Executive Summary

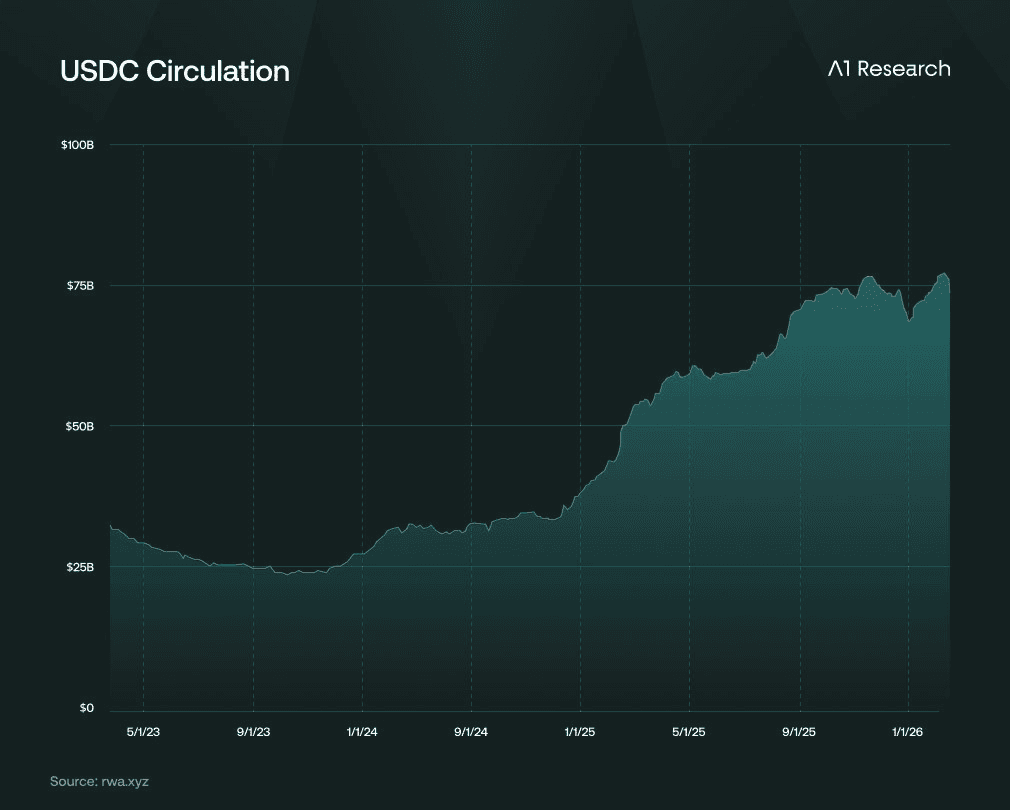

Agentic payments are solving a real gap: AI-driven, “unbankable” businesses (solo devs, micro-APIs) can finally transact via stablecoins, with USDC supply reaching ~$75B and L2 fees dropping to ~$0.001, making sub-dollar payments viable for the first time.

The infrastructure is already live and credible: Coinbase (x402), Stripe (MPP + x402), Visa, Google, AWS, and Cloudflare are shipping production integrations, embedding stablecoin micropayments directly into APIs and HTTP requests.

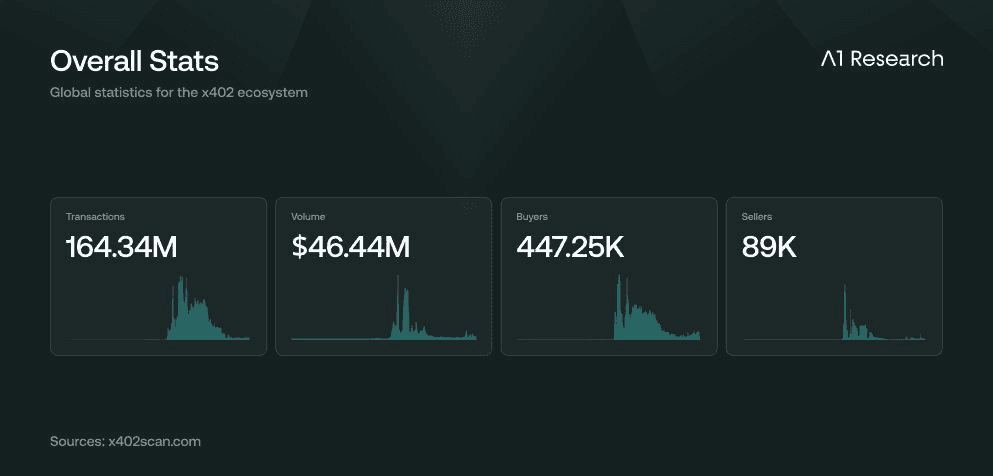

But the investability is overstated: despite ~165M transactions, real volume is only ~$30M over ~10 months, with most payments in the $0.20–$0.40 range and ~3,900 merchants tiny compared to Visa’s daily scale.

The payment layer itself is structurally weak: x402 has no token by design, facilitators can run at near-zero cost (~$5/month), and fees are racing toward zero, mirroring TCP/IP, which created massive value but captured none.

Value accrues elsewhere: settlement layers (Base, Solana), orchestration layers (Stripe processing $1.9T annually), and especially identity + trust infrastructure (70K+ onchain agents), where reputation systems create compounding network effects and durable moats.

