicated block space, custom derivatives-optimized transaction types, and full sequencer control, and critically, this sequencer control enables privacy features that would be architecturally impossible on a transparent shared rollup. State diffs post as encrypted blobs on Ethereum L1 via EIP-4844, account data is RPC-masked on L2, and order flow processes entirely off-chain. The result is a system where positions, liquidation levels, and trading activity are not visible to external observers, while still inheriting Ethereum's settlement security via STARK proofs. The November 2025 Grinta upgrade brought sub-500ms pre-confirmations, and the Stwo prover integration improved proving efficiency. For the full privacy architecture breakdown including the three-layer model, Privacy Council structure, and trust assumptions, see our prior report.

ZK-Rollup / Validium L2 (Lighter, EdgeX). Both platforms settle to Ethereum via zero-knowledge proofs, but with meaningfully different implementations and data availability models. Lighter built a custom ZK-Rollup achieving approximately 300ms latency and 1,000 TPS, and open-sourced its audited ZK circuits in December 2025, a significant transparency commitment that enables independent verification of the proof system's integrity. EdgeX currently runs on StarkEx in Validium mode where trading data is stored off-chain with a Data Availability Committee rather than posted to Ethereum. This Validium architecture provides EdgeX with inherent position privacy: positions, margin balances, and liquidation levels are not published on-chain, making them invisible to external observers. EdgeX is transitioning to a modular multi-VM architecture in V2 (targeted Q1 2026), which separates perpetual execution (edgeVM) from standard DeFi operations (edgeEVM), adds parallel transaction execution, and introduces FlashLane QoS scheduling for latency-sensitive operations.

ZK-powered Validium (GRVT). GRVT occupies a distinct architectural position as a sovereign ZK Chain built on Matter Labs' ZK Stack, operating in Validium mode within the ZKsync Elastic Network. Unlike applications deployed on existing L1/L2 infrastructure, GRVT controls its own chain configuration, sequencing, and data policies while posting ZK validity proofs to Ethereum for settlement. The Validium architecture stores trading data off-chain rather than on Ethereum, which provides both privacy (positions, margins, and liquidation levels are invisible to external observers) and scalability (claimed throughput of up to 600,000 trades per second with sub-2ms off-chain matching latency) at the cost of additional trust in the operator and a Data Availability Committee (DAC). The November 2025 ZKsync Atlas integration enabled native interoperability between Ethereum L1 and ZK Stack chains, providing GRVT with native Ethereum Mainnet liquidity access without bridges. The hybrid architecture processes performance-sensitive operations (order matching, risk calculations) off-chain while pushing fund-impacting actions on-chain, where smart contracts validate that liquidations are mathematically fair before settlement.

Application on Existing L1/L2 (Variational, Aster, Extended). Variational deploys on Arbitrum using an RFQ model rather than CLOB, where the Omni Liquidity Provider (OLP), a team-operated market maker, acts as sole counterparty to all retail trades, hedging externally on CEX/DEX venues. This eliminates the orderbook entirely and enables zero-fee trading, but introduces counterparty concentration risk and a structural dependency on a single entity's hedging capability. Aster deploys across BNB Chain (78% of TVL), Arbitrum, Ethereum, and Solana with a hybrid architecture. Extended migrated from StarkEx to Starknet mainnet in mid-2025, gaining Cairo programmability. Its architectural distinction lies in looking to embed unified margin logic at the base layer itself as an ERC-20 token, meaning any application deployed on the network will automatically inherit access to users' margin and shared liquidity. Rather than treating margin as an application-level feature that each protocol must implement independently, Extended treats it as network infrastructure, analogous to how TCP/IP provides networking as a base-layer service rather than requiring each application to build its own.

Settlement and Security. For institutional risk frameworks, the settlement layer determines ultimate recourse. ZK proofs (SNARKs/STARKs) to Ethereum (Paradex, Lighter, Extended) offer the strongest verifiability with onchain data availability. ZK proofs with Validium data availability (EdgeX) provide equivalent proof system strength but with off-chain DA trust assumptions. ZK proofs to Ethereum via ZKsync (GRVT) follow closely, inheriting Ethereum's security guarantees through validity proofs on settlement level despite the Validium data availability trade-off. Optimistic proofs via Arbitrum (Variational) provide weaker finality guarantees, dependent on a functioning verifier system. Hyperliquid's custom L1 consensus is strong, but has no Ethereum fallback, and Aster's guarantees vary by deployment chain and relies largely on offchain logic.

3. Market Microstructure, Fee Economics, and Execution Quality

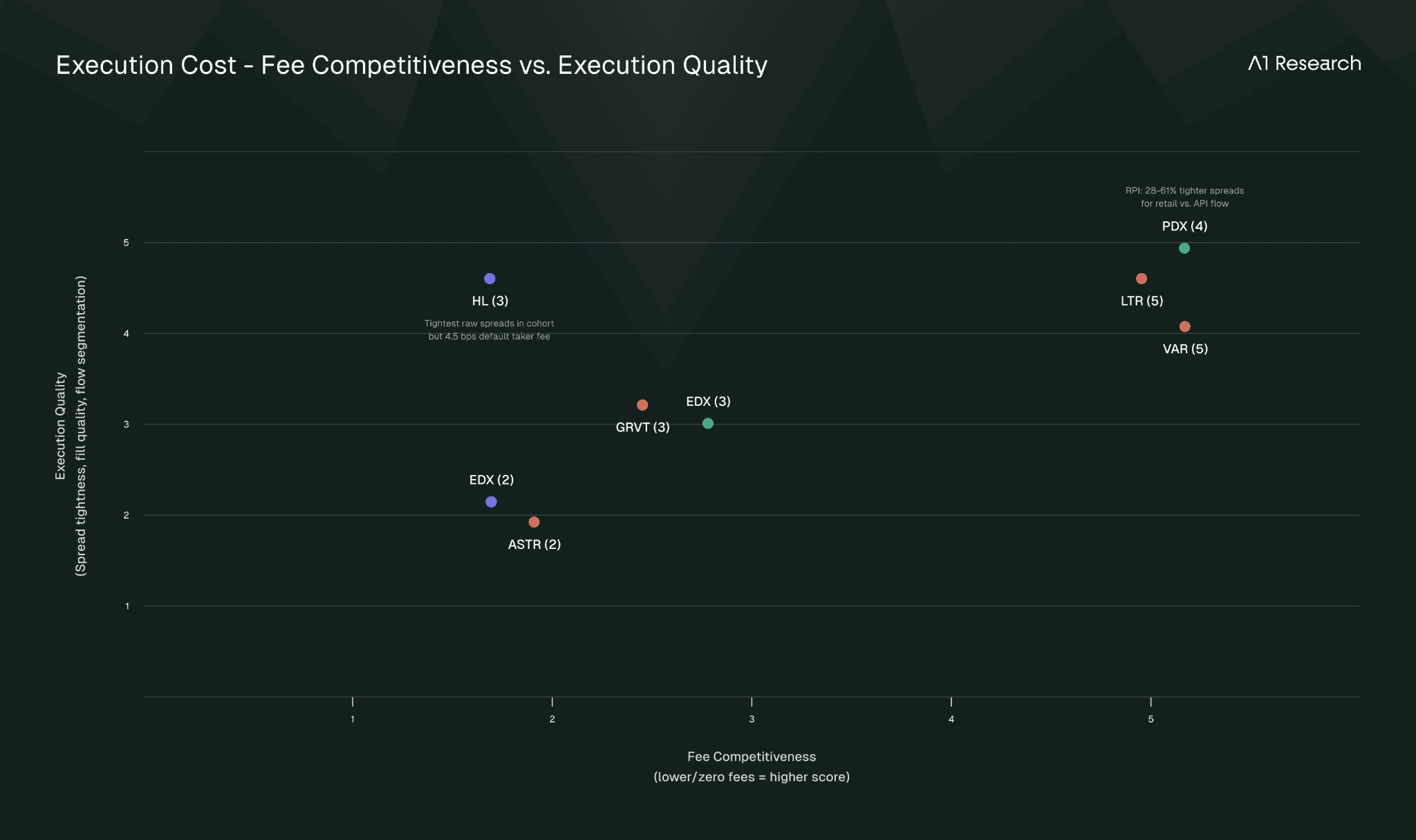

As the market entered a maturing phase, the fee structures have diverged sharply, reflecting different business model philosophies that matter far more than headline spread numbers suggest.

Zero-fee models now represent a meaningful share of the market. Paradex charges 0% for retail makers and takers, monetizing instead through a PFOF-style mechanism where market makers pay 0.5 bps for access to curated retail flow via the RPI system (professional/API traders pay 2 bps taker). Lighter charges zero fees for retail, with revenue from its liquidity pool and mandatory 1:10 LIT staking (introduced January 2026): for every $1 deposited into the LLP, depositors must stake $0.10 equivalent in LIT tokens, creating structural token demand that partially offsets the revenue foregone by eliminating trading fees while aligning LP incentives through capital commitment beyond passive liquidity provision. Variational charges zero trading fees entirely, capturing revenue through OLP spread, partially redistributed via loss refunds (1-5% base) and volume-tiered discounts.

Tiered fee models remain standard elsewhere. Hyperliquid charges 0.2 bps maker / 4.5 bps taker at default tier, with maker rebates driving its tight spreads. EdgeX charges 2/6 bps, GRVT offers negative maker fees at all tiers (rebates from -0.01 bps at Level 1 to -0.3 bps at Level 9) with 4.5 bps default taker, making it the first onchain exchange to pay all retail traders for providing liquidity, Extended offers maker rebates (0.2-1.3 bps) at volume thresholds, and Aster operates at 2/5 bps.

Order Flow Segmentation and Execution Quality

Fees are only one component of total execution cost. The deeper question is how orders are matched and what protections exist against adverse selection, the problem where informed or toxic flow systematically picks off stale quotes and degrades market maker willingness to quote tight.

Paradex's RPI (Retail Price Improvement) system is the most sophisticated approach in the cohort. The mechanism segments order flow at the sequencer level: retail orders placed through the Paradex UI are routed to a dedicated RPI book where market makers pay 0.5 bps for access to curated, non-toxic flow. Because these market makers know they are quoting against human retail traders rather than latency-arbitrage bots or MEV searchers, they can offer tighter spreads with larger size. The result, documented in our prior research, is significant: RPI spreads are 28-61% tighter than API-only spreads across major pairs, with SOL perpetuals showing RPI spreads less than half the API spread. This is structurally analogous to TradFi payment-for-order-flow arrangements, but with a critical difference: the price improvement is measurable, transparent, and accrues directly to the retail trader rather than being captured by an intermediary.

The latency advantage problem, where co-located or faster participants systematically extract value from slower market makers, is addressed differently across platforms. Paradex's sequencer-level flow segmentation acts as an implicit speed bump: retail flow is separated before it reaches the main orderbook, eliminating the latency race entirely for that flow category. Hyperliquid's fully onchain orderbook means all participants compete on the same infrastructure with no segmentation, which produces tight raw spreads through aggressive maker rebates but exposes all order flow to the same latency dynamics. GRVT and EdgeX operate off-chain matching engines with on-chain settlement, where the operator controls matching priority but without explicit flow segmentation mechanisms. Variational sidesteps the problem entirely through its RFQ model: there is no orderbook to front-run, but the OLP as sole counterparty must price in its own hedging latency risk.

Fee-Adjusted Execution Cost Analysis

In our previously published Paradex research, we conducted statistical orderbook analysis across seven platforms using 328 independent snapshots (January 13-16, 2026). The key finding: when trading fees are included in total execution cost for a $100K BTC market order, the ranking shifts materially. Zero-fee venues move from mid-tier on raw spreads to top-three on total cost. Exchanges showing sub-basis-point spreads but charging 4.5+ bps in taker fees become more expensive on a total cost basis. For the full quantitative breakdown including per-asset depth metrics and slippage simulations, refer to that report.

Funding Rate Mechanics: The Hidden Cost Layer

For institutions holding positions over multi-day or multi-week horizons, funding rates represent a cost that can materially exceed trading fees. Funding is the periodic payment exchanged between long and short position holders to keep perpetual contract prices anchored to spot. When perp prices trade above spot, longs pay shorts; when below, shorts pay longs. The mechanism is universal, but the implementation details differ significantly across platforms, creating divergent cost-of-carry profiles.

Hyperliquid computes an 8-hour funding rate using a standard formula: Funding Rate = Average Premium Index + clamp(Interest Rate - Premium Index, -0.0005, +0.0005), with the interest rate component fixed at 0.01% per 8 hours (approximately 11.6% APR paid to shorts). However, unlike CEXs that settle every 8 hours, Hyperliquid settles funding every hour at one-eighth of the computed 8-hour rate. The premium is sampled every 5 seconds and averaged over each hour. Funding is capped at 4% per hour, significantly higher than most CEX caps, meaning Hyperliquid positions can experience larger funding spikes during extreme market dislocations.

Paradex uses a continuous accrual model, fundamentally different from discrete-interval settlement. Funding accrues continuously as unrealized PnL and is realized only when a position is adjusted on-chain. This eliminates the discrete price jumps that occur on platforms with snapshot-based funding: on exchanges like Binance, a trader who opens a long position one minute before an 8-hour funding snapshot pays the full period's rate. On Paradex, the same trader would pay funding proportional only to the time held. For basis traders and delta-neutral strategies, this continuous mechanism produces more predictable carry costs and eliminates the "funding sniping" behavior where traders close positions just before adverse funding snapshots.

Variational handles funding differently due to its RFQ architecture: the OLP absorbs funding exposure as part of its spread, meaning traders do not pay or receive discrete funding payments. The cost of carry is instead embedded in the OLP's quoted prices, which can be opaque to the end user.

The remaining platforms (EdgeX, Extended, GRVT, Lighter, Aster) implement standard 8-hour funding rate mechanisms with formula-based computation. For institutional participants running cross-venue basis trades, the divergence in settlement intervals (1-hour on Hyperliquid, continuous on Paradex, 8-hour on most others) creates both risk and opportunity: normalized funding rates across venues can differ by several basis points during volatile periods, generating carry trade alpha for sophisticated participants while creating hidden costs for those who do not account for the differences.

