Perpification is what happens when financial nihilism meets infrastructure that lets you lever anything, in a world that won't sit still.

Executive Summary

The visible symptom: Crypto's market structure has inverted, and the same pattern is leaking into every regulated venue.

The actual driver: A generation that feels economically locked out is choosing instruments that match a world too volatile to hold.

The cultural answer: Crypto skipped options because perps are what TradFi would have built without fifty years of regulatory plumbing.

The structural argument: Calling this gambling is a category error; the only thing that matters is whether the rake extracts or routes.

What comes next: AI agents make every niche market tradeable, and the volatility that drove perpification compounds into something much larger.

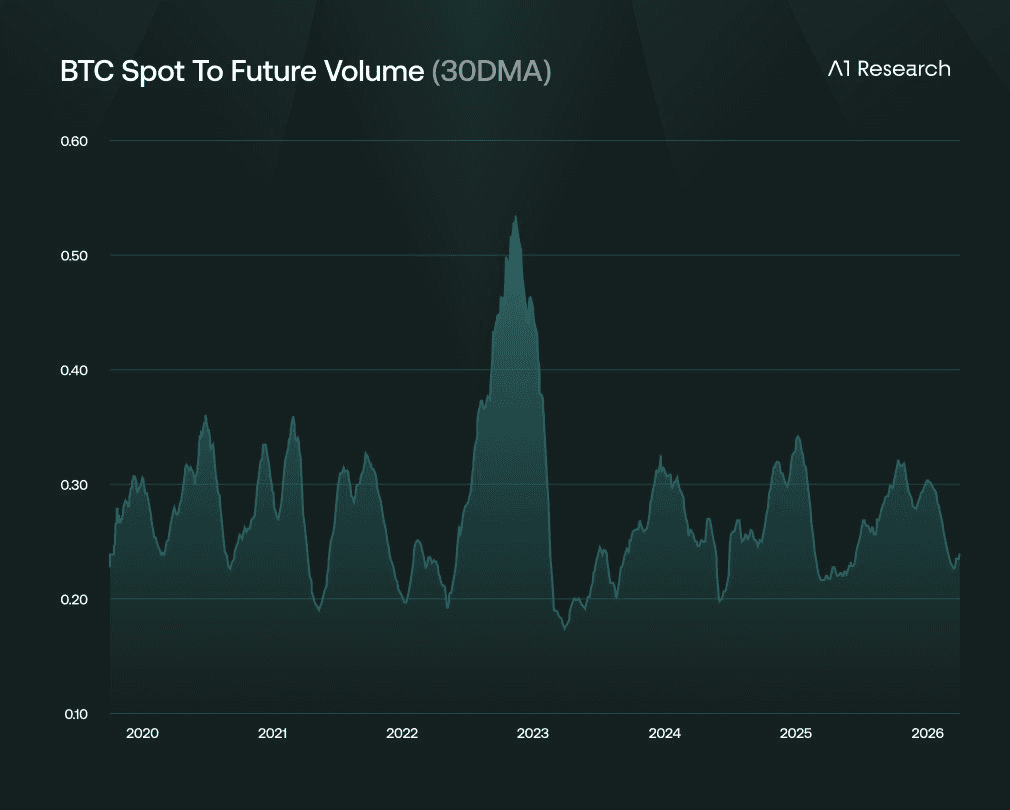

1. Spot Is Dead

BTC perp volume runs 5x spot. Most people on CT have stared at this number so long they've stopped seeing it.

That's the problem.Five times. Think about what that ratio means. It's not derivatives layered on top of a healthy spot market. It's a market structure where holding the underlying is a niche behavior and trading the synthetic is the default. The spot market is now a feed. The thing we used to call "the market" is the reference price for the actual market.

This isn't a crypto phenomenon anymore. The evidence is piling up:

Polymarket and Kalshi launched US perps the same day (April 21, 2026), with Polymarket's tagline shifting from "we price the future" to "now you can lever it"

HIP-3 cracked the door on real-world asset perps and Hyperliquid silver hit $1B in daily volume in early 2026

During Iran tensions, Hyperliquid did over $1B in oil over a single weekend, while every TradFi venue sat closed, watching crude move 30% from Friday to Monday open

Every good is becoming a perp.

That's the line worth sitting with. A perp, unlike a spot position, lets you make money whether the price goes up or down. In a spot world, volatility is a tax. You're long, price drops, you bleed. In a perp world, volatility is the entire product. Direction is one bit of information. Magnitude is the whole game. Being short oil during Iran is the same trade as being long. Being short Tesla during a tariff scare is the same trade as being long during the rip.

The world right now produces more volatility per quarter than at any point most of us have been alive for. AI repricing labor markets in real time. Geopolitical realignment generating weekly tail events. Currency debasement now showing up in portfolio construction documents, not just niche substacks. The Fed isn't even the only meaningful actor in your P&L anymore. The Pentagon, OpenAI, and TSMC's fab schedule all show up on the tape.

Volatility is the fuel.

Buy-and-hold was a strategy for a world that ended sometime around 2021-2022 and we're only now writing the obituary. To understand why perpification is spreading and accelerating, you have to start with the demand.