The long term shift isn’t just payments but autonomous finance: as trillions in assets move onchain and ~$84T wealth transfers to a more crypto-native generation, agents may not just transact but manage capital making trust layers more valuable than payment rails.

Crypto reinvents its origin story every eighteen months or so. DeFi would replace banks. NFTs would replace ownership. The metaverse would replace, well, going outside. Each time, the pitch was directionally right and the timing was ruinous. Billions evaporated in the gap.

The latest version says that crypto was never really for people. It was built for machines. AI agents that don't fumble seed phrases, don't care that the UI looks like a spreadsheet had a panic attack, and don't need anyone to explain the difference between Base, Polygon, and Optimism.

And large companies are making predictions already:

- Coinbase CEO Brian Armstrong posted on X earlier this month that AI agents will soon outnumber humans making transactions.

- McKinsey says agents could touch $3 to $5 trillion in consumer commerce by 2030.

- Paradigm's Matt Huang tells builders to assume most of their customers won't be people at all.

The institutional coalition assembled around this idea is staggering. Coinbase, Cloudflare, Google, Stripe, Visa, AWS, Circle. All shipping production integrations, not proof of concepts, for protocols that embed stablecoin micropayments directly into HTTP requests.

So here's the problem if you're trying to invest in this: you can't tell whether the infrastructure being built will actually generate returns for anyone besides Coinbase and Stripe. The ecosystem reports cite $7 billion in market cap and 165 million transactions. The sceptics point to $50,000 in daily volume, half of it is wash trading. Same data. Opposite conclusions.

This piece asks a question neither side seems interested in asking: if agentic payments win, where does the money actually go?

The Placeholder That Finally Shipped

Here's a piece of internet history that matters.

In the 1990s, Tim Berners-Lee reserved HTTP status code 402, "Payment Required," right alongside 200 (OK) and 404 (Not Found). Think about that for a second. A native payment layer for the web, as basic as a hyperlink. Any server could charge for any resource at the protocol level.

It never shipped.

Credit card interchange fees made any payment under $5 a money loser, and without programmable settlement, micropayments couldn't exist. So the web defaulted to advertising. Google's auction model, Facebook's news feed, the entire clickbait industrial complex: all of it traces back to this one missing feature.

For thirty years, 402 sat dormant. A placeholder waiting for plumbing that didn't exist.

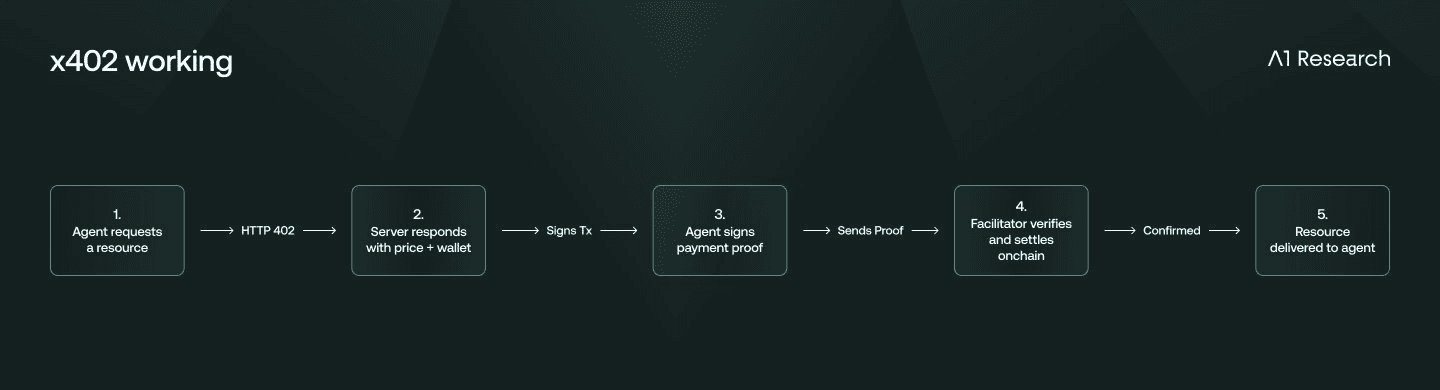

That plumbing exists now. Coinbase launched x402 in May 2025 to activate it, and the protocol does something refreshingly simple. An agent requests a resource. The server responds with a price, a token type, and a wallet address. The agent signs a payment proof. A facilitator verifies and settles onchain. The resource is delivered. No accounts, no API keys, no subscriptions. Settlement in roughly two seconds on Base for around $0.0001.

The companies that signed on moved fast:

Cloudflare co-founded the x402 Foundation.

Google built x402 into the Agent Payments Protocol (AP2).

Stripe launched x402-based USDC payments on Base through its PaymentIntents API.

AWS integrated it into Lambda and API Gateway.

Visa built x402 interoperability into its Trusted Agent Protocol after watching a 4,700% surge in AI-driven retail traffic.

Circle launched nanopayments: fractional-cent, fee-free USDC transfers.

Something like this has probably never happened before in crypto. Production integrations from companies that collectively serve billions of users.

So why now?

The strongest argument comes from Noah Levine at a16z, and it reframes everything. Everyone thinks AI payments are a tech problem. Wrong. It's a risk problem.

Traditional payment companies don't just move money. They absorb your risk. If you scam users, rack up chargebacks, or vanish overnight, the payment processor eats the loss. So before they let you accept payments, they ask one question: are you worth the risk?