Liquidation Mechanics, Insurance Funds, and Loss Socialization

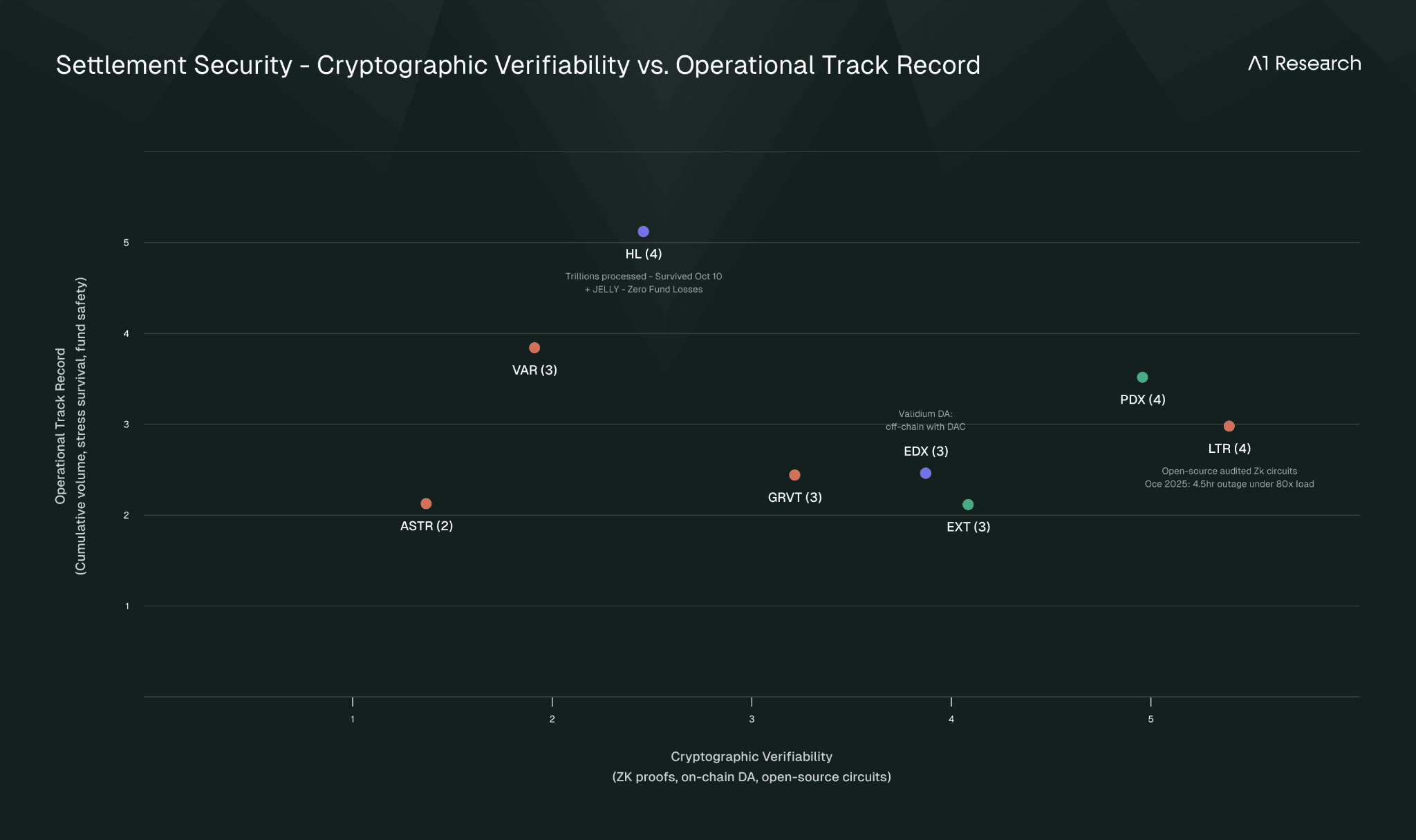

How a platform handles underwater positions when the liquidation engine cannot close at market prices is one of the most consequential, yet least discussed, dimensions of exchange architecture. The design choice directly determines who bears tail risk during extreme market events, and the October 10, 2025 crash (Section 7) transformed what had been abstract architectural differences into concrete, dollar-denominated outcomes for different user segments.

Hyperliquid: Three-Tier Waterfall. Hyperliquid operates a three-tier liquidation waterfall. When a position hits its liquidation price but cannot be closed through normal market orders, the liquidation engine first attempts market-rate closure. If that fails, the position passes to the HLP (Hyperliquidity Provider) vault, roughly $400-500M in TVL as of February 2026, which acts as backstop liquidator. HLP depositors earn yield from market-making activity in normal conditions but absorb toxic, underwater positions during cascading liquidations. If even the HLP cannot absorb the position, the system triggers Auto-Deleveraging (ADL), forcibly reducing profitable traders' positions to offset the shortfall. Hyperliquid also maintains a separate Assistance Fund, a mechanism funded by protocol fees that automatically converts trading fees to HYPE in a fully automated manner as part of L1 execution. As of February 2026, the Assistance Fund held approximately 40 million HYPE (valued at roughly $1.25 billion), with a December 2025 validator vote formalizing recognition of these tokens as permanently burned. The Assistance Fund is distinct from HLP and serves a different function: it is a fee-recycling and token value accrual mechanism rather than a liquidation backstop. The October 2025 crash triggered ADL for the first time in Hyperliquid's history, with the academic analysis referenced below documenting $2.1 billion in positions closed via ADL within 12 minutes, demonstrating that the three-tier system can be exhausted under sufficient stress. The March 2025 JELLY incident demonstrated the manipulation surface area inherent in a transparent backstop model. On March 26, a coordinated attack exploited JELLY token markets: the attacker shorted JELLY on Hyperliquid while simultaneously buying spot JELLY on external DEXs to trigger a short squeeze. The resulting price spike created an unrealized loss of $12-13.5 million on the toxic short position that was absorbed by HLP. Hyperliquid ultimately intervened by delisting the JELLY market and force-settling at $0.0095, well below the prevailing market price of approximately $0.50, a decision that erased the attacker's gains and resulted in HLP actually profiting roughly $700K on the settlement. The incident was controversial: the forced delisting at a non-market price raised questions about the degree of centralized intervention possible on the platform. In response, Hyperliquid implemented stricter leverage limits (BTC capped at 40x, ETH at 25x) and a 20% minimum collateral retention rule to reduce the likelihood of similar attacks.

Paradex: Insurance Fund + Socialized Loss. Paradex takes a deliberately different approach, with no ADL mechanism. Liquidated positions and their associated liquidation penalties transfer to the Insurance Fund, which is funded by accumulated penalties and can be recapitalized via profitable liquidation unwinds or protocol transfers. The fund balance is publicly verifiable on-chain via the Paraclear smart contract. If the Insurance Fund is depleted during extreme events, Paradex applies a Socialized Loss Factor to withdrawals only: users who do not withdraw are unaffected, and the penalty is removed once the fund is recapitalized. Paradex has published a detailed argument for why socialized loss is superior to ADL in portfolio-margin environments, centering on what the team calls "portfolio blindness": ADL breaks cross-instrument hedges by closing individual legs without considering overall account exposure. A trader hedging a long ETH perp with a short BTC perp could have only the profitable leg forcibly closed by ADL, leaving an unintended directional exposure, exactly the outcome that portfolio margin was designed to prevent. The counterargument deserves equal weight: socialized loss penalizes users who need to withdraw during a crisis, creating a liquidity trap where the most risk-averse participants (those seeking to exit during turmoil) bear disproportionate cost, while users who remain are effectively subsidized. In a severe enough event, awareness of potential withdrawal penalties could itself trigger a withdrawal rush, creating the very bank-run dynamic the mechanism aims to prevent. Both approaches involve trade-offs; the question is whether the platform's user base is better served by predictable individual-level risk (ADL) or collective tail-risk sharing (socialized loss).

Lighter: LLP Backstop + Conservative ADL. Lighter uses the Lighter Liquidity Pool (LLP) as its first line of defense, similar in concept to Hyperliquid's HLP but with conservative ADL trigger policies. The LLP absorbs liquidation positions in normal conditions, participating in market making and acting as the protocol's risk buffer mechanism. ADL is available as a backstop but triggers rarely. During the October 10, 2025 crash, the LLP suffered a 5.35% drawdown (approximately $21.5M in losses) while the platform experienced a multi-hour sequencer outage (Section 7), but ADL did not trigger despite the severe operational stress.

“Pure” ADL Platforms (EdgeX, GRVT, Aster, Extended). Several platforms in the cohort implement Insurance Fund plus ADL systems as standard architecture. The Insurance Fund absorbs initial losses, with ADL activating when the fund is depleted. ADL systems typically maintain a priority queue ranking counterparties by profit and leverage, deleveraging the most profitable and most leveraged positions first. GRVT adds an important additional layer: liquidations are triggered off-chain by the risk engine but then sent to the GRVT L2 chain and validated on-chain via smart contracts to ensure mathematical fairness, providing a transparency guarantee even though the matching engine operates off-chain. GRVT's relatively smaller scale compared to Hyperliquid means it has not been battle-tested to the same degree during extreme market events.

Insurance Fund Sizing. The capitalization of backstop mechanisms varies dramatically across the cohort and directly affects each platform's capacity to absorb tail-risk events without triggering ADL or socialized losses. Hyperliquid's HLP vault (almost $400M TVL) serves as the primary liquidation backstop, supplemented by the Assistance Fund (approximately 40 million HYPE, valued at roughly $1.14 billion, though this functions as a fee-recycling mechanism rather than a liquidation reserve). Lighter's LLP holds approximately $256M in TVL, functioning simultaneously as market maker, insurance fund, and yield source for depositors. EdgeX's eLP vault and dedicated insurance fund draw on an approximately $118M treasury. Paradex's Insurance Fund is Paradex's Insurance Fund balance is publicly queryable via both a REST API endpoint and the Paraclear smart contract's getTokenAssetBalance function on L2, with state transition correctness guaranteed by STARK proofs to Ethereum, though independent balance reconstruction from L1 alone is not possible without Privacy Council decryption keys, a trade-off inherent to the encrypted state diff architecture. The balance is modest relative to Hyperliquid and Lighter given Paradex's smaller scale. For the remaining platforms (GRVT, Variational, Extended, Aster), insurance fund balances are either not publicly disclosed or are too early-stage to benchmark meaningfully. The concentration of backstop capital in Hyperliquid and Lighter reflects their larger scale, but also means these platforms have the most to lose when backstop mechanisms are tested, as October 10 demonstrated.

Variational faces an entirely different risk vector: the OLP as sole counterparty must hedge externally in real time, and hedging lag during rapid price movements can result in hedging costs exceeding spread revenue, testing the sustainability of the single-counterparty model under genuine stress. The October 2025 crash stress-tested this directly (Section 7).

The ADL Trilemma. An academic analysis of ADL systems published in December 2025, using Hyperliquid's October 10 data as its empirical foundation, formalized what practitioners have long intuited: there exists an "ADL Trilemma," the impossibility of simultaneously satisfying solvency (ensuring the platform remains solvent), revenue (maintaining fee income from continued trading), and fairness (treating profitable traders equitably). Any ADL design can optimize for at most two of these three properties, and the choice reveals the platform's priorities. The paper documented that Hyperliquid lost nearly 50% of its open interest in the weeks following October 10, suggesting that aggressive ADL activation, while preserving solvency, carried significant costs in trader retention and platform revenue. Paradex's socialized-loss model sidesteps this trilemma entirely by eliminating ADL from its architecture, though at the cost of placing ultimate tail risk on the insurance fund and, in extremis, on withdrawing users.

The intersection of liquidation mechanics and transparency creates an additional extractable-value dynamic. On fully transparent chains like Hyperliquid, every trader's liquidation levels are publicly visible, enabling sophisticated participants to identify clusters of liquidation prices and execute strategies designed to push prices through those levels, triggering cascading liquidations that generate profit. This "liquidation MEV" is structurally impossible on privacy-preserving venues like Paradex, GRVT, and EdgeX, where liquidation levels are not observable by external parties, a point explored further in Section 4.

Competitive Dynamics

The zero-fee trend parallels Robinhood's disruption of equity commissions, and the competitive implications are significant. If Lighter pairs builder rebates with zero fees, third-party frontends could route flow through Lighter and capture the entire fee stack, potentially doubling revenue versus Hyperliquid's 4.5 bps. The infrastructure already exists: LiquidTrading (Paradigm-backed, $7.6M seed) facilitates billions in volume across Hyperliquid, Ostium, and Lighter.