2. Financial Nihilism Is the Correct Read

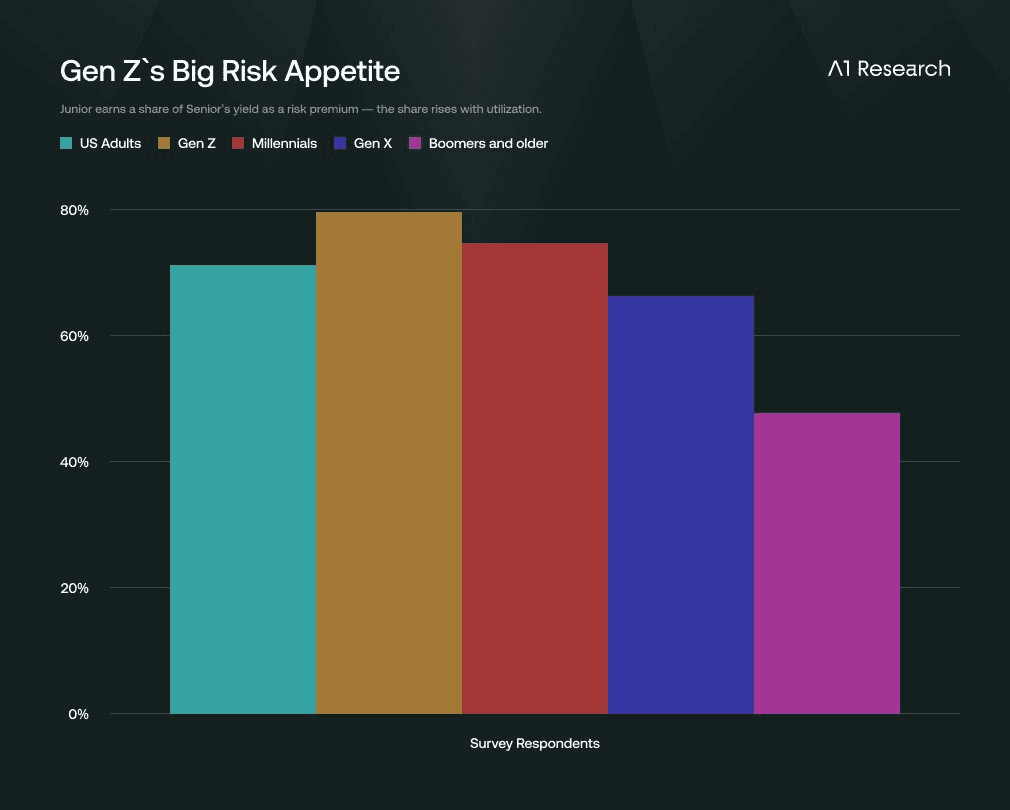

Northwestern Mutual ran the numbers in early 2026. 80% of Gen Z investors using high-risk assets explicitly said they're using them because they feel financially behind. 73% of all US adults using speculative instruments said the same thing. Bloomberg called it "financial nihilism." David Pakman at Consensus Hong Kong, more accurately, called it economic nihilism, and pointed out it isn't nihilism in the philosophical sense at all. It's a calculated response to structural barriers in wealth-building.

Run the math, any 28-year-old with a finance brain has already run it: six figures of student debt, a median home in any tier-1 metro requires capital they don't have and won't accumulate at the rate wages are growing. The institutionally-blessed wealth-building product is the S&P 500 at 8 to 10 percent annualized. At those returns, the gap between where they are and where they need to be doesn't close in their working life. It widens.

If the conventional path can't deliver, the rational play is to reach for instruments that can.

Even if the expected value is worse. Even if variance is brutal. The upside distribution is the only one that contains a path to the goal. This isn't a gambler's fallacy. It's correctly identifying you're not in a game you can win by playing more conservatively.

The version of this argument that gets repeated on CT is "the system is broken, so we apes." Right but lazy. The sharper version: the demand for leveraged, fast, asset-agnostic exposure isn't crypto-coded. It's global. We're just the segment that built the cleanest rails for it.

Different rails, same demand:

Cboe data: retail accounted for over 60% of US options volume in 2025

0DTE phenomenon: structurally a leverage product for retail thinking in hours, not quarters

Global FX/CFD volume: hit $30 trillion monthly in 2025, up 3x in a decade (60% Asia-Pacific)

US retail futures volume: sits 50% above pre-pandemic levels

Same answer to the same question, which is: given the volatility regime we're actually in, what's the right retail strategy?

The answer the entire global retail cohort has converged on, independently, across jurisdictions, is to trade the volatility instead of trying to hide from it. Buy-and-hold is a strategy for a stable world. We don't live in one.

Which raises a question CT under-discusses. If the demand is the same, why did TradFi build options and we built perps?

3. The Cultural Gap That Made Perps Inevitable

Crypto skipped options. Not because Deribit doesn't exist. It's existed for years, the product is solid, the order books are deep enough. Most of CT can't tell you what gamma is and doesn't care.

The honest answer is that perps are a cleaner instrument for the actual demand, and options were never the right tool. They were the only tool TradFi had built.

Compare the cognitive overhead. To trade a 0DTE call on SPY, you have to pick a strike, manage theta over the day, reason about IV versus realized, and time the close before expiry. To trade a perp on anything, you pick direction and leverage. That's the entire decision tree. Set your liquidation level by setting your size. Done.

This points at a distinction nobody draws cleanly. Options sell volatility. Perps sell direction. TradFi conflated these because options were the only legal retail leverage product, so retail traders who wanted directional exposure were forced to express it through a vol instrument. The result is millions of TradFi retail traders explaining their positions in vol terms when what they actually wanted was direction. Just direction.

Crypto's cohort, given a clean choice, picked perps decisively. It wasn't close. The cultural verdict is in the data: 6x perp-to-spot ratio, 86 trillion dollars in annual perp volume, every major retail-facing crypto interface built around the perp orderbook.