AI is creating a new class of "business" that can't answer that question well. Solo builders, micro-APIs, single-purpose tools, sometimes not even a registered company. Small, fast, uncertain.

From a payment processor's view, this is a terrible trade: low revenue, high risk. So they simply don't onboard them.

And here's the key. These builders aren't choosing between cards and crypto. Cards won't have them. The real choice is stablecoins or nothing.

Crypto isn't competing with Visa here. It's filling a vacuum that Visa refuses to touch. AI keeps minting "unbankable" internet businesses, and stablecoins are becoming their default payment method.

Erik Reppel, x402's creator, frames it differently in a recent Forbes interview. Forget cheaper transactions. The bigger win is killing credential sprawl. Most companies maintain over 600 individual APIs, each with its own account, key, and billing relationship. With x402, your wallet becomes the universal API key. One credential, every service. If you've ever spent an afternoon wrestling OAuth tokens across a dozen platforms, you know exactly how appealing that sounds.

Two structural shifts made all of this viable at the same time.

1. Stablecoins hit critical mass: USDC circulation reached $75.3 billion by Q4 2025, up from around $500 million in 2019.

2. L2 fees collapsed. Base processes transactions for roughly $0.0001, Solana for about $0.005. The fee floor that killed micropayments in the 1990s just doesn't exist anymore.

Meanwhile, Stripe co-authored a competing standard called MPP (Machine Payments Protocol) with Tempo, a payments-focused L1 that raised $500 million at a $5 billion valuation with OpenAI, Visa, Shopify, and Anthropic as design partners. MPP takes a different path: session-based streaming payments where an agent authorises a spending limit upfront and streams micropayments against it, with Stripe's compliance, fraud detection, and tax handling baked in.

The two protocols aren't really fighting over the same users. x402 covers long-tail, permissionless scenarios: indie developer APIs, decentralised data markets, services that don't want a payment processor hovering over their shoulder. MPP covers enterprise-grade, high-frequency traffic where compliance and fiat settlement are non-negotiable. Stripe supports both and owns the abstraction layer above them, which is probably the smartest positioning in the entire space.

So the infrastructure is real, the backers are first-rate, and the gap it fills is genuine. If you stopped reading here, you'd think this was a once-in-a-decade investment opportunity.

Most people do stop here, that's the problem.

The Volume Is a Mirage And the Timeline Is a Trap

Approximately 165 million transactions and $46.5 million in cumulative volume. Looks like a market that's arrived.

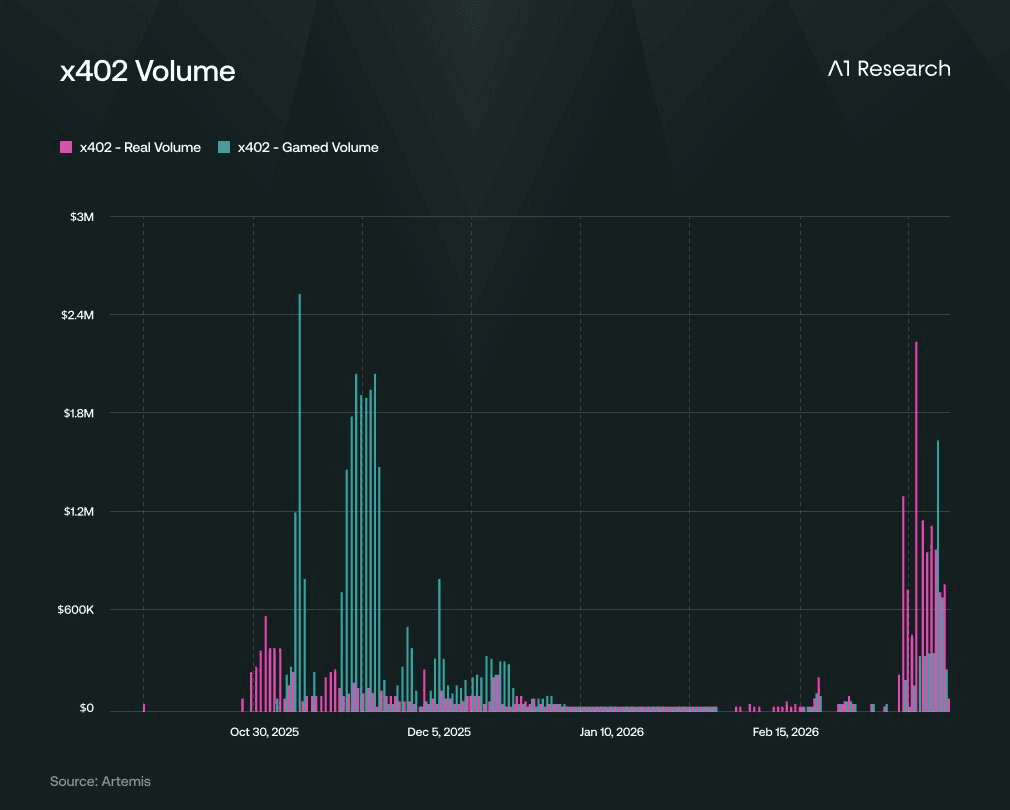

The Artemis data lays that in Q4 2025: mostly gamed volume, artificial transactions juicing the metrics. Then everything went dead through year-end and into January 2026. Then volume came back, and the composition flipped. Most current activity is real, not gamed. Galaxy Research confirms the share of gamed transactions dropped below 50% in early December 2025 and keeps falling.