4. Privacy: The Institutional Unlock

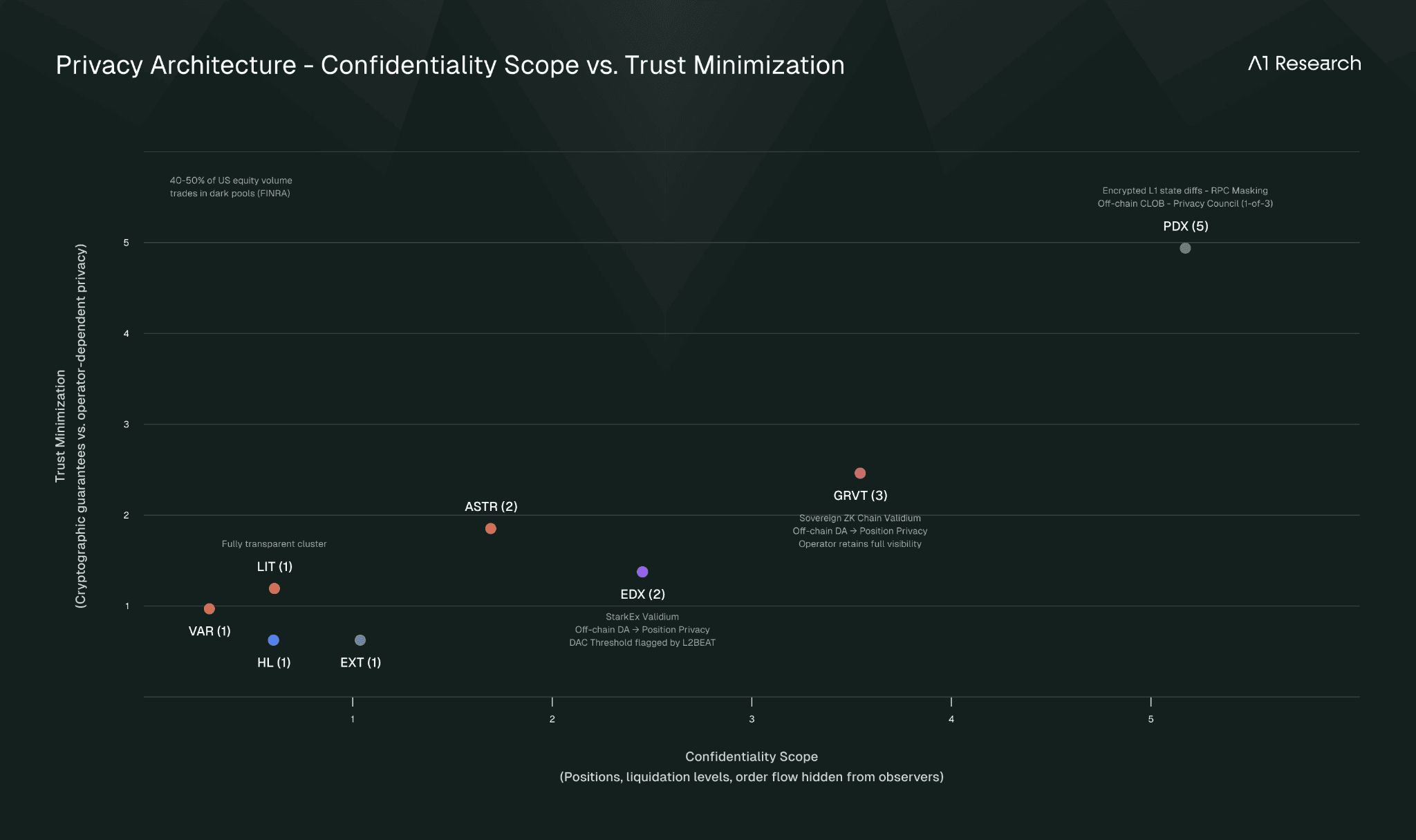

Every trade on a transparent blockchain is a signal. Position sizes, entry points, liquidation levels, and profit targets are all broadcast to any observer willing to parse the data. For institutions managing serious capital, this information leakage is not theoretical but quantifiable. "Whale hunting," the practice of targeting large visible positions for coordinated liquidation attacks, is a documented and profitable on-chain strategy. Traditional finance addressed this problem decades ago through off-exchange venues, including dark pools, internalizers, and confidential OTC markets, which collectively accounted for over 50% of total U.S. equity volume throughout 2025. Industry on-exchange share fell to 48.8% in Q3 2025 before recovering slightly to 49.1% in Q4, per Nasdaq's quarterly market data. The trend is widespread across all market caps and stock price ranges, not limited to sub-dollar microcap trading (Nasdaq Research). Onchain equivalents must exist for institutional adoption to scale beyond its current bounds.

Paradex is currently the only production venue offering comprehensive, purpose-built position confidentiality: encrypted state diffs on Ethereum L1, RPC-masked account data on L2, and off-chain CLOB execution where orders never touch a public mempool. The trust assumption matters: Paradex's centralized sequencer retains order flow visibility during matching (operator-trust privacy, not trustless cryptographic privacy), but the operator never takes custody of user funds. The Privacy Council (Paradex, Paradex Foundation, Karnot) with 1-of-3 decryption threshold provides emergency recovery. Architectural privacy is significantly harder to retrofit than to build from inception. The complexity of retrofitting privacy into transparent execution layers, which requires changes to state commitment schemes, RPC infrastructure, and settlement data formats, would require competitors an estimated 12+ months of dedicated engineering to replicate Paradex's current privacy stack.

GRVT achieves meaningful privacy as a structural byproduct of its sovereign ZK Chain architecture operating in Validium mode. Because GRVT runs its own chain within the ZKsync Elastic Network rather than deploying on a shared transparent rollup, trading data including positions, margin balances, and liquidation levels is stored off-chain rather than posted to Ethereum, making it invisible to external observers. The practical outcome for traders is significant: liquidation hunting, position sniping, and front-running based on visible on-chain data are structurally eliminated, similar to Paradex. However, there are important distinctions. GRVT's privacy was not designed from inception as a multi-layer confidentiality system; it is an inherent property of the Validium data availability model, chosen primarily for scalability and cost efficiency. The operator (GRVT) retains full visibility into all trading activity, and per L2BEAT's assessment, the Data Availability Committee's validator contract only checks formatting rather than serving as a true DA oracle. There is no Privacy Council equivalent or encrypted L1 state commitment. The privacy is real and architecturally embedded, but it is operator-dependent with fewer redundancy layers than Paradex's purpose-built system.

EdgeX derives a similar class of privacy from its StarkEx Validium architecture. As a "Central Validium" per L2BEAT's classification, EdgeX stores user balance and position data off-chain with a Data Availability Committee rather than publishing it on Ethereum. This means positions, margin states, and liquidation levels are not visible to external chain observers, which is essentially the same structural property that prevents liquidation hunting on GRVT. However, EdgeX's privacy carries additional trust assumptions: the DAC threshold has been flagged by L2BEAT as potentially too low, and the operator retains full visibility. Unlike Paradex and GRVT, EdgeX does not actively position privacy as a core feature of its value proposition, and the V2 migration to a multi-VM architecture could potentially alter the data availability model. The privacy is architecturally real but not purpose-built or explicitly marketed.

Aster introduced "Hidden Orders" functionality addressing order visibility, but not position or liquidation level privacy. The remaining platforms (Hyperliquid, Lighter, Extended, and Variational) operate with fully transparent or minimally obfuscated state.

5. Programmability and Builder Ecosystems

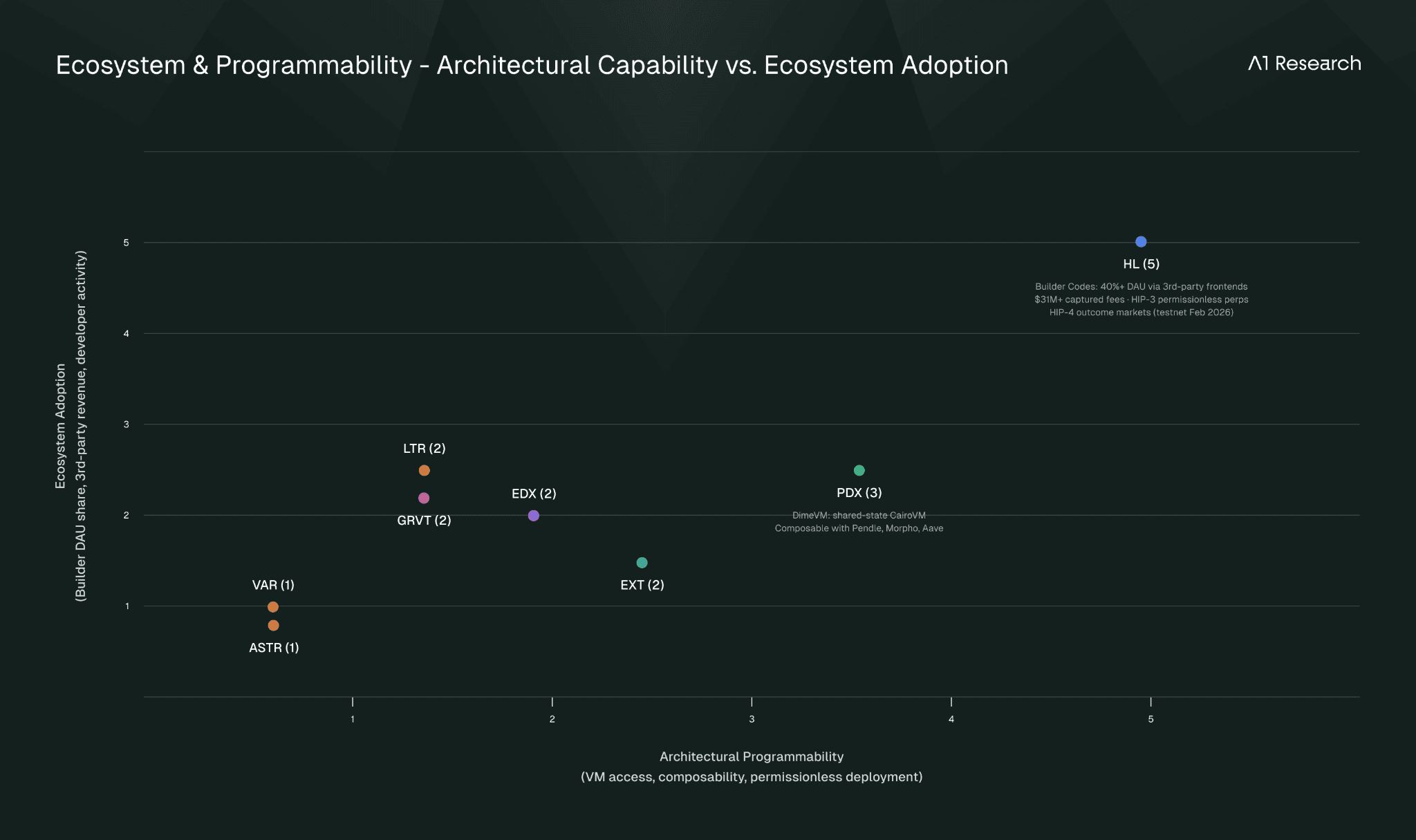

A perp DEX that functions only as a standalone trading application faces a ceiling on its network effects. A perp DEX that functions as programmable infrastructure, where developers can build frontends, deploy custom markets, create structured products, and compose with exchange liquidity, creates exponentially more defensible advantages. This is one of the most consequential dimensions of differentiation in the cohort.

Hyperliquid: The AWS of Liquidity

Hyperliquid executed a strategic pivot in mid-2025 from B2C to B2B infrastructure, building the most developed builder ecosystem in the perp DEX space.

Builder Codes are an on-chain revenue attribution mechanism allowing third-party apps to earn up to 10 bps on perps and 100 bps on spot trades routed through their interfaces. Adoption has been striking: roughly 40% of daily active users now trade via third-party frontends (peaked above 50% in late October 2025). The top three builders (Based, Phantom, pvp.trade) captured over $31M in fees collectively, with Phantom earning $100K+ daily.

HIP-3 (Builder-Deployed Perpetuals) enables permissionless perpetual market deployment on HyperCore, requiring a 500K HYPE stake (expected to decrease over time). Deployers control oracle prices, leverage limits, and market settlement parameters while inheriting the full HyperCore stack: the high-performance matching engine, unified cross-margin, and the entire API surface. This opens the door to RWA perps, AI hashrate futures, commodity indices, and any derivative product the deployer can define. The staking requirement is maintained for 30 days post-market-halt with theoretical slashing capability. Critically, HIP-3 markets plug into every Builder Code frontend instantly: a new RWA perpetual deployed at 3pm becomes tradeable across Phantom, pvp.trade, and every other third-party interface by 3:01pm, with zero additional integration work. This is the distribution flywheel in action. HIP-3 markets have already exploded to record deployment highs, validating the permissionless model.

HIP-4: Outcome-Based Markets

HIP-4 (Outcome-Based Markets), announced on February 2, 2026 and currently on testnet, represents Hyperliquid's most ambitious product expansion to date. Outcome contracts are fully collateralized instruments that settle at a fixed price within a predefined range, introducing dated markets and non-linear payoffs to a system previously limited to perpetuals. Unlike leveraged derivatives, outcomes require no margin trading and carry zero liquidation risk: buyers can lose only their initial capital.

The implications are significant. If a trader believes BTC will exceed $100K by the end of March, they buy the corresponding outcome contract. At expiry, it settles at the upper bound (profit) or lower bound (loss limited to initial cost). No margin calls, no overnight liquidations. This structure naturally fits two use cases: prediction markets (betting on event outcomes) and bounded options-like instruments (expressing directional views within defined risk parameters).

What makes HIP-4 strategically distinct from standalone prediction platforms is composability. HIP-4 contracts run on HyperCore, sharing the same trading engine and unified cross-margin system as perpetuals. A trader can hold a long ETH perp while simultaneously buying an outcome contract that pays if ETH falls below a threshold, both positions in the same margin account, automatically offsetting each other, reducing net risk exposure, and freeing excess margin. In TradFi terms, this is a structured product. Investment banks charge significant fees to construct such combinations. Hyperliquid aims to enable this natively, no intermediaries required, with automatic cross-instrument hedge recognition. Standalone prediction exchanges like Polymarket and Kalshi, which collectively processed tens of billions in volume during 2025, cannot offer this kind of cross-product margining because they operate as isolated event markets rather than integrated derivative engines.

The initial rollout will feature curated markets denominated in USDH (Hyperliquid's native stablecoin), with permissionless deployment opening based on user feedback. The progression from HIP-3 (permissionless perps) to HIP-4 (permissionless outcomes) transforms HyperCore from a perpetual futures engine into a general-purpose derivatives primitive layer.

HyperEVM and CoreWriter bridge smart contract composability with the high-performance orderbook. CoreWriter enables HyperEVM contracts to place orders, manage vaults, and interact with validators on HyperCore. Kinetiq, the dominant liquid staking protocol (~$650M TVL, approximately 80% LST market share), exemplifies this: staked HYPE on HyperEVM can be leveraged to build HIP-3 markets on HyperCore, creating a capital efficiency loop where liquid staking protocols become the ecosystem's economic connective tissue.