This is also why perpification of everything is happening on these rails and not, say, 0DTE-ification of everything. Crypto's cohort revealed something about the underlying demand that TradFi's regulatory plumbing had been hiding for fifty years. People don't want vol exposure dressed as leverage. They want leverage. As clean an instrument as possible.

If perps are the cleaner instrument, the next question is whether the elegance is load-bearing or just window dressing for what is, structurally, the same thing as everything else.

4. Everything Was Always a Perp

You don't need a perps explainer. Skip ahead if you want. The only thing that matters here is the Paradigm reframe at the end.

Quick mechanics anyway, in case you want to send this to someone who needs them. A perp tracks spot. No expiry. Kept aligned via a funding rate longs and shorts pay each other when mark drifts from index. The funding rate is a feedback control system: the further the drift, the bigger the corrective payment. Same logic as a thermostat.

The design choice that matters: liquidity concentrates in one orderbook. Compare to options markets, where every additional strike and expiry splits available liquidity into a thinner pool. A BTC perp market has one book. A BTC options market has hundreds. Single-book structure means tighter spreads, more volume, deeper liquidity, and a flywheel that fragmented options markets structurally cannot match. This is the actual reason perp DEXs scale and options DEXs perpetually struggle, despite a decade of trying.

Now the actual point.

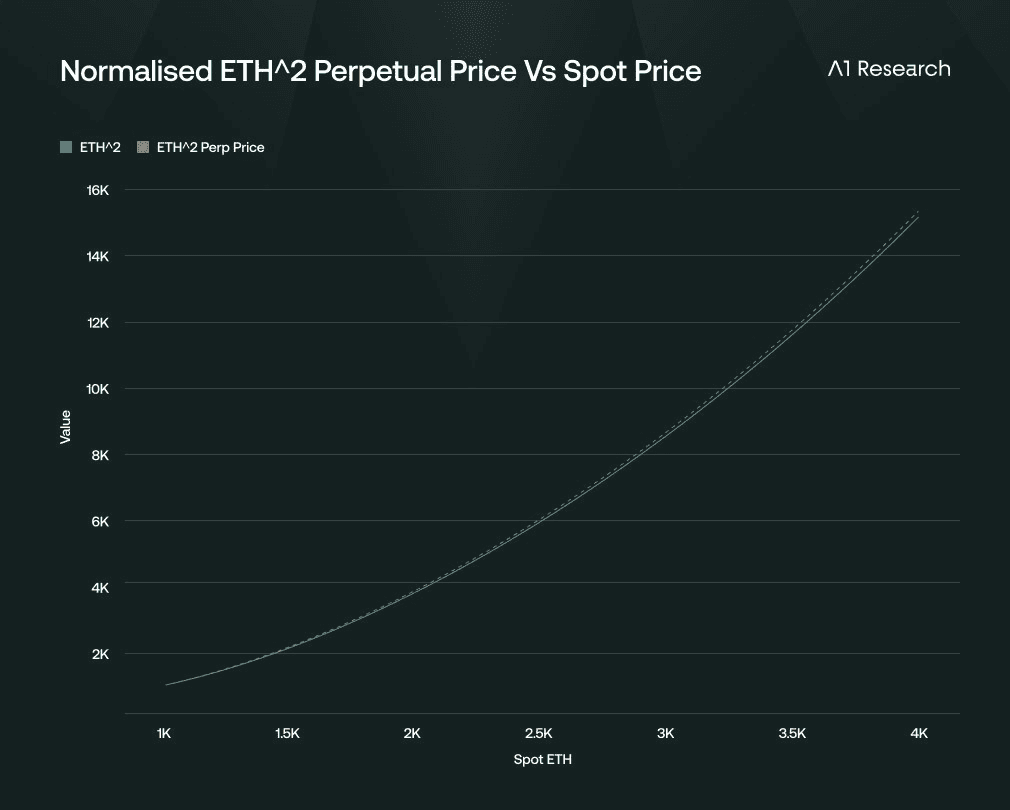

In 2024, Dan Robinson and the Paradigm team published a paper that recolors everything. Their claim, which I think is the most important conceptual move in DeFi this decade: stablecoins, margined futures, and AMMs are all power perpetuals at different exponents.

Crypto-collateralized stablecoins like DAI? Zero-power perpetuals. Margined futures like dYdX? 1-power perpetuals. Constant-product AMMs like Uniswap? Replicating portfolios for 0.5-power perpetuals. Squeeth? 2-power perpetual.

The entire DeFi stack: collateralized lending, derivatives, automated market making. All power perps at different exponents.

This isn't a metaphor. It's math. The collateral ratio, funding mechanism, and liquidation logic that defines a perp is the same machinery that defines DAI. A funding rate keeping a stablecoin pegged to a dollar is a 0-power perp's funding rate. The Uniswap LP position's payoff curve is the replication of a 0.5-power perp.

Perps aren't a crypto product that happened to spread. They're the underlying primitive that finance has been building variations of for decades, finally exposed in their general form because crypto stripped away the legacy plumbing that hid the structural identity.

Once you see it, you stop asking "why are perps eating spot." You start asking why it took this long for the underlying primitive to become the visible product.

The warning is the same warning that's always been there. At 10x, a 9.5% adverse move wipes you out. Cross-margin cascades during flash crashes. ADL forcibly trims winners when bankrupt liquidations exceed insurance fund and HLP buffers.

The 10/10 cascade in 2025 was a real event that real people lost real money in.

The mechanics that make perps elegant make them brutal at scale.