That 68% decline in 30-day transactions is the system shedding noise and revealing actual demand underneath. Encouraging, genuinely.

But let's be honest about what "actual demand" means at this scale. Around 107 million transactions over ten months. About $30 million in legitimate volume. Most payments are between 20 and 40 cents. Roughly 3,900 merchants, including AWS, Alchemy, and Messari. Run the unit economics and the picture gets sobering. The average x402 merchant is pulling in about $769 per month across roughly 2,700 transactions.

To make even $5,000 a month selling API calls at $0.30 each, a merchant needs around 16,700 transactions, six times what the average merchant currently handles. To make $10,000 a month, you need over 33,000. The entire ecosystem generates about $3 million in monthly volume spread across nearly 4,000 sellers. For context, Felix - an AI agent running an app store for other agents on Base earned $163,686 in a single month. That's 213 times what the average x402 merchant makes. The outliers are dramatic. The median is not a business.

Real, yes. Tiny, also yes. x402's entire cumulative volume is five times less than what Visa processes in a single day.

The timeline problem

Haseeb Qureshi at Dragonfly offers the sharpest frame for thinking from the investment point of view. His analogy says that the computer mouse was invented in 1964. Imagine seeing it and looking into the future. No more terminal interfaces. GUIs would onboard billions. You'd be right. But it took decades before the mouse was widespread and commercial.

That's where agentic payments sit right now.

Qureshi identifies a specific catalyst worth tracking because it's falsifiable. None of the major AI labs have fine-tuned models against OpenClaw traces yet, and those traces are rich with signal. Once the first lab releases a purpose-built agentic model, expect a big jump in performance. Every lab has piles of OpenClaw data, and they're all working on this because the prize is enormous.

That catalyst is months away, not years. But even then, the adoption curve stretches long. Tinkerers are playing with this now. Early adopters follow after next-gen models ship. The early majority comes years later. The late majority, many years after that.

Qureshi puts it well: what smart people do on weekends and evenings today, everyone will be doing in ten years.

Here's the cold reality, though. Being directionally right about the technology while being wrong about the timeline is economically the same as being wrong.

Incumbents aren't waiting

Traditional payment companies are not standing on the sidelines while tinkerers experiment. They're building:

Santander and Mastercard completed Europe's first live end-to-end AI agent payment within a regulated banking framework in March 2026. Visa's Trusted Agent Protocol has processed hundreds of agent transactions with 100+ partners. Stripe's Agentic Commerce Suite already works across x402, MPP, and Google's UCP, with Etsy, URBN, Coach, Kate Spade, and Ashley Furniture onboarded. Stripe also added Affirm and Klarna to agent transactions through Shared Payment Tokens. Mastercard Agent Pay is live for all US cardholders and integrated into PayPal's wallet.

Olivia Chow at Zero Knowledge Consulting makes a great point that crypto-native sources consistently miss: what card networks are exceptionally good at is defining the rules for when things go wrong. Who's responsible, what happens to a regular person when a transaction breaks, how fraud gets resolved. Stablecoins still haven't figured out the equivalent. And because card networks are already building agentic capabilities, this might not threaten their business at all. It could increase their power, because now they're not just processing payments but sitting on the discovery side too.

Trace Cohen at Six Point Ventures is blunter. The notion that Visa and Mastercard won't matter in the age of AI agents is absurd. Their technology works. History says they're far more likely to buy or absorb promising newcomers than be displaced by them.

So the tech is real but the volumes are negligible. The timeline is years. Incumbents are adapting faster than anyone expected. The natural conclusion is that x402 is uninvestable.

That conclusion is also wrong. You just have to look at a different layer.

Where the Money Actually Goes

Here's the core issue. The entire agentic payments debate is stuck on the wrong question. Everyone argues about which payment rail wins: x402 vs MPP vs card networks. But the payment layer is commoditising toward zero.

Think about this for a second. A hackathon submission ran a fully functional x402 facilitator for $5 a month. Dexter's zero-fee facilitator model already commands around 35% of daily transaction share. The x402 protocol itself has no native token. Deliberately.

Protocol neutrality speeds up adoption by removing rent-seeking friction. Great for the system. Terrible for anyone trying to invest in the protocol layer Khala Research draws the comparison to TCP/IP, and the parallel cuts both ways. TCP/IP built the internet. It captured nothing. The infrastructure on top, Amazon, Google, Stripe, captured everything. x402 may be the payment equivalent: an open protocol that creates massive value for the economy it powers while generating zero value for its own "shareholders" (because it doesn't have any).

So the investable question isn't whether x402 wins. It's which layers of the stack built around x402 have durable economics.