The strategic logic behind this pivot is clear. Rather than fighting market share fragmentation at the application layer, Hyperliquid moved to own the infrastructure layer. If every frontend routes through HyperCore regardless of brand, market share at the application layer becomes less relevant.

Paradex: DimeVM and the SuperChain

Paradex is building DimeVM, a general-purpose CairoVM platform sharing state with the exchange. Developers deploy Starknet-compatible contracts with mature tooling (Hardhat, Starkli), enabling third-party dApps to compose directly with Paradex's margin system, settlement layer, and risk engine. The vision: an onchain financial "SuperDEX" extending beyond trading into programmable finance.

DimeVM's shared-state architecture is the key differentiator from Hyperliquid's HyperEVM/CoreWriter model. Where HyperEVM contracts interact with HyperCore through CoreWriter, a system contract that enables cross-domain actions but with multi-second delays and no atomicity guarantees (a failed HyperCore action does not revert the originating HyperEVM transaction), DimeVM contracts share state directly with the exchange's on-chain systems, meaning a smart contract can read and write to the same state as the margin system, settlement layer, and risk engine without cross-domain messaging. This enables atomic composability for on-chain operations: a vault strategy can simultaneously adjust margin, manage collateral, and interact with external DeFi protocols in a single transaction. Order execution itself routes through the off-chain sequencer for latency optimization, consistent with Paradex's hybrid architecture. Paradex has committed to open-sourcing all components of the Paradex Network's stack, including the web app, risk engine, chain, backend, and APIs, a meaningful distinction in a space where most exchange infrastructure remains proprietary.

In production, DimeVM currently powers the Universal Portfolio Margin system, where CairoVM executes real-time risk analysis to deliver 80-90% margin reduction for hedged positions. It also underpins Paradex Vaults, which produce LP tokens designed for composability with external DeFi protocols including Pendle, Morpho, and Aave. Developer adoption is early-stage relative to Hyperliquid's builder ecosystem, reflecting both Paradex's younger platform age and the smaller CairoVM developer base compared to Solidity/EVM. However, the maturity of Starknet tooling and Paradex's integration with the broader Starknet ecosystem (including Starknet-native wallets) provide a development infrastructure that is production-ready rather than experimental.

The roadmap extends DimeVM into a full financial stack: XUSD (yield-bearing synthetic dollar), integrated borrow/lend markets, perpetual options (already live), dated options, and pre-markets, with the stated goal of making Paradex the base layer for programmable onchain finance rather than simply a derivatives exchange.

The Rest of the Spectrum

EdgeX V2 (Q1 2026) will introduce a modular multi-VM execution architecture with permissionless market deployment, moving away from the StarkEx implementation. Extended on the other hand embeds a unified margin at the base layer as an ERC-20 primitive accessible to all network applications, while GRVT launched Builder Codes (similar to Hyperliquid) in December 2025 (with Tealstreet, Tread.fi as first partners). Lighter has its own ZK EVM on its 2026 roadmap with Turing-complete circuits and Universal Margin allowing Ethereum L1 assets as collateral. Variational and Aster have no programmability layer or builder ecosystem, a significant long-term limitation for network effects.

6. Product Feature Differentiation

The convergence of trading, lending, and structured products within a single margin account is the defining product trend of 2026. For institutional participants, the question is which platforms deliver multi-product capital efficiency without fragmenting risk management across venues. The subsections below map where each platform stands across the dimensions that matter most for this convergence.

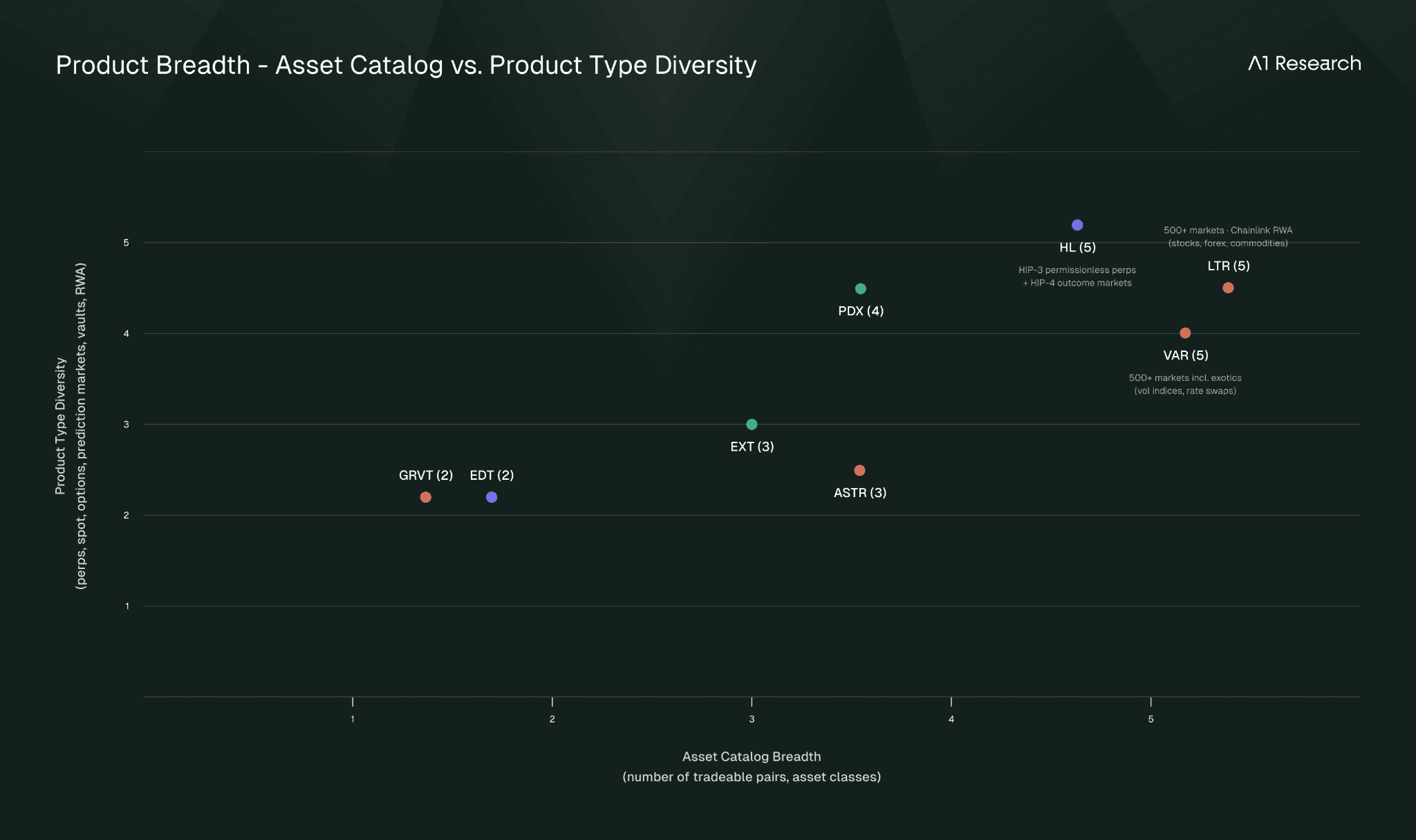

Asset Coverage

Lighter and Variational lead breadth at 500+ markets each. Lighter's Chainlink 24/5 U.S. Equities Streams integration (from January 2026) enables perpetual stocks, forex, and commodities, definitely one of the most concrete TradFi bridges in the cohort. Variational's automated Listing Engine onboards projects within hours of TGE (Eclipse listed 3 hours post-launch) and includes exotics like volatility indices and interest rate swaps. Paradex lists 250+ markets and is the first DEX with both perps and perpetual options fully onchain. Hyperliquid offers hundreds of markets too with HIP-3 enabling a rapid, permissionless expansion. EdgeX covers 100+ pairs including TradFi markets, while GRVT, Aster and Extended are in a similar range.

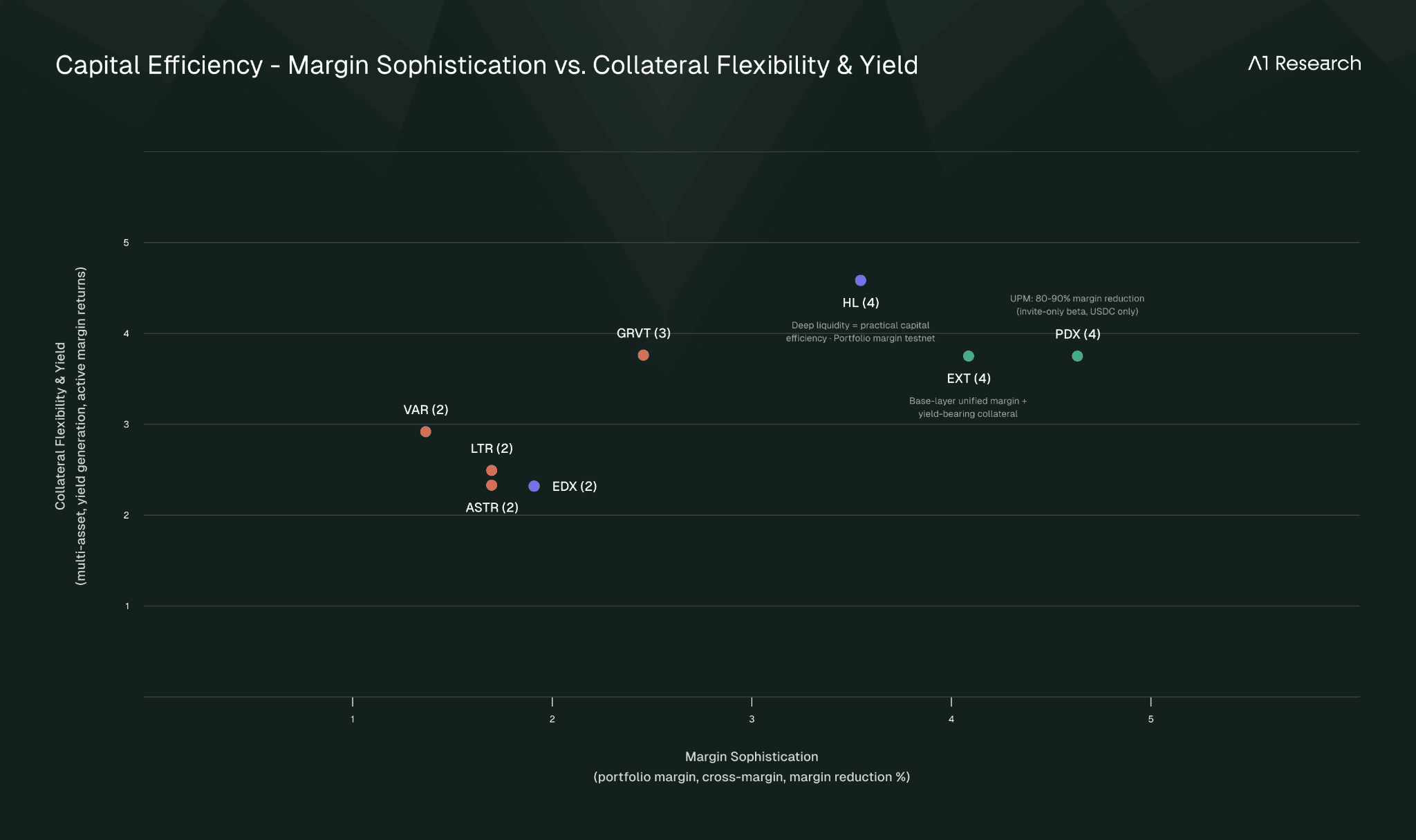

Margin Systems and Cross-Collateral

Paradex leads with Universal Portfolio Margin (CairoVM-powered, 80-90% margin reduction for hedged positions, isolated/cross/portfolio modes, sub-accounts for strategy isolation; currently invite-only beta). Extended's Native Unified Margin embedded at the base layer is the most architecturally ambitious approach. Hyperliquid has portfolio margin in pre-alpha testnet (December 2025), unifying spot and perp positions. GRVT targets unified margin Q1 2026. Lighter and EdgeX plan portfolio margin in 2026. Variational uses isolated settlement pools per trade with no unified margin. Aster offers standard cross-margin.