But here's the question of the elegance forces.If perps are the underlying primitive, then stablecoins, AMMs, and margined futures are all variations of the same machine.

Why does the financial press keep treating the crypto versions as gambling and the legacy versions as finance?

5. The Category Error

It's a category error. Once you see it, you can't unsee it. Once enough people see it, the regulatory frame collapses.

Here's the structural identity Lauris (@lzminsky) laid out cleanly. A casino bet: wager a dollar on red, receive two dollars if outcome occurs. A call option: pay a dollar premium, receive two dollars if strike condition is met. These are the same equation. Both are contingent claims. Both exchange present certainty for future contingency. Both have a market maker on the other side providing liquidity. The only thing that differs is the wrapper. Marble columns and a regulator-approved exchange license versus an Etherscan page and an audited smart contract.

Linguistic and cultural distinction, not structural.

Keynes said this. Schumpeter said this. Galbraith said this. The serious end of the economics profession has held this view for a century. The regulatory profession has built an enormous apparatus pretending otherwise, and the apparatus is now load-bearing for a system whose structural identity it can no longer credibly mask.

Then there's the historical scaffoldxbt2027 (@xbt2027) traced. Hyperfinancialization didn't start with crypto. It started in 1971, when Bretton Woods collapsed and the dollar detached from gold. Money became a pure symbol backed by trust. Two years later, in 1973, CBOE launched listed derivatives. From that moment, the financial system started building progressively more abstract claims on progressively more abstract underliers. MBS (Mortgage Backed Security) are derivatives of claims on real assets. CDS(Credit Default Swap) are derivatives on those derivatives. We've been trading signs about signs for over fifty years. Piketty's empirical work, return on capital running at 4 to 5 percent annually while real economic growth runs at 1 to 1.5 percent since the 1980s, quantifies the structural condition that makes financial nihilism rational.

Crypto didn't cause this. Crypto made it legible.

In every prior round of financialization, there was at least a fig leaf. A real asset somewhere at the bottom of the stack pretending to anchor the abstraction. With memecoins, the fig leaf comes off. The valuations are determined entirely by what xbt2027 calls the coordination game with iterated expectations: what other players believe other players will pay tomorrow. No Nash equilibrium. No anchor. Pure self-referential consensus.

The honest reaction to this isn't horror. It's recognition. The mechanism is the same one TradFi has been running for fifty years, just stripped of the comforting fiction that there was a real asset propping it up.

Now look at what's actually being built. Five and fifteen-minute crypto bets are doing 70 million dollars daily on Polymarket and Kalshi. Hyperliquid testnet has a recurring HYPE binary that settles every three minutes. Every major venue is converging on the same direction of travel: shorter, more repeatable, more monetizable cycles. Perps plus prediction markets plus memecoins are getting stitched into single interfaces, what FT called "gambling super apps." Same wallet, same screen. Sports outcome here, BTC binary there, microcap there.

Yes, it looks like gambling. Yes, it functionally is gambling. So is every options contract retail buys. So is the S&P. CFTC data suggests 80% of futures volume in major contracts is speculative, not commercial hedging. The line between investing and gambling is cultural, not mathematical, and it always has been.

Here's the structural difference that actually matters, which Lauris articulated and most CT hasn't fully internalized yet.

Traditional gambling is negative-sum because the rake extracts. Ten players bet 100 dollars each, casino takes 10%, 900 dollars redistributes among the players. Long-term, players lose. The system is designed to drain.

On-chain rails change this. Each wager can route into spot markets, deepening liquidity for the underlying. The rake doesn't drain. It routes. Every bet on a launchpad becomes a buy order that seeds liquidity. Every perp position generates funding flows and fees that recycle back into the protocol's economic loops. Speculation becomes the mechanism by which liquidity is injected, assets are distributed, attention is concentrated.

EV(network) = Σ EV(player) + EV(routing). When routing is positive, the network grows even as individual players lose. This is structurally different from Vegas. It's also structurally different from TradFi options markets, where the rake (spreads, broker fees, market-maker edge) extracts to off-chain entities that don't recycle the flow back into the underlying market.

This is the one thing TradFi commentators keep missing when they cover crypto-as-gambling. They're not wrong that it's gambling. They're wrong that gambling is necessarily negative-sum. The on-chain version has a different structural property than the Vegas version, and the structural property is the only thing worth arguing about.

The category error matters because it determines what gets built. Treat perpification as gambling and you regulate it like a vice. Push it offshore. Make it less transparent. Leave the human cost worse than under honest rails. Treat it as a financial primitive and you build transparent on-chain infrastructure with predictable rules and verifiable solvency. The argument isn't "speculation is good." It's "speculation is what's actually happening, at scale, on every rail, in every retail market, and the only question worth asking is whether we build for it honestly or pretend it's something else."

Polymarket changed its tagline from "we price the future" to "now you can lever it." That wasn't marketing. It was an admission. The rest of this is about what gets built once we stop pretending.

6. AI Eats the Loop

Everything above is the human version. Retail expresses demand, builders ship infrastructure, venues compete for flow. That version is already obsolete in the parts of the stack where it matters most.