The value hierarchy

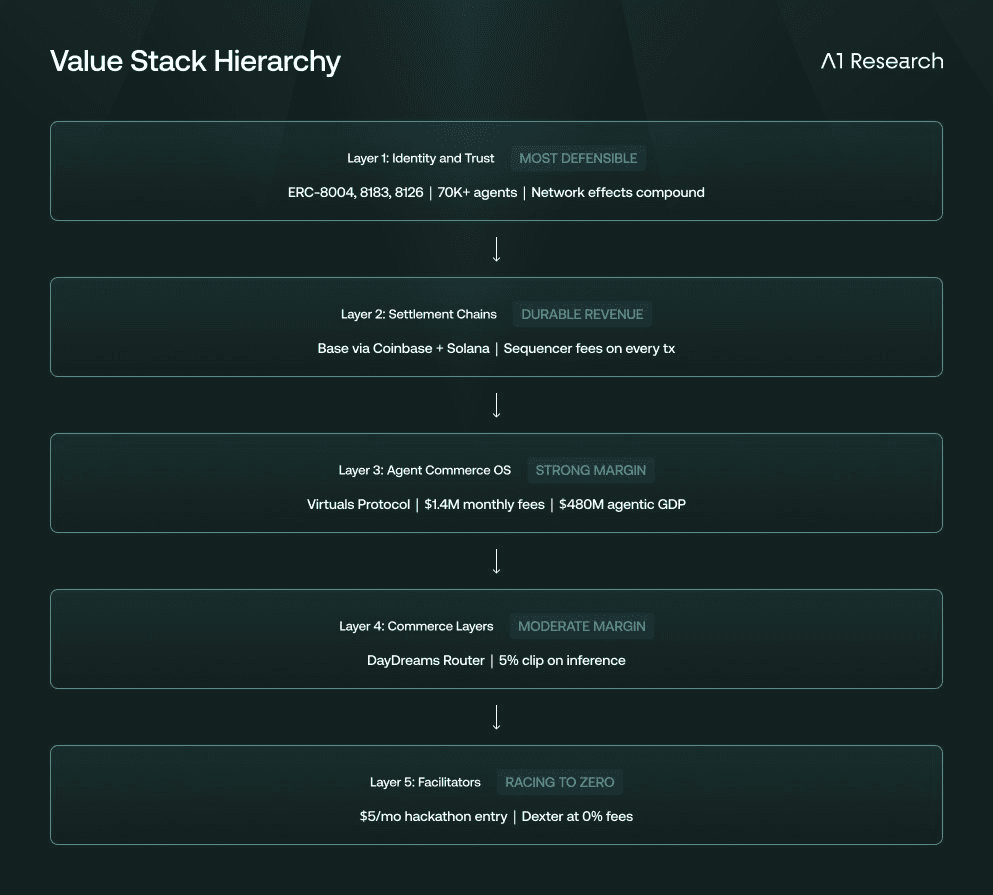

Here's what emerges when you cross-reference every source.

Settlement chains earn sequencer fees on every transaction. Base (via Coinbase) and Solana are the primary beneficiaries. This is the most durable revenue stream because the protocol itself enforces it.

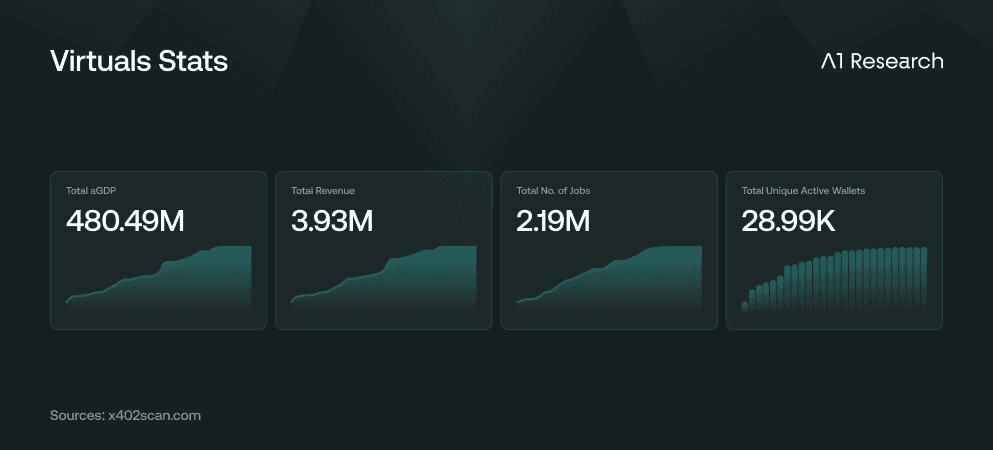

Agent commerce operating systems capture transaction fees on agent-to-agent work. Virtuals Protocol is generating $3.9 million in monthly revenue fees with $480 million in cumulative "Agentic GDP."

Commerce layers capture routing and inference fees. DayDreams takes a 5% clip on inference transactions through its Router.

Identity and trust layers earn attestation and verification fees. We will come back to this because it's the layer everyone is sleeping on.

Facilitators, the layer most visibly connected to x402, are the most contested and lowest-margin part of the stack. Commoditising fastest.