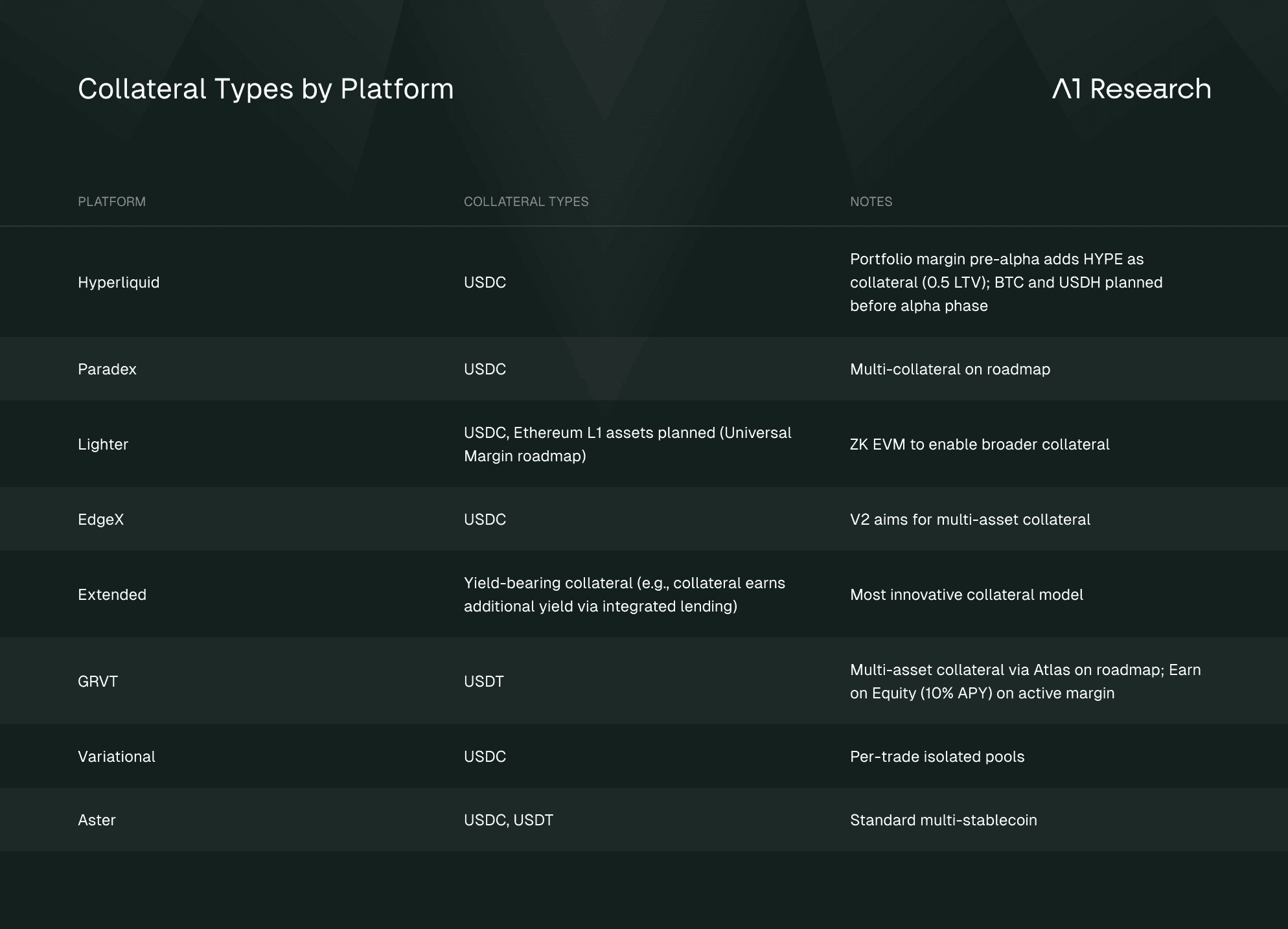

Collateral types accepted for margin vary significantly and directly impact capital efficiency:

Extended's model stands out: deposited collateral earns additional yield through the integrated lending market, meaning traders' margin balances generate returns even while securing positions. This is a fundamentally different capital efficiency proposition than platforms where collateral sits idle. GRVT's Earn on Equity program (10% APY on active trading margin, compounding every 4 hours) represents a novel approach to the same problem, directly subsidizing the opportunity cost of capital locked in margin accounts.

Lending, Options, and Vaults

The convergence of trading and lending is a defining 2026 trend. Extended leads the pack here with a live integrated lending/borrowing market where yield-bearing collateral earns additional yield. Paradex plans seamless borrow/lend from its unified account plus XUSD for yield stacking. Hyperliquid integrates HyperEVM lending into portfolio margin. Paradex is the only venue with live perpetual options onchain; GRVT plans an options orderbook Q1-Q2 2026, while Variational Pro supports customizable OTC options.

On vaults, Hyperliquid's HLP (~$373M TVL per Hyperscreener data, lifetime Sharpe of 2.89, peaking above 5.2 in early 2025 before compressing to ~1.7 in 2025 YTD) and Kinetiq liquid staking (~$639M TVL, down from a $2.5B peak and highly sensitive to HYPE price) dominate. Lighter's LLP grew to ~$500M TVL by November 2025, generating roughly 60% APY through mid-2025 at lower TVL before compressing to ~34% APY at scale; with volumes declining six-fold from $300B weekly in November to under $50B by February 2026, current yields are likely lower still. GRVT's GLP stands out for risk-adjusted performance (11.4 Sharpe and 25.6% APR per Messari's December 2025 assessment, though measured over only seven weeks since its November 11 launch at just $8.4M AUM; the six-month pre-launch backtest showed a 7.6 Sharpe at ~48% APR). GLP is managed by Ampersan, an ex-Optiver team, charges 0% management fees, distributes 100% of yield to depositors, and runs an explicitly delta-neutral strategy. Paradex offers programmable multi-strategy vaults composable with external DeFi. EdgeX's eLP vault has delivered high APRs (81.5% per Messari in November 2025 at $179.5M TVL), while Extended's vault runs at more modest rates (12-20% APR per available data). Variational's OLP achieved 300%+ annualized yield from April to July 2025, though this reflected a small initial vault size, and sustainability at scale remains unproven

7. Market Data: Who Is Winning and Why

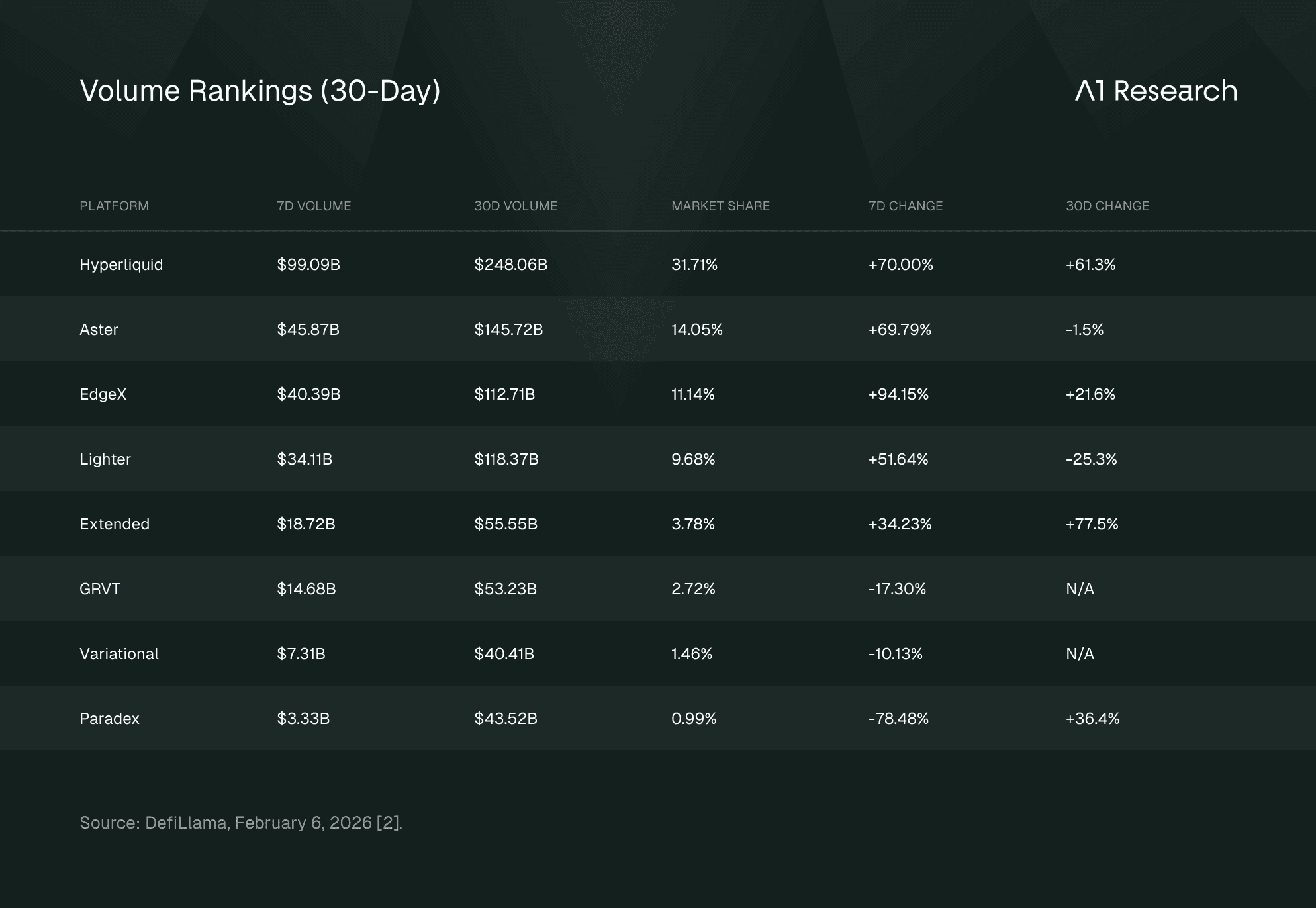

Source: DefiLlama, February 6, 2026.

Paradex's inclusion in the volume table above requires context. Its -78.48% 7d volume decline, the steepest in the cohort by a wide margin, coincides with the transition from Season 2 to Season 3 of its incentive program (February 1, 2026), a pattern consistent with the volume compression typically observed during airdrop season transitions as farming-driven activity resets. The 30d figure of $43.52B and the +36.4% 30d growth rate provide a more reliable picture of organic trajectory than the distorted 7d snapshot. That said, the magnitude of the 7d drop raises legitimate questions about what proportion of Paradex's volume is incentive-dependent versus organic, a question that will be answered definitively only after TGE when incentive structures normalize.

Source: DefiLlama, February 6, 2026.

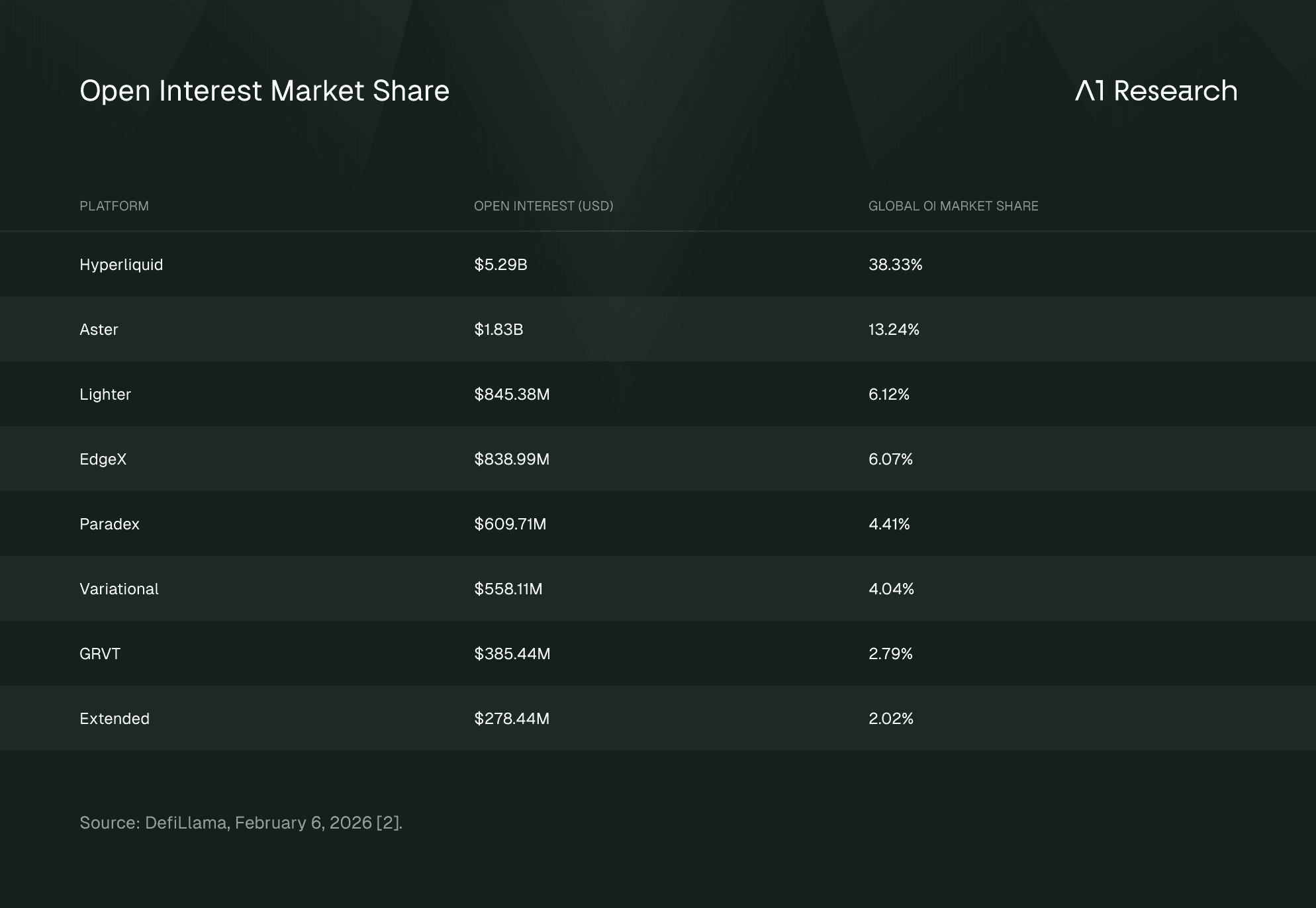

Hyperliquid maintains the dominant position, accounting for over 38% of global OI among tracked derivative protocols. The concentration reflects both genuine liquidity depth and market maker capital committed to the platform. The drop-off from Hyperliquid to the next tier is steep: Aster holds 13.2%, while the remaining six platforms each account for less than 7%. Aster's second-place OI position ($1.83B) deserves particular scrutiny given its temporary DefiLlama delisting for wash trading patterns. Even after discounting for potential artificial inflation, the absolute scale of capital locked on Aster is difficult to dismiss entirely: maintaining $1.83B in open interest requires real collateral deposits regardless of volume manipulation. The platform's BNB Chain integration (78% of TVL), tokenized stock offerings, and multi-chain deployment across four networks give it genuine structural advantages in accessibility and asset coverage that explain at least some of this capital commitment.

Source: DefiLlama, February 6, 2026.