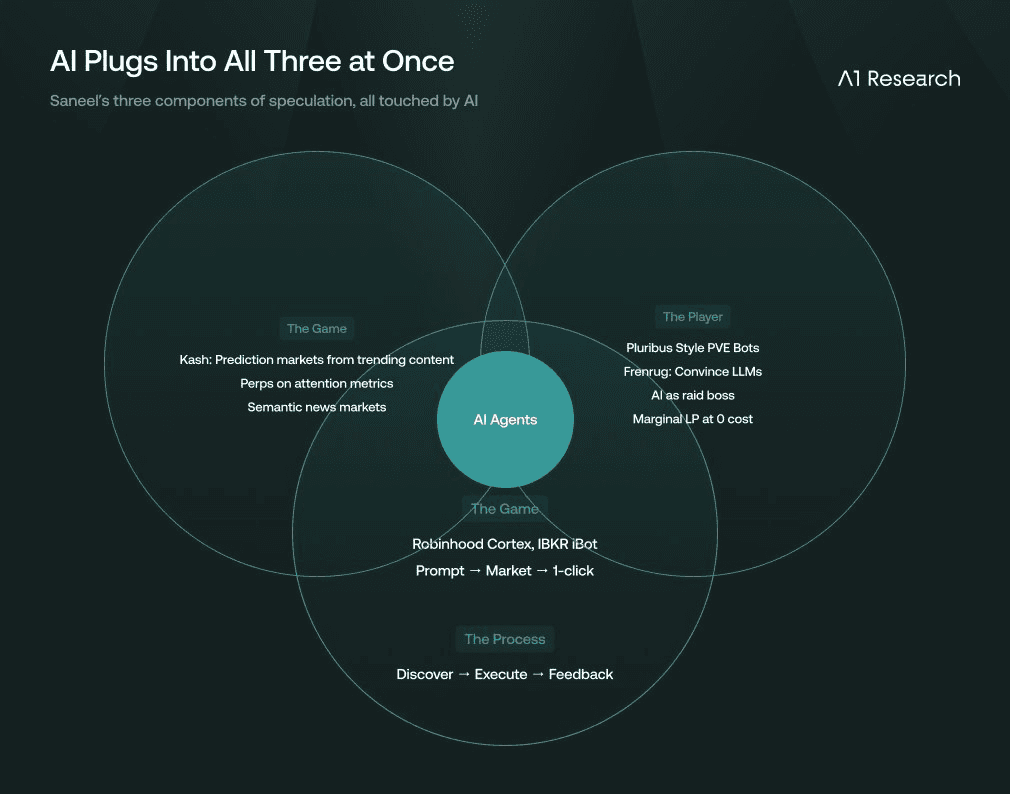

Saneel’s (@sanlsrni) deconstructed speculation cleanly. Three components.

The game : AI as market engineer: doesn't trade in markets, creates them (Kash spinning up prediction markets from trending content, perps on attention metrics, semantic markets like

The players : AI as participant: turns PvP speculation into PvE structures (pay to face the bot, stake on bot vs. players, AI raid bosses)

The process : AI as execution layer: compresses the arc from belief to trade (Robinhood Cortex, IBKR's iBot, natural-language trading interfaces)

As a market engineer, AI doesn't trade in markets. It creates them. Kash spins up prediction markets in real time from trending content. Perps on attention metrics already exist. Semantic markets like tmr.news are running. Once a model can identify a tradeable question and write the contract for it faster than a human can notice the question is interesting, the universe of available markets expands by orders of magnitude. HIP-3 deployers are scratching the surface of this. Every novel data feed becomes a potential perp market, and humans aren't the bottleneck on identifying which feeds matter.

As a player, AI changes what the games can be. Pluribus beat poker pros by bluffing more randomly. The implication isn't just "AI is good at poker." The implication is structural. Historically PvP speculation games can be turned into PvE structures. Pay to face the bot. Stake on the bot versus other players. Leaderboard tournaments against an AI raid boss. Frenrug was the early version, letting users try to convince LLMs to move financial value. The next version is novel modes of speculation that only exist because there's a non-human counterparty whose presence reshapes the game itself.

As a process, AI compresses the entire arc from belief to execution. Robinhood Cortex, IBKR's iBot, the natural-language trading interfaces shipping every month. The endpoint is the product Saneel described. Input any prompt, any belief, any piece of media. Get matched to the most suitable markets and trades. Execute in one click. The product that owns that flow is worth more than the products that own any single piece of it.

The most consequential thing AI does to perp markets is solve the long-tail liquidity problem.

Right now, perp markets exist for roughly a thousand tokens out of sixty million plus that exist, plus a few hundred RWAs. The bottleneck isn't infrastructure. It's that human market-makers aren't economical for niche markets. Spreads are wide. Volume is thin. Price discovery is bad.

Nick (@nickemmons) has the cleanest version of this argument.

AI agents have a marginal cost of attention approaching zero. They can monitor 100,000 markets at once, ingest specialized data the moment it publishes, execute on 1% edges, never get bored or tilted or distracted. For an AI agent, market-making "will TSMC's H100 capex exceed 40 billion dollars in 2026" is trivial. Every niche market that was previously uneconomic to run becomes viable. The TAM of correct-but-not-yet-priced information is vastly larger than what human traders can process.

This is what hyperfinancialization looks like as it lands. Not metaphorically. Literally.

Granular asset markets: instead of trading Apple, you trade Apple Services as distinct from Apple iPhone

Worldview vaults: deposit into the agent representing your thesis (accelerationist, doomer, China-bull, debasement-pilled), let it execute across thousands of markets

Futarchy: bet on outcomes instead of voting on preferences; implement the policy with the highest market price

And here's the part nobody on CT has fully worked out yet.

AI doesn't just process volatility. It creates it. Markets where AI agents are 90 percent of liquidity will move faster, react harder, and reprice more frequently than human-dominated markets ever could. The volatility regime that drove perpification in the first place will intensify as AI takes over participation.