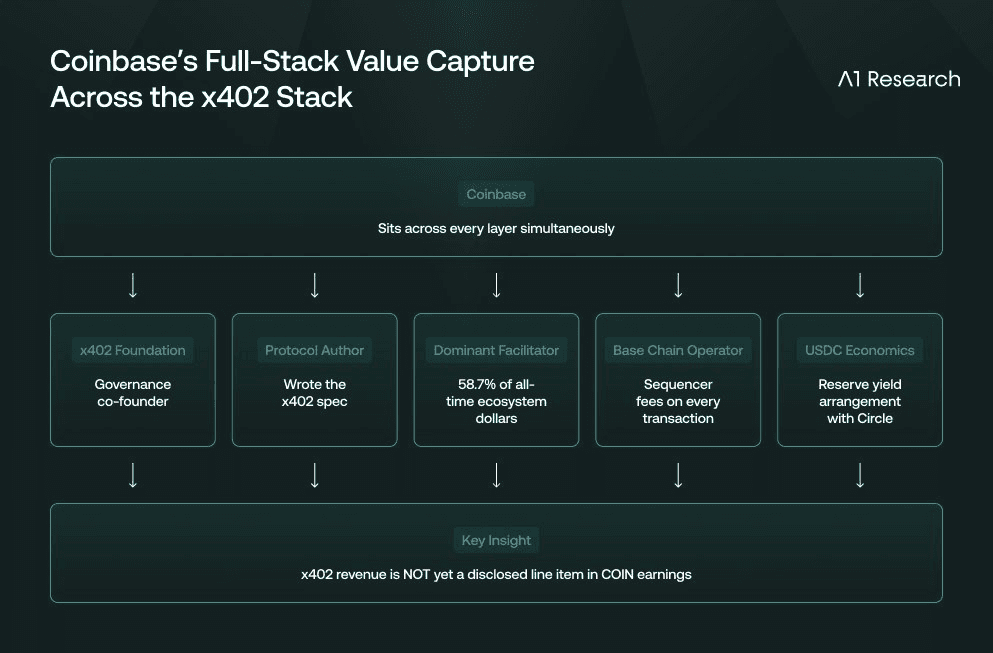

The Coinbase inevitability

The entity best positioned is the one that wrote the protocol.

Coinbase sits at every layer simultaneously: protocol author, dominant facilitator by cumulative dollar volume (58.7% of all-time ecosystem dollars), Base settlement chain operator, USDC economics participant through its reserve yield arrangement with Circle, and x402 Foundation co-founder.

Even if facilitators commoditise completely (which they are), Coinbase still earns Base sequencer fees and USDC float on every transaction that settles. Brian Armstrong declared an "AI-first mentality" throughout the company and predicted that AI agents will soon outnumber humans in transaction volume.

x402 machine commerce revenue isn't a disclosed line item in Coinbase earnings yet. No analyst consensus model prices it in. If you want x402 exposure, the cleanest instrument may simply be COIN equity. Not ecosystem tokens. NFA

Stripe's quiet move

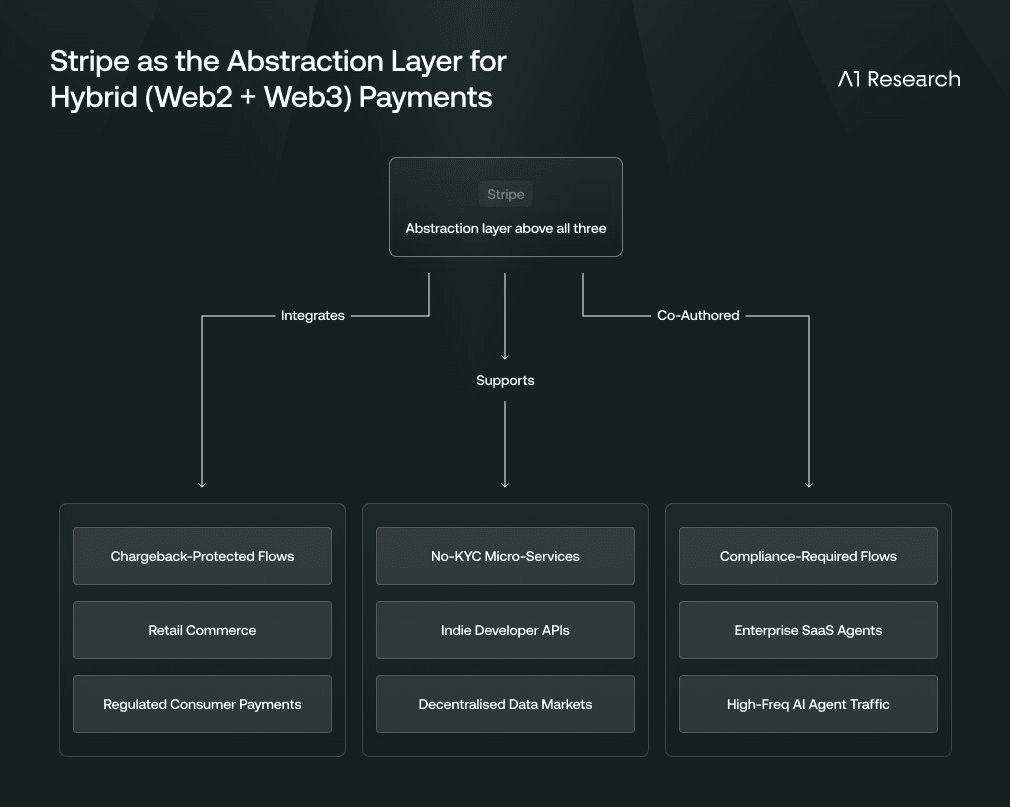

Stripe's positioning is equally sharp and even less discussed.

By supporting x402 on Base, co-authoring MPP with Tempo, and building a protocol-agnostic Agentic Commerce Suite all at the same time, Stripe guarantees it captures value regardless of which protocol wins. Funds flow through Stripe's account system no matter what. The company processed $1.9 trillion in 2025 payment volume. It doesn't need to bet on a protocol. It just needs to be the layer above all of them.