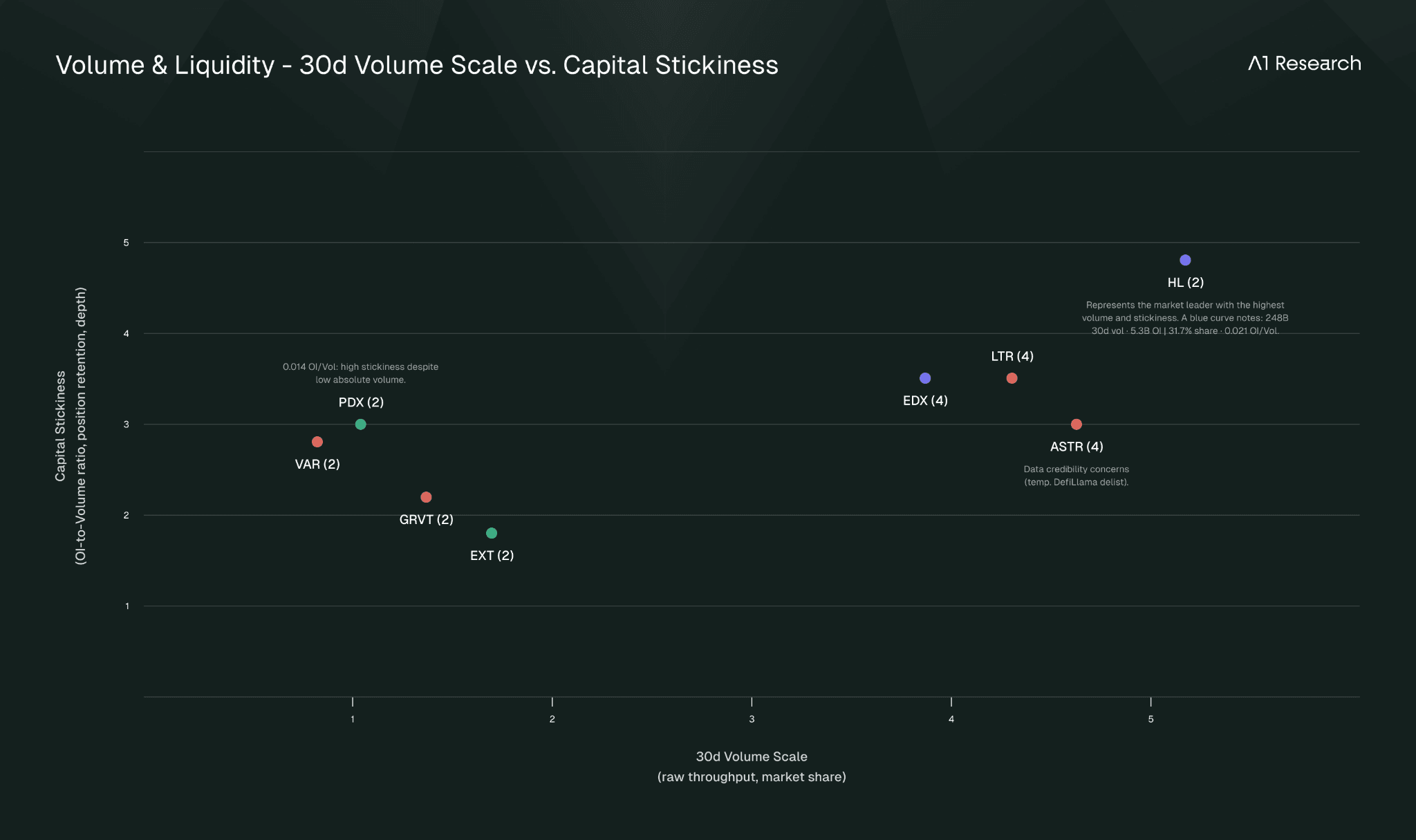

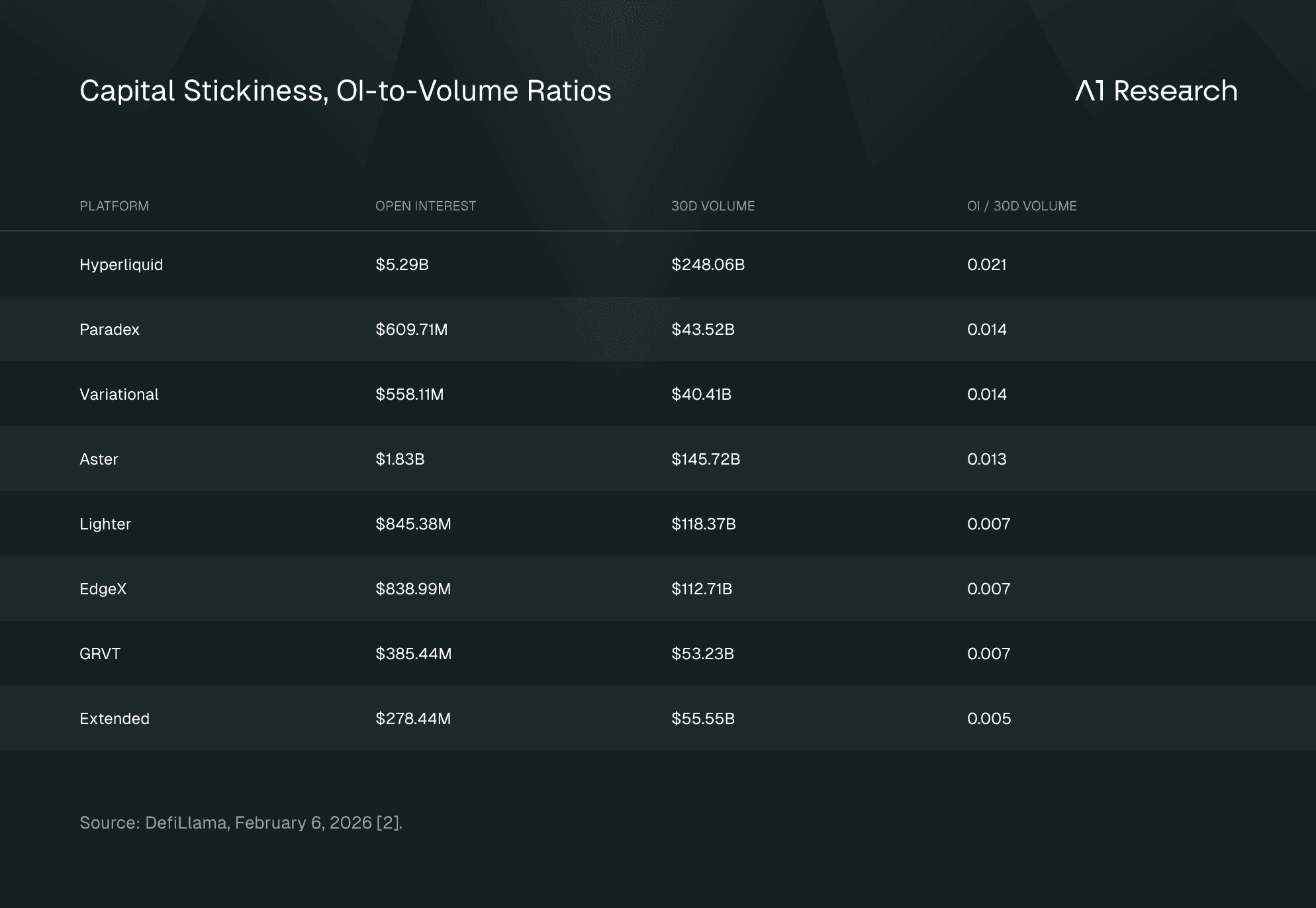

The OI-to-30d-Volume ratio is the most revealing metric in this analysis. It measures stickiness: how much open interest is held relative to trading churn over a meaningful timeframe. Higher ratios indicate genuine position-holding; lower ratios suggest high-frequency activity or airdrop farming. Using 30-day volume rather than 24-hour snapshots smooths out single-day anomalies such as the February 5 crash, which inflated daily volumes across most venues and distorted short-term ratios.

The cohort splits into three tiers. Hyperliquid (0.021) stands alone at the top, reflecting the deepest liquidity pool and most committed market-making capital in the cohort. Paradex (0.014) and Variational (0.014) form the second tier alongside Aster (0.013), with ratios roughly 2x the bottom of the field, reflecting meaningful position retention from different sources: Paradex's institutional position-holding supported by privacy architecture and portfolio margin, Variational's RFQ model that naturally encourages longer hold times, though Aster's position warrants additional scrutiny given its temporary DefiLlama delisting for wash trading concerns. The bottom tier of Lighter (0.007), EdgeX (0.007), GRVT (0.007), and Extended (0.005) suggests significantly higher proportions of incentive-driven churn or short-duration trading relative to standing positions.

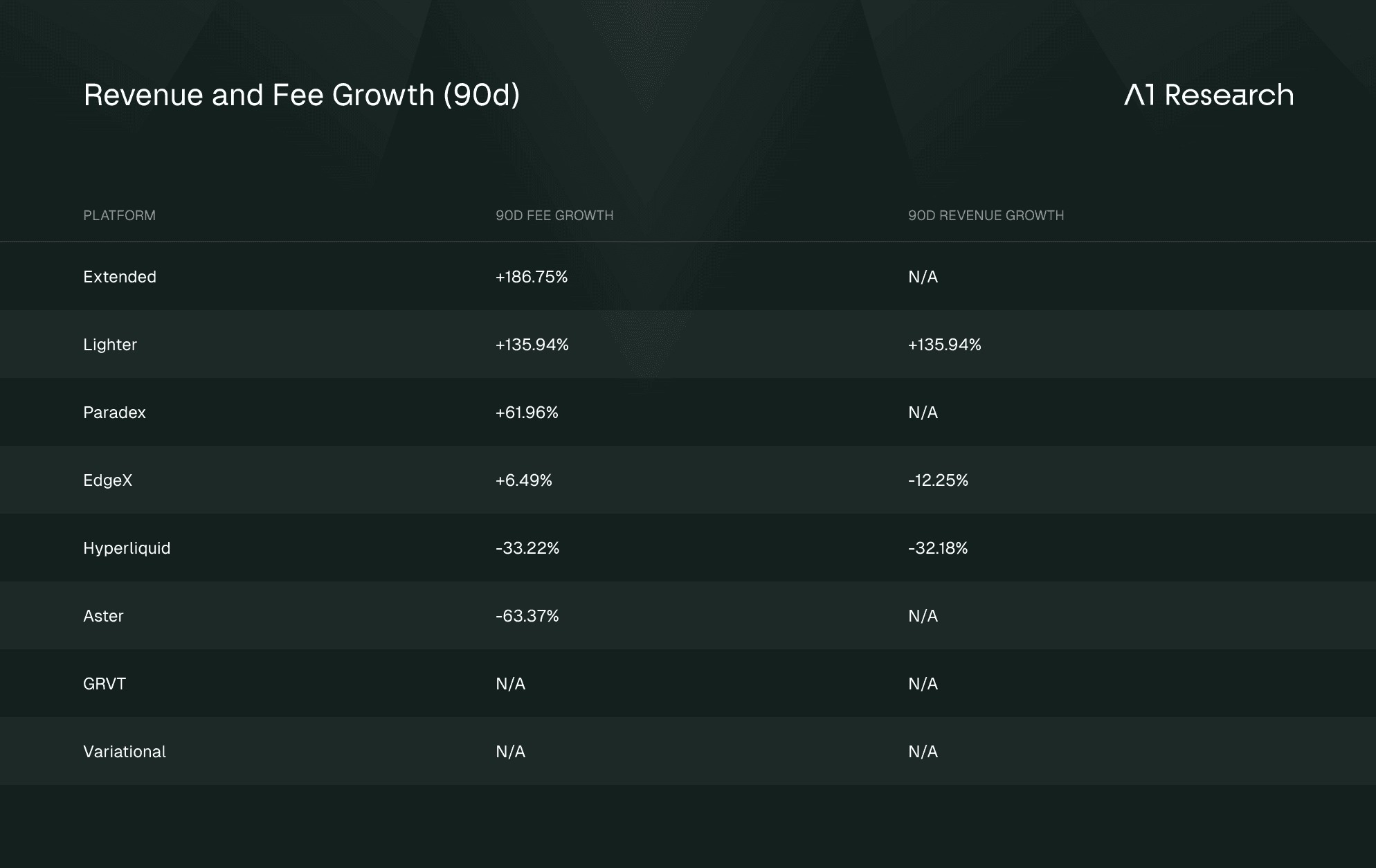

Source: DefiLlama, February 8, 2026. Revenue reflects protocol-level revenue after token holder distributions or buybacks where applicable; N/A revenue indicates pre-TGE platforms without live revenue-sharing mechanisms (Extended, GRVT, Paradex, EdgeX). Lighter's 1:1 fee-to-revenue ratio suggests full protocol retention. EdgeX is the only platform showing positive fee growth alongside negative revenue growth, indicating margin compression. Hyperliquid's -33.22% fee decline reflects a 90-day window comparison against a period of peak activity rather than structural deterioration; Hyperliquid remains the largest absolute fee generator in the cohort at an estimated $200M+ monthly run rate. Aster's -63.37% fee decline aligns with its broader data credibility concerns noted elsewhere in this report. GRVT and Variational lack DefiLlama fee/revenue tracking integrations entirely: GRVT's fee data is explicitly marked as unavailable despite $53B+ in 30d volume, while Variational's peer-to-peer RFQ architecture and OLP spread-capture model are not indexed by DefiLlama's analytics framework.

Paradex's specific trajectory showed monthly volume growing from ~$8B (July 2025) to ~$32B (December 2025) to $43.5B in 30-day volume by February 2026, representing sustained 5x+ growth over seven months. Extended leads 90-day volume growth at +185.75%, the strongest long-term momentum in the cohort.