Perpification isn't the endpoint of a high-volatility world. It's the entry point to a much higher-volatility one. Which forces the question. When AI agents are the marginal liquidity provider on every market, and any opinion is leverable in real-time, what does retail participation even mean?

Are humans speculators? Or are humans the slow, biased, emotional counterparties for AI agents that out-process them by orders of magnitude in every dimension that matters? Polymarket's tagline arc, projected forward. "We price the future." Then "now you can lever it." Then "we price the future, and the agents trading it have already factored in your move."

Perpification of everything was always going to mean perpification by everything. Including agents that aren't human at all. The trade is no longer an asset. The trade is whether you're the player or the LP.

7. Conclusion

Volatility is the fuel. Perps are the engine. AI is about to be the driver.

The world is producing more uncertainty per quarter than at any point most of us have been alive for, and a generation that figured out the conventional path doesn't close their gap has decided to trade it instead of hide from it. That's not gambling. That's not nihilism. It's the cleanest available read of the environment we're actually in.

Crypto skipped options because perps are what people would have built if TradFi's regulatory plumbing hadn't held the wrong instrument in place for fifty years. And every assumption underneath that shift, that humans set the prices, that retail competes with retail, that liquidity is the bottleneck, breaks the moment AI agents become the marginal participant in every market.

The market is open. The agents are awake. Pick your seat.