The layer everyone is sleeping on

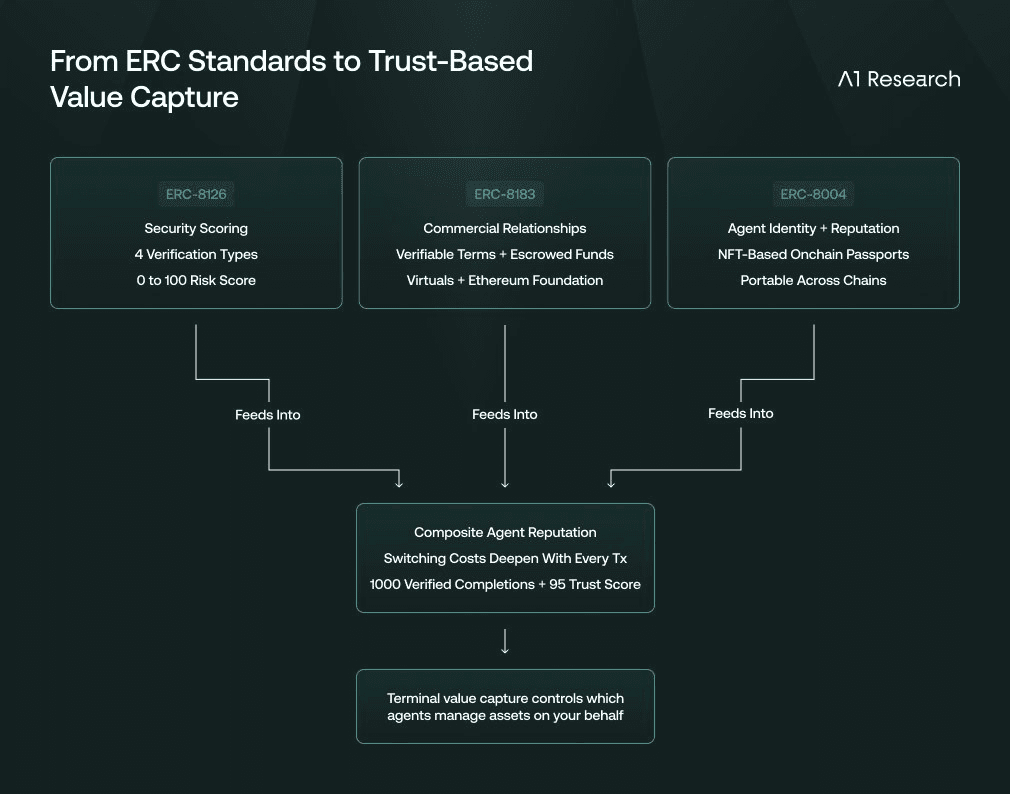

The most underappreciated part of this entire stack, the one with the strongest structural moat and the least analyst attention, is agent identity and trust.

Here's what's being built. ERC-8004 handles agent identity and reputation through onchain NFT-based passports. ERC-8183, co-developed by Virtuals Protocol and the Ethereum Foundation, adds the commercial relationship: verifiable terms, escrowed funds, delivery attestation, deterministic settlement. ERC-8126 adds security scoring, four verification types feeding into a 0-to-100 risk score. Over 70,000 agents are already registered onchain across Ethereum, Base, and BNB.

Here's why this matters more than payments.

Stripe can process a card payment. It cannot provide a cryptographically verifiable, portable, onchain reputation record for a non-human agent. OAuth 2.0 handles delegated authorisation. It was not designed for agents operating without persistent human sessions across thousands of endpoints simultaneously.

The payment piece is commoditising. The identity piece has natural network effects. Every completed job feeds a reputation signal back into the agent's onchain record, creating switching costs that deepen with every transaction. An agent with a thousand verified completions and a 95 trust score on ERC-8004 has something you can't replicate by starting over on a different system.

This is the one layer where crypto-native infrastructure has a durable structural advantage that incumbents genuinely can't copy.

The Bigger Game

Extend the timeline and the endgame may not be payments at all.

Forbes recently surfaced a dimension the crypto-native sources almost entirely miss. As traditional assets migrate onto blockchains (BlackRock's $2 billion Treasury fund BUIDL, Franklin Templeton's $1 billion government money fund FOBXX), the building blocks for autonomous portfolio management are quietly falling into place.

A stock index is just a rules-based basket. Once assets exist in tokenised form, AI agents don't just spend money. They hold assets, rebalance portfolios, move capital across markets without ever touching a traditional brokerage account.

This arrives alongside two huge demographic shifts. About $84 trillion is expected to pass from Baby Boomers to their heirs, many of whom grew up with Robinhood, already have crypto wallets, and are comfortable with automated financial management. And roughly 40% of the approximately 330,000 US financial advisors are expected to retire in the next decade, creating a structural gap in wealth management that somebody will fill.

If the endgame is agents managing money and not just spending it, then payment rails are the wedge, not the destination. The firms that control agent identity, reputation, and trust infrastructure, the layers that decide which agents are authorised to manage assets on your behalf, may capture more terminal value than anyone processing the underlying transactions.

Final Note

The agentic payments infrastructure being built right now is genuinely new. The institutional coalition is real. The technical gap it fills is real. The long-tail merchant class it serves can't be served by traditional rails. None of that is hype.

But "real infrastructure" is not "investable at current prices."

The protocol layer captures nothing by design. The facilitator layer races to zero. The timeline from tinkerers to mainstream stretches years. Incumbents are moving faster than expected, carrying a trust and compliance moat stablecoins haven't cracked yet. The $7 billion CoinGecko number is mostly Chainlink. The $700 million in genuinely connected tokens prices in a future that depends on model capabilities nobody has built yet.