Stress Test: October 10, 2025

On October 10, 2025, President Trump announced 100% tariffs on Chinese imports, triggering a synchronized selloff across global risk assets. The NASDAQ fell 3.6% and the S&P 500 dropped 2.7% before the contagion spread to crypto markets, which, trading 24/7 without circuit breakers, absorbed the full force of the move. BTC declined approximately 14% intraday from around $122,000 to $105,000, while ETH fell 12-20% depending on the venue, and average token declines across the CoinDesk Data universe reached approximately 47%, surpassing the May 2021 crash. The result was the single largest liquidation event in crypto history: $19.1-19.3 billion liquidated across 1.6 million traders within 24 hours, approximately nine times larger than any previous single-day total. Of the total, roughly $16.7 billion were long positions, a 5:1 long-to-short ratio reflecting how completely the market was positioned for continuation. Total perpetual futures open interest across major exchanges contracted 43%, falling from $217 billion to $123 billion. The single largest known liquidation was a $200 million ETH-USDT long on Hyperliquid. On the other side of the crash, a trader known as the "Hyperunit whale", later linked by on-chain analyst Eye to former BitForex CEO Garrett Jin via ENS domains ereignis.eth and garrettjin.eth, had opened over $1 billion in BTC and ETH shorts on Hyperliquid ($735 million BTC, $353 million ETH) just minutes before the tariff announcement, netting an estimated $190-200 million in profit within 24 hours. The timing fueled insider trading speculation, though no evidence of improper conduct has emerged; Jin denied ownership of the wallet, stating "the fund isn't mine, it's my clients'". In a bitter reversal, the same trader subsequently built an ETH long exceeding $700 million (reaching $730 million by mid-January with combined exposure across ETH, SOL, and BTC exceeding $900 million), only to exit in early February 2026 with a total loss of approximately $250 million as ETH declined sharply, leaving the Hyperliquid account with $53 according to Arkham Intelligence.

The outcomes varied sharply across platforms, with each architectural choice producing distinct, measurable consequences.

Hyperliquid experienced its first-ever Auto-Deleveraging (ADL) event, a significant milestone for a platform whose three-tier waterfall (market orders, HLP backstop, ADL) was designed to absorb toxic positions without forcing profitable traders out. An academic analysis of the event documented $2.1 billion in positions closed via ADL within just 12 minutes. Hyperliquid's open interest contracted 57%, the most severe contraction in the cohort, falling from $14 billion to $6 billion as leveraged positions were forcefully unwound. Despite the ADL activation, HLP ultimately ended the day with approximately $40 million in profit from advantageous settlement of the toxic positions it absorbed. The event revealed a structural vulnerability in fully transparent orderbooks: because all positions and liquidation prices are visible on-chain, the crash coincided with observable clustering of liquidations at key price levels, consistent with the "liquidation MEV" dynamic where informed participants profit from triggering cascading forced closures. In the weeks following October 10, Hyperliquid lost nearly 50% of its open interest, suggesting that aggressive ADL activation, while preserving platform solvency, carried significant costs in trader confidence and capital retention.

Lighter suffered the most acute operational failure in the cohort. The exchange experienced a 4.5-hour outage (approximately 10:30 PM to 3:00 AM EST, October 10-11) as its single sequencer crashed under approximately 79.8x normal transaction load, compounded by database index corruption that required manual recovery. The outage resulted in the loss of three transaction batches and prevented users from managing or closing positions during the crash. The total damage was approximately $50 million: $25 million in trader losses during the outage (many of which were likely unsalvageable given the speed of the move), $21.5 million in LLP losses (a 5.35% drawdown), and an additional $7 million in losses from a post-crash sequencer disruption. Lighter subsequently distributed points as compensation. For a platform built on the premise of ZK-rollup reliability and Ethereum settlement security, the outage raised questions about the gap between theoretical architecture and production resilience under extreme conditions. The Beosin post-mortem identified two core architectural vulnerabilities: the single sequencer creating a single point of failure, and the ZK-SNARK proof generation pipeline lacking resource reservation for high-priority operations like liquidations.

Paradex benefited from its privacy architecture as a structural buffer. Because liquidation levels were not publicly visible, the coordinated liquidation hunting behavior observed on transparent venues was structurally impossible. The socialized loss model (which was not triggered during this major event) would have meant no profitable traders were forcibly deleveraged, preserving portfolio integrity for hedged positions, precisely the "portfolio blindness" problem that ADL would have introduced on other platforms.

GRVT was relatively insulated for several reasons: its open interest and volume were substantially smaller than Hyperliquid or the major CEXs, meaning less absolute liquidation pressure; the GLP vault was still in its six-month backtest phase and was not publicly deployed; and GRVT's Validium-derived privacy provided a similar shield against liquidation hunting as Paradex, though at smaller scale. Coincidentally, GRVT launched its Earn on Equity program on the same day as the crash, which may have attracted fresh capital precisely as other platforms faced outflows. The limited stress exposure means GRVT's liquidation infrastructure remains largely untested under genuine duress, a meaningful unknown for a platform whose $53.23B in 30d volume and $385M OI are pre-TGE figures with unknown incentive dependency. The -17.30% 7d volume decline on the February 6 snapshot, while less dramatic than Paradex's seasonal drop, warrants the same analytical scrutiny: until TGE clarifies organic retention, GRVT's volume profile carries the same incentive-uncertainty discount applied elsewhere in this report.

Variational's OLP faced a different stress vector entirely: the speed of the move created hedging lag that risked hedging costs exceeding spread revenue, a structural vulnerability inherent in the single-counterparty model where external hedging must keep pace with internal position changes. The core risk is quantifiable in principle: when implied volatility expands faster than the OLP can execute offsetting positions on external venues (Binance, Bybit, other DEXs), each second of lag translates into unhedged directional exposure. During October 10's peak liquidation cascade, BTC moved roughly 3-4% within minutes, meaning even 10-30 seconds of hedging delay could produce losses exceeding the entire spread captured on the underlying retail flow. The OLP's P&L during the event has not been publicly disclosed, leaving an open question about whether the single-counterparty model can sustain itself through tail events or whether it requires periodic recapitalization that would undermine the zero-fee value proposition.

The aftermath was sobering for the entire market. Post-crash liquidity across perp DEXs reached its thinnest levels since mid-2022, as market makers widened spreads and reduced posted size across venues. Stablecoin markets were also rattled, with Ethena's USDe depegging to approximately $0.65 on Binance, triggering secondary liquidation cascades across LSDs and alt-L1s. The October 10 event served as a natural experiment that revealed which architectural trade-offs were theoretical and which were operationally consequential: the three-tier waterfall was exhausted, the socialized loss model held, the single-sequencer ZK-rollup broke, and privacy provided a measurable structural buffer against predatory liquidation behavior.

8. Risk Assessment

Hyperliquid. Validator concentration on a custom L1 with no Ethereum settlement fallback remains the primary architectural risk: in a catastrophic consensus failure, there is no external settlement layer to fall back to. The October 10 ADL activation (see section 7) demonstrated concrete limits to the three-tier liquidation waterfall, with $2.1B in positions closed via ADL within 12 minutes and nearly 50% open interest loss in subsequent weeks. HLP vault depositors function as implicit insurers of last resort during liquidation cascades, a risk further illustrated by the March 2025 JELLY incident, where forced delisting and non-market settlement at $0.0095 (versus ~$0.50 market price) raised centralization concerns about operator intervention capabilities. Full transparency of all positions and liquidation levels creates structural exposure to liquidation MEV. The B2B infrastructure pivot is strategically sound but introduces ecosystem development execution risk across HIP-3, HIP-4, and the broader builder network.

Paradex. The centralized sequencer retains full order flow visibility during matching, and per L2BEAT, there is no mechanism to force transaction inclusion if the sequencer is down or censoring. Contracts are instantly upgradable with no exit window for users in case of unwanted upgrades, governed by multiple multisig configurations (2/4, 2/5, and 3/6 thresholds across different system components). The Privacy Council's 1-of-3 decryption threshold creates a dependency for encrypted state recovery. Volume concentration risk is evidenced by the -78.48% 7d decline during the Season 2 to Season 3 incentive transition, raising questions about organic volume share pre-TGE. The socialized loss model preserves portfolio integrity during extreme events but creates withdrawal penalty risk that could theoretically accelerate outflows during a crisis.

Lighter. The October 2025 outage (see section 7) is the most consequential risk event in Lighter's history: 4.5 hours of downtime under stress, $50M in user impact, and two architectural vulnerabilities exposed (single-sequencer dependency and ZK-SNARK proof pipeline resource contention). For a platform whose value proposition rests on ZK-rollup reliability and Ethereum settlement security, the gap between theoretical architecture and production resilience under extreme conditions remains the central concern. The mandatory 1:10 LIT staking requirement (January 2026) may constrain LP participation and create friction for institutional capital. RWA markets depend on Chainlink oracle reliability for off-hours pricing, introducing external dependency risk for the platform's most differentiated product line.

EdgeX. The V2 migration from proven StarkEx infrastructure to a new modular multi-VM architecture (edgeVM + edgeEVM) represents meaningful execution risk: the current system works, and the replacement is unproven at scale. Per L2BEAT, the Validium DAC threshold has been flagged as potentially too low, and the data availability model changes in V2 could alter the privacy properties that currently derive from the Validium architecture. The centralized execution model means the operator retains full control over matching priority and transaction ordering.

Extended. The base-layer unified margin architecture is the most ambitious design in the cohort but remains unproven at scale with limited ecosystem adoption. Open interest ($278M) and volume ($55.5B 30d) are growing rapidly (+185% 90d volume) but from the smallest base in the cohort, creating fragility risk if growth stalls or incentive structures change. The Starknet stack migration from StarkEx is complete but the integrated lending market, which underpins the yield-bearing collateral model, has not been stress-tested under conditions comparable to October 10.

GRVT. ZKsync ecosystem dependency introduces shared infrastructure risk: the EmergencyUpgradeBoard (a 3/3 multisig of SecurityCouncil, Guardians, and ZkFoundationMultisig) can bypass the standard 4-8 day upgrade delay and execute upgrades immediately, while the chain admin operates under a 2/3 multisig threshold. The operator can manage transaction filtering via the TransactionFilterer, and there is no exit window for users in case of unwanted upgrades. Mandatory KYC is a feature for institutional adoption but creates friction for DeFi-native retail flow. Pre-TGE volume uncertainty remains the key unknown: $53B in 30d volume and $385M OI are impressive, but organic retention post-TGE is unproven.

Variational. The single-counterparty RFQ model concentrates all execution risk on the team-operated OLP, which must hedge externally in real time on CEX/DEX venues. During rapid price movements, hedging lag can produce unhedged directional exposure where losses exceed spread revenue, a vulnerability the October 2025 crash stress-tested directly (Section 7) without public P&L disclosure. The absence of any programmability layer or composability path limits long-term network effects, and the isolated per-trade settlement pool structure constrains capital efficiency relative to cross-margin alternatives.

Aster. The temporary DefiLlama delisting for wash trading patterns undermines data credibility and creates persistent uncertainty about what proportion of reported volume and OI is organic. Even after reinstatement, the platform lacks the transparent verification mechanisms (open-source ZK circuits, on-chain insurance fund visibility, proof-based settlement) that would resolve these concerns. Multi-chain liquidity fragmentation across four networks (BNB Chain, Arbitrum, Ethereum, Solana) dilutes depth on any single venue. The absence of privacy, programmability, or builder ecosystem features limits institutional appeal and long-term defensibility against architecturally more sophisticated competitors.

Systemic. Regulatory risk remains the most significant exogenous uncertainty across the cohort, with MiCA enforcement, FATF travel rule expansion, and potential OFAC action against onchain derivative protocols each capable of reshaping venue selection overnight (Section 8). Oracle risk affects all platforms, with Chainlink dependency concentrated in Lighter's RWA markets and Pyth/proprietary feeds carrying different trust profiles elsewhere. Liquidity fragmentation across 8+ competing venues may ultimately drive institutional consolidation onto fewer platforms, rewarding the venues that resolve the most institutional requirements rather than those with the highest current volume.

Regulatory Landscape and Platform Exposure

Regulatory positioning varies sharply across the cohort and is likely to become the primary driver of institutional venue selection over the next 12-24 months. Three regulatory vectors deserve specific analysis.

MiCA and Onchain Derivatives. The EU Markets in Crypto-Assets Regulation requires crypto-asset service providers (CASPs) to obtain authorization, implement governance standards, maintain capital reserves, and comply with market abuse provisions. Full enforcement in 2026 means any platform offering derivatives services to EU residents faces a compliance mandate. Onchain perpetual DEXs operating without a legal entity face a structural gap: MiCA does not exempt decentralized protocols, but enforcement against truly decentralized systems remains untested and jurisdictionally ambiguous. Platforms with identifiable operators have a clearer path to CASP authorization: GRVT's Bermuda Class M license and VASP status provide a ready-made compliance framework, while Paradex's centralized sequencer entity and EdgeX's institutional-facing structure offer potential authorization paths. Fully permissionless architectures without identity layers, notably Hyperliquid and Variational, face the most ambiguous regulatory exposure and would require fundamental architectural changes to satisfy MiCA requirements.

FATF Travel Rule vs. Privacy Architectures. The FATF travel rule requires Virtual Asset Service Providers (VASPs) to collect and transmit originator and beneficiary information for transfers above jurisdiction-specific thresholds, typically $1,000, creating a direct tension with privacy-preserving execution. GRVT's mandatory KYC and VASP status already satisfy travel rule requirements by design, making it the most compliance-ready platform in the cohort. Paradex's architecture presents a nuanced case worth examining closely: position confidentiality protects against market participants but the centralized sequencer retains full visibility into all trading activity, enabling selective regulatory disclosure without compromising trading privacy. This "compliance trapdoor" model, where the operator can satisfy regulatory inquiries without exposing data to other market participants, could prove to be a sustainable path for privacy-preserving venues that need to operate within regulated frameworks. Hyperliquid's permissionless architecture with no identity layer would require fundamental changes to comply. The unresolved question is whether regulators will accept venue-level compliance (the operator can disclose when required) or demand protocol-level transparency (all data must be accessible on-chain), a distinction that would reshape the competitive landscape dramatically.