Recommended Articles

Dive into 'Narratives' that will be important in the next year

" height="53.254000000000005px" id="poHfazHFu" transform="translate(192 19.5)" width="54.447px"/><path d="M 17.077 0 C 20.225 0 23.038 0.665 25.515 1.994 C 28.06 3.324 30.036 5.153 31.442 7.48 C 32.916 9.74 33.652 12.233 33.652 14.96 L 25.114 14.96 C 25.114 12.832 24.344 11.036 22.804 9.573 C 21.263 8.111 19.354 7.38 17.077 7.38 C 14.867 7.38 12.992 8.045 11.452 9.374 C 9.979 10.637 9.242 12.234 9.242 14.161 C 9.242 16.289 10.112 18.051 11.853 19.446 C 13.662 20.843 16.207 21.973 19.488 22.837 C 24.176 24.034 27.826 25.863 30.437 28.322 C 33.049 30.782 34.355 34.007 34.355 37.996 C 34.355 41.054 33.585 43.746 32.045 46.073 C 30.571 48.333 28.53 50.096 25.918 51.36 C 23.306 52.623 20.392 53.254 17.178 53.254 C 13.963 53.254 11.05 52.555 8.438 51.159 C 5.827 49.763 3.75 47.902 2.21 45.575 C 0.736 43.182 0 40.522 0 37.597 L 8.539 37.597 C 8.539 39.924 9.376 41.885 11.05 43.481 C 12.724 45.076 14.8 45.874 17.278 45.874 C 19.622 45.874 21.598 45.209 23.205 43.88 C 24.879 42.484 25.717 40.755 25.717 38.694 C 25.717 36.5 24.845 34.704 23.104 33.309 C 21.363 31.846 18.818 30.683 15.47 29.819 C 10.916 28.689 7.3 26.926 4.621 24.532 C 2.009 22.139 0.703 18.815 0.703 14.56 C 0.703 11.635 1.406 9.075 2.812 6.881 C 4.286 4.687 6.261 2.991 8.739 1.795 C 11.284 0.598 14.063 0 17.077 0 Z" fill="rgb(255, 255, 255)" height="53.25400000000002px" id="dwV_m7WwK" transform="translate(254.5 19.5)" width="34.35500000000002px"/><path d="M 27.223 0 C 32.313 0 36.934 1.163 41.086 3.49 C 45.238 5.817 48.486 9.009 50.83 13.064 C 53.241 17.12 54.447 21.641 54.447 26.627 C 54.447 27.957 54.347 29.12 54.146 30.117 L 8.81 30.117 C 9.154 32.32 9.878 34.446 10.95 36.401 C 12.557 39.259 14.767 41.52 17.579 43.181 C 20.459 44.844 23.674 45.675 27.223 45.675 C 31.107 45.675 34.557 44.778 37.571 42.982 C 40.651 41.187 42.895 38.794 44.301 35.802 L 53.342 35.802 C 51.467 41.054 48.185 45.276 43.497 48.467 C 38.809 51.658 33.384 53.254 27.223 53.254 C 22.133 53.254 17.513 52.091 13.361 49.764 C 9.209 47.437 5.927 44.245 3.516 40.189 C 1.172 36.134 0 31.613 0 26.627 C 0 21.641 1.172 17.12 3.516 13.064 C 5.927 9.009 9.209 5.817 13.361 3.49 C 17.513 1.164 22.133 0 27.223 0 Z M 27.223 7.58 C 23.674 7.58 20.459 8.41 17.579 10.072 C 14.767 11.734 12.557 14.028 10.95 16.953 C 9.958 18.722 9.265 20.643 8.898 22.638 L 45.545 22.638 C 45.137 20.485 44.341 18.424 43.196 16.555 C 41.588 13.762 39.378 11.568 36.566 9.973 C 33.753 8.377 30.638 7.579 27.223 7.579 Z M 103.691 44.578 L 110.522 44.578 L 110.522 52.058 L 96.257 52.058 L 96.257 45.427 C 94.611 47.805 92.401 49.683 89.627 51.06 C 86.748 52.522 83.533 53.254 79.984 53.254 C 76.501 53.254 73.353 52.522 70.54 51.06 C 67.795 49.53 65.585 47.503 63.91 44.977 C 62.303 42.45 61.499 39.592 61.499 36.401 C 61.499 33.209 62.303 30.35 63.91 27.823 C 65.518 25.231 67.728 23.203 70.54 21.74 C 73.353 20.278 76.501 19.546 79.984 19.546 L 95.453 19.546 L 95.453 9.076 L 64.915 9.076 L 64.915 1.196 L 103.691 1.196 Z M 80.888 26.926 C 78.879 26.926 77.037 27.359 75.363 28.223 C 73.688 29.021 72.382 30.151 71.445 31.613 C 70.507 33.009 70.038 34.605 70.038 36.401 C 70.038 38.129 70.507 39.724 71.445 41.187 C 72.382 42.649 73.688 43.814 75.363 44.677 C 77.037 45.476 78.879 45.874 80.888 45.874 C 83.768 45.874 86.279 45.443 88.422 44.578 C 90.632 43.648 92.34 42.417 93.545 40.888 C 94.818 39.292 95.453 37.463 95.453 35.402 L 95.453 26.926 Z" fill="rgb(255, 255, 255)" height="53.254000000000005px" id="J9sNA1zvT" transform="translate(296.5 19.5)" width="110.52200054931643px"/><path d="M 472.484 17.603 C 476.837 17.603 480.856 18.467 484.539 20.196 C 488.222 21.858 491.302 24.218 493.78 27.276 C 496.325 30.334 498.034 33.792 498.904 37.648 L 490.164 37.648 C 488.825 33.991 486.581 31.066 483.434 28.872 C 480.286 26.678 476.636 25.581 472.484 25.581 C 469.002 25.581 465.82 26.411 462.94 28.074 C 460.128 29.669 457.884 31.897 456.21 34.755 C 454.603 37.615 453.8 40.773 453.8 44.23 C 453.8 47.687 454.603 50.845 456.21 53.704 C 457.884 56.562 460.128 58.824 462.94 60.486 C 465.82 62.082 469.002 62.879 472.484 62.879 C 476.636 62.879 480.286 61.781 483.434 59.587 C 486.581 57.393 488.825 54.469 490.164 50.812 L 498.904 50.812 C 498.034 54.668 496.325 58.125 493.78 61.183 C 491.302 64.241 488.222 66.635 484.539 68.363 C 480.856 70.027 476.837 70.857 472.484 70.857 C 467.395 70.857 462.773 69.694 458.621 67.367 C 454.469 65.04 451.187 61.848 448.776 57.792 C 446.433 53.737 445.261 49.216 445.261 44.23 C 445.261 39.244 446.433 34.723 448.776 30.667 C 451.187 26.612 454.469 23.42 458.621 21.093 C 462.773 18.766 467.395 17.603 472.484 17.603 Z M 68.395 70.021 L 58.566 70.021 L 34.197 10.609 L 9.83 70.021 L 0 70.021 L 28.873 0 L 39.522 0 Z M 96.18 70.021 L 87.443 70.021 L 87.443 10.047 L 71.775 10.047 L 71.775 0 L 96.181 0 L 96.181 70.021 Z" fill="rgb(255, 255, 255)" height="70.85700064086915px" id="XyVzovWZk" transform="translate(0 