Tornado Cash Precedent and Smart Contract Sanctions Risk. OFAC's 2022 Tornado Cash designation and subsequent legal proceedings established that smart contract-based protocols can face sanctions enforcement, though the legal landscape remains contested following the 2024 appeals court ruling that narrowed the scope to immutable contracts versus operator-controlled systems. For perpetual DEXs, the distinction matters: all eight platforms in this cohort have identifiable operators and upgrade mechanisms, placing them more clearly within OFAC's enforcement reach than immutable contracts. The risk is asymmetric: platforms without compliance infrastructure (KYC, transaction monitoring, sanctions screening) face disproportionate exposure because they cannot demonstrate compliance even if required to. A single OFAC designation targeting an onchain derivatives protocol would likely trigger immediate institutional capital flight to licensed venues, consolidating flow onto GRVT and any platform that has obtained equivalent authorization by that point.

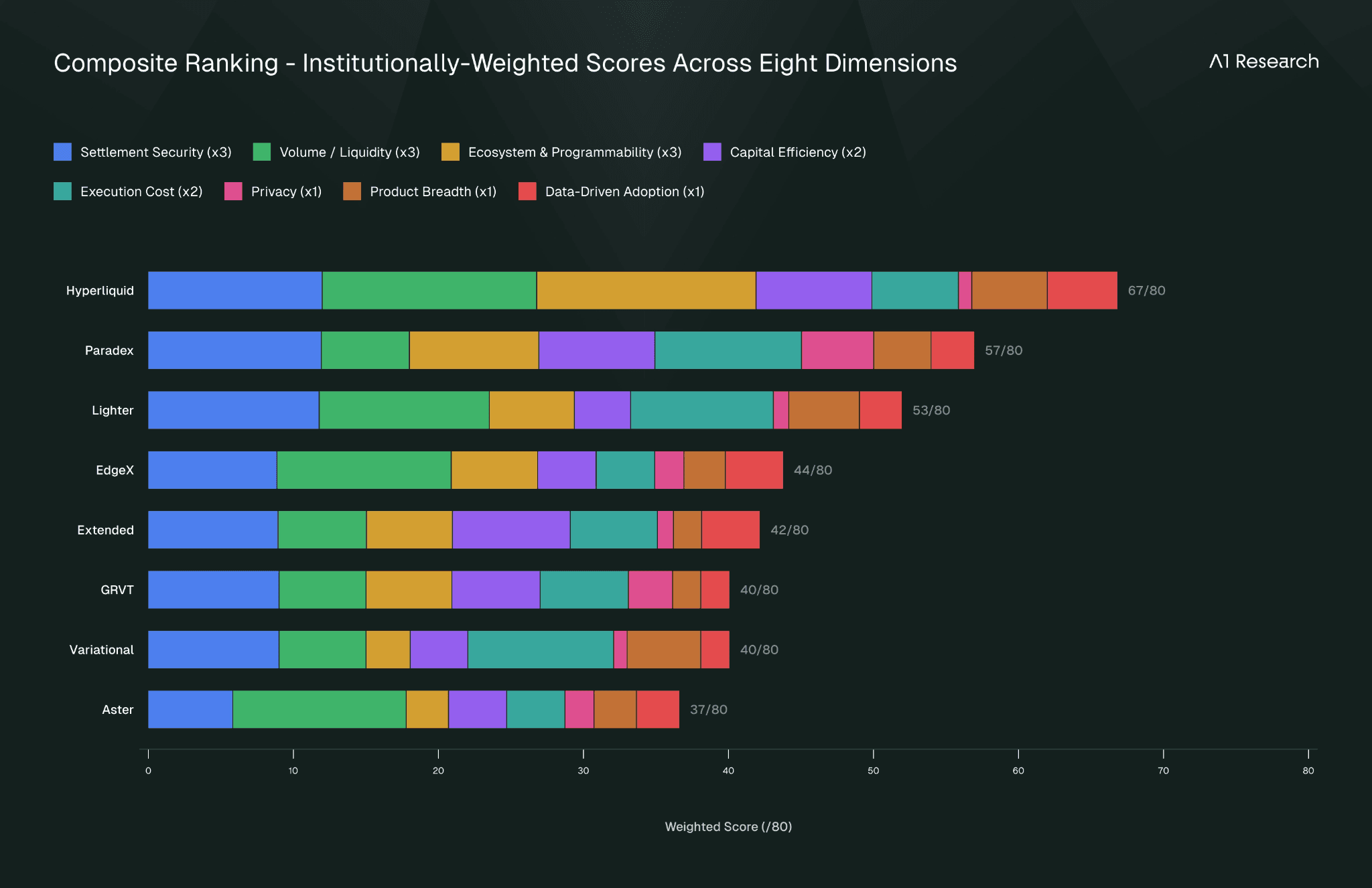

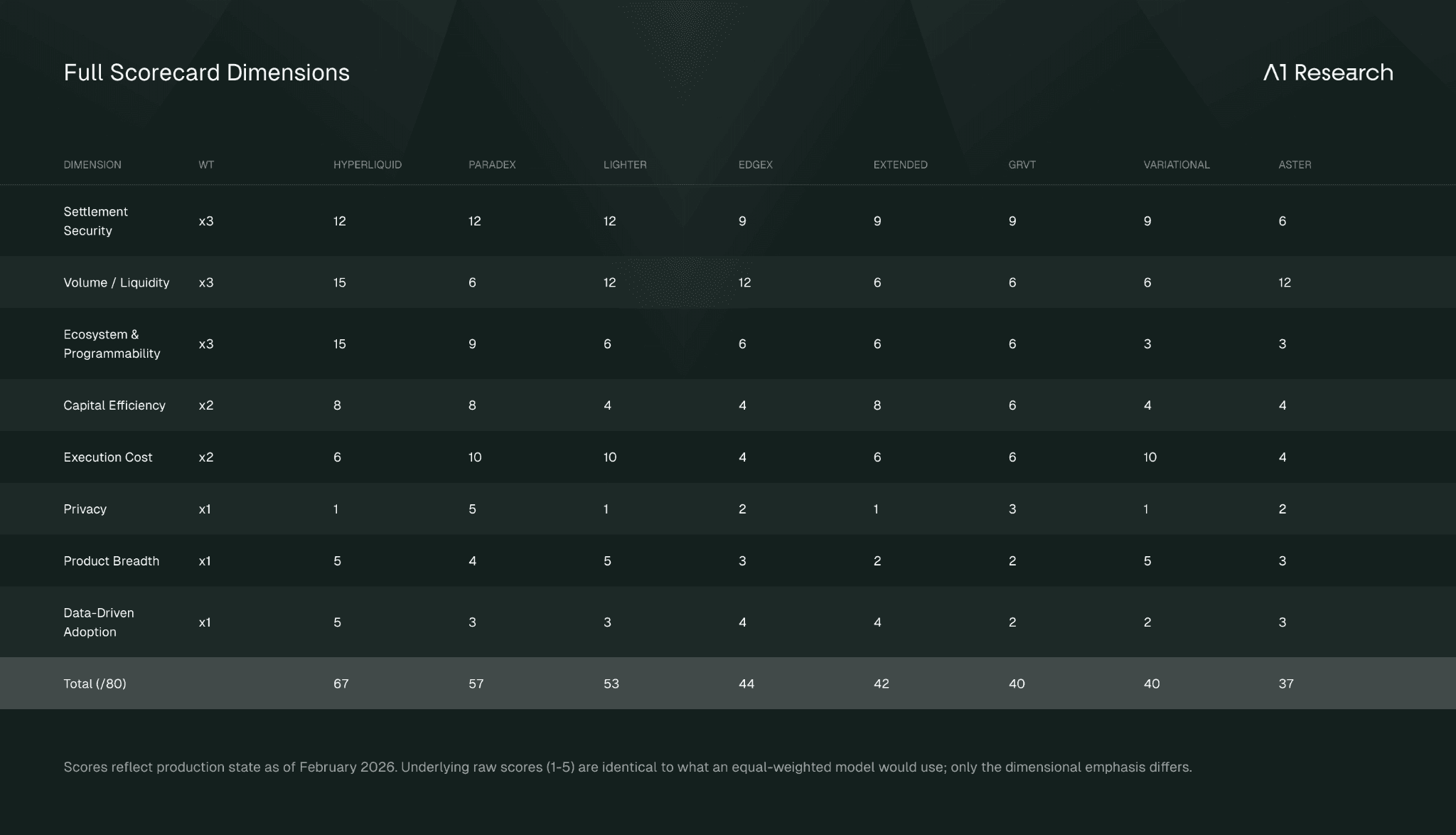

9. The Scorecard

Each platform is rated 1 (basic) to 5 (best-in-class) across eight dimensions, reflecting current production capabilities rather than roadmap promises. Dimensions are weighted in three tiers reflecting institutional allocator priorities: ×3 for non-negotiable infrastructure (settlement security, volume/liquidity, ecosystem and programmability), ×2 for core differentiators (capital efficiency, execution cost), and ×1 for long-term considerations (privacy, product breadth, data-driven adoption). The weighting reflects how institutional allocators actually select execution venues: safety of funds and ability to enter/exit at size are table stakes, margin optimization and total cost of carry drive venue selection, and privacy, product range, and growth trajectory inform longer-term allocation decisions.

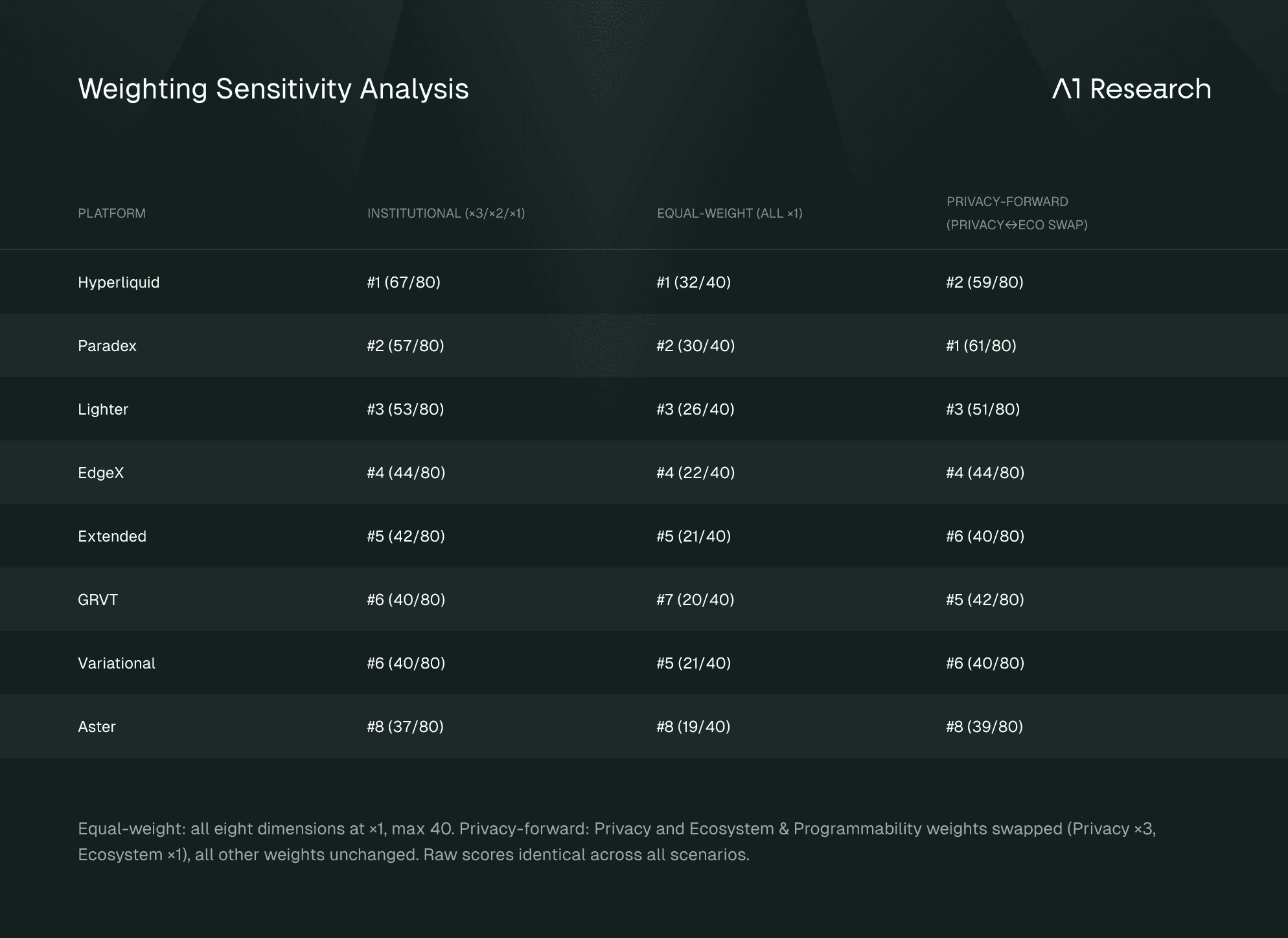

Methodology limitations. Three constraints should inform how readers use this scorecard. First, the 1-5 ordinal scale compresses order-of-magnitude differences: the gap between Hyperliquid's volume (5) and Paradex's (2) represents a roughly 6x difference in 30d volume and a 40x difference in market share, information that a three-point spread does not convey. Second, all data reflects a single snapshot (February 6, 2026), and point-in-time bias is unavoidable; the Paradex 7d decline coinciding with its incentive transition and the GRVT 7d decline are both likely transient but cannot be confirmed as such within this methodology. Third, the ×3/×2/×1 weighting tiers are an editorial judgment, not a mathematical derivation. The logic is sequential: institutional allocators treat safety of funds and ability to enter/exit at size as binary gatekeepers (×3), a venue that fails on either is excluded before other dimensions are evaluated. Cost structure and margin optimization drive venue selection among qualified platforms (×2). Privacy, product range, and growth trajectory inform longer-term allocation timing (×1). Reasonable allocators may weight differently, and the sensitivity table below demonstrates how rankings shift under alternative frameworks. We present the institutional weighting as our primary lens while publishing the raw scores so readers can apply their own.

Equal-weight: all eight dimensions at ×1, max 40. Privacy-forward: Privacy and Ecosystem & Programmability weights swapped (Privacy ×3, Ecosystem ×1), all other weights unchanged. Raw scores identical across all scenarios.