2)" width="498.90398632812503px"/><path d="M 22.401 0 C 26.419 0 30.036 0.93 33.251 2.792 C 36.532 4.587 39.11 7.081 40.985 10.272 C 42.86 13.396 43.799 16.92 43.799 20.843 C 43.799 24.699 42.86 28.189 40.985 31.313 C 39.11 34.372 36.566 36.799 33.351 38.593 C 31.265 39.754 28.996 40.549 26.642 40.943 L 45.205 68.812 L 34.557 68.812 L 16.616 41.286 L 8.84 41.286 L 8.84 68.812 L 0 68.812 L 0 0 Z M 8.84 33.608 L 22.2 33.608 C 24.544 33.608 26.688 33.076 28.63 32.012 C 30.572 30.882 32.079 29.352 33.15 27.425 C 34.222 25.497 34.758 23.336 34.758 20.943 C 34.758 18.549 34.222 16.388 33.15 14.46 C 32.079 12.532 30.572 11.003 28.63 9.873 C 26.688 8.743 24.544 8.177 22.2 8.177 L 8.84 8.177 Z" fill="rgb(255, 255, 255)" height="68.812px" id="tX8m5fMcV" transform="translate(141 3)" width="45.20500000000001px"/><path d="M 25.215 28.622 C 21.732 28.622 18.685 29.352 16.073 30.815 C 13.528 32.278 11.586 34.34 10.247 36.999 C 8.908 39.592 8.237 42.65 8.237 46.174 L 8.237 71.804 L 0 71.804 L 0 20.942 L 8.237 20.942 L 8.237 30.4 C 10.035 27.253 12.277 24.798 14.969 23.037 C 17.982 21.109 21.397 20.145 25.215 20.145 Z M 102.415 29.563 C 104.366 26.491 106.844 24.116 109.848 22.439 C 113.13 20.643 116.88 19.746 121.099 19.746 C 125.185 19.746 128.801 20.61 131.948 22.339 C 135.163 24.001 137.64 26.428 139.382 29.619 C 141.123 32.744 141.994 36.367 141.994 40.489 L 141.994 71.804 L 133.757 71.804 L 133.757 42.982 C 133.757 38.395 132.351 34.705 129.538 31.912 C 126.792 29.12 123.108 27.724 118.487 27.724 C 115.273 27.724 112.427 28.356 109.949 29.619 C 107.538 30.882 105.663 32.71 104.323 35.103 C 103.051 37.431 102.415 40.123 102.415 43.182 L 102.415 71.804 L 94.178 71.804 L 94.178 0 L 102.415 0 Z" fill="rgb(255, 255, 255)" height="71.80400045776368px" id="YoO0zKl7f" transform="translate(416 0)" width="141.99400140380868px"/></g><g d="M 8.96 4.214 C 9.786 4.214 10.48 4.51 11.042 5.107 C 11.637 5.668 11.936 6.362 11.936 7.189 C 11.936 8.014 11.637 8.725 11.042 9.32 C 10.749 9.613 10.42 9.826 10.055 9.967 L 12.183 13.732 L 10.4 13.732 L 8.453 10.162 L 7.471 10.162 L 7.471 13.734 L 5.884 13.734 L 5.884 4.212 L 8.959 4.212 Z M 7.473 8.725 L 8.86 8.725 C 9.29 8.725 9.638 8.592 9.902 8.328 C 10.201 8.026 10.362 7.614 10.347 7.189 C 10.356 6.779 10.196 6.384 9.904 6.097 C 9.64 5.8 9.258 5.636 8.861 5.651 L 7.473 5.651 Z M 9.026 0 C 10.712 0 12.234 0.396 13.587 1.189 C 14.952 1.926 16.072 3.046 16.81 4.412 C 17.603 5.769 18 7.29 18 8.975 C 18 10.693 17.603 12.23 16.81 13.584 C 16.053 14.937 14.938 16.053 13.587 16.809 C 12.232 17.601 10.712 18 9.026 18 C 7.308 18 5.753 17.618 4.366 16.858 C 3.03 16.084 1.919 14.973 1.143 13.636 C 0.382 12.248 0.002 10.693 0 8.975 C 0 7.29 0.382 5.769 1.143 4.412 C 1.9 3.061 3.015 1.945 4.366 1.189 C 5.753 0.398 7.308 0 9.026 0 Z M 9.026 1.638 C 7.72 1.624 6.435 1.967 5.307 2.628 C 4.216 3.257 3.309 4.164 2.68 5.256 C 2.051 6.379 1.738 7.635 1.738 9.024 C 1.738 10.38 2.051 11.618 2.68 12.742 C 3.328 13.82 4.23 14.722 5.307 15.37 C 6.432 15.999 7.671 16.314 9.026 16.314 C 10.381 16.314 11.605 15.999 12.696 15.37 C 13.766 14.73 14.653 13.825 15.273 12.742 C 15.934 11.618 16.265 10.363 16.265 8.975 C 16.278 7.667 15.935 6.381 15.273 5.255 C 14.662 4.148 13.75 3.237 12.644 2.627 C 11.553 1.967 10.3 1.625 9.026 1.639 Z" fill="transparent" height="18px" id="fDqcVjis4" transform="translate(571 0)" width="18px"><path d="M 3.076 0.002 C 3.902 0.002 4.596 0.298 5.158 0.895 C 5.753 1.456 6.052 2.15 6.052 2.977 C 6.052 3.803 5.753 4.513 5.158 5.108 C 4.865 5.401 4.536 5.614 4.171 5.755 L 6.299 9.521 L 4.516 9.521 L 2.569 5.951 L 1.587 5.951 L 1.587 9.522 L 0 9.522 L 0 0 L 3.075 0 Z M 1.589 4.513 L 2.976 4.513 C 3.406 4.513 3.754 4.38 4.018 4.116 C 4.317 3.814 4.478 3.402 4.463 2.977 C 4.472 2.567 4.312 2.172 4.02 1.885 C 3.756 1.588 3.374 1.424 2.977 1.439 L 1.589 1.439 Z" fill="rgb(255, 255, 255)" height="9.522276301010859px" id="YcHNItJFD" transform="translate(5.884 4.212)" width="6.299243485570059px"/><path d="M 9.026 0 C 10.712 0 12.234 0.396 13.587 1.189 C 14.952 1.926 16.072 3.046 16.81 4.412 C 17.603 5.769 18 7.29 18 8.975 C 18 10.693 17.603 12.23 16.81 13.584 C 16.053 14.937 14.938 16.053 13.587 16.809 C 12.232 17.601 10.712 18 9.026 18 C 7.308 18 5.753 17.618 4.366 16.858 C 3.03 16.084 1.919 14.973 1.143 13.636 C 0.382 12.248 0.002 10.693 0 8.975 C 0 7.29 0.382 5.769 1.143 4.412 C 1.9 3.061 3.015 1.945 4.366 1.189 C 5.753 0.398 7.308 0 9.026 0 Z M 9.026 1.638 C 7.72 1.624 6.435 1.967 5.307 2.628 C 4.216 3.257 3.309 4.164 2.68 5.256 C 2.051 6.379 1.738 7.635 1.738 9.024 C 1.738 10.38 2.051 11.618 2.68 12.742 C 3.328 13.82 4.23 14.722 5.307 15.37 C 6.432 15.999 7.671 16.314 9.026 16.314 C 10.381 16.314 11.605 15.999 12.696 15.37 C 13.766 14.73 14.653 13.825 15.273 12.742 C 15.934 11.618 16.265 10.363 16.265 8.975 C 16.278 7.667 15.935 6.381 15.273 5.255 C 14.662 4.148 13.75 3.237 12.644 2.627 C 11.553 1.967 10.3 1.625 9.026 1.639 Z" fill="rgb(255, 255, 255)" height="18px" id="VlQ3a59vB" width="18px"/></g></svg>)