The contrarian move isn't to dismiss x402. It's to look past the payment story entirely and ask where compounding network effects actually live.

Right now, that's the identity layer. Onchain reputation and trust infrastructure that incumbents can't replicate and that deepens with every transaction.

In five years, it might be the entire autonomous financial management stack.

The mouse was invented in 1964. The GUI revolution it powered was real. But the people who made money weren't the ones who invested in the mouse.

Disclaimer: The content provided in this article is for educational and informational purposes only and should not be construed as financial, investment, or trading advice. Digital assets are highly volatile and involve substantial risk. Past performance is not indicative of future results. Always conduct your own research and consult with qualified financial advisors before making any investment decisions. A1 Research is not responsible for any losses incurred based on the information provided in this article. This campaign contains sponsored content. A1 Research and its affiliates may hold positions in the projects and protocols mentioned in this article.

Recommended Articles

Dive into 'Narratives' that will be important in the next year

" height="53.254000000000005px" id="poHfazHFu" transform="translate(192 19.5)" width="54.447px"/><path d="M 17.077 0 C 20.225 0 23.038 0.665 25.515 1.994 C 28.06 3.324 30.036 5.153 31.442 7.48 C 32.916 9.74 33.652 12.233 33.652 14.96 L 25.114 14.96 C 25.114 12.832 24.344 11.036 22.804 9.573 C 21.263 8.111 19.354 7.38 17.077 7.38 C 14.867 7.38 12.992 8.045 11.452 9.374 C 9.979 10.637 9.242 12.234 9.242 14.161 C 9.242 16.289 10.112 18.051 11.853 19.446 C 13.662 20.843 16.207 21.973 19.488 22.837 C 24.176 24.034 27.826 25.863 30.437 28.322 C 33.049 30.782 34.355 34.007 34.355 37.996 C 34.355 41.054 33.585 43.746 32.045 46.073 C 30.571 48.333 28.53 50.096 25.918 51.36 C 23.306 52.623 20.392 53.254 17.178 53.254 C 13.963 53.254 11.05 52.555 8.438 51.159 C 5.827 49.763 3.75 47.902 2.21 45.575 C 0.736 43.182 0 40.522 0 37.597 L 8.539 37.597 C 8.539 39.924 9.376 41.885 11.05 43.481 C 12.724 45.076 14.8 45.874 17.278 45.874 C 19.622 45.874 21.598 45.209 23.205 43.88 C 24.879 42.484 25.717 40.755 25.717 38.694 C 25.717 36.5 24.845 34.704 23.104 33.309 C 21.363 31.846 18.818 30.683 15.47 29.819 C 10.916 28.689 7.3 26.926 4.621 24.532 C 2.009 22.139 0.703 18.815 0.703 14.56 C 0.703 11.635 1.406 9.075 2.812 6.881 C 4.286 4.687 6.261 2.991 8.739 1.795 C 11.284 0.598 14.063 0 17.077 0 Z" fill="rgb(255, 255, 255)" height="53.25400000000002px" id="dwV_m7WwK" transform="translate(254.5 19.5)" width="34.35500000000002px"/><path d="M 27.223 0 C 32.313 0 36.934 1.163 41.086 3.49 C 45.238 5.817 48.486 9.009 50.83 13.064 C 53.241 17.12 54.447 21.641 54.447 26.627 C 54.447 27.957 54.347 29.12 54.146 30.117 L 8.81 30.117 C 9.154 32.32 9.878 34.446 10.95 36.401 C 12.557 39.259 14.767 41.52 17.579 43.181 C 20.459 44.844 23.674 45.675 27.223 45.675 C 31.107 45.675 34.557 44.778 37.571 42.982 C 40.651 41.187 42.895 38.794 44.301 35.802 L 53.342 35.802 C 51.467 41.054 48.185 45.276 43.497 48.467 C 38.809 51.658 33.384 53.254 27.223 53.254 C 22.133 53.254 17.513 52.091 13.361 49.764 C 9.209 47.437 5.927 44.245 3.516 40.189 C 1.172 36.134 0 31.613 0 26.627 C 0 21.641 1.172 17.12 3.516 13.064 C 5.927 9.009 9.209 5.817 13.361 3.49 C 17.513 1.164 22.133 0 27.223 0 Z M 27.223 7.58 C 23.674 7.58 20.459 8.41 17.579 10.072 C 14.767 11.734 12.557 14.028 10.95 16.953 C 9.958 18.722 9.265 20.643 8.898 22.638 L 45.545 22.638 C 45.137 20.485 44.341 18.424 43.196 16.555 C 41.588 13.762 39.378 11.568 36.566 9.973 C 33.753 8.377 30.638 7.579 27.223 7.579 Z M 103.691 44.578 L 110.522 44.578 L 110.522 52.058 L 96.257 52.058 L 96.257 45.427 C 94.611 47.805 92.401 49.683 89.627 51.06 C 86.748 52.522 83.533 53.254 79.984 53.254 C 76.501 53.254 73.353 52.522 70.54 51.06 C 67.795 49.53 65.585 47.503 63.91 44.977 C 62.303 42.45 61.499 39.592 61.499 36.401 C 61.499 33.209 62.303 30.35 63.91 27.823 C 65.518 25.231 67.728 23.203 70.54 21.74 C 73.353 20.278 76.501 19.546 79.984 19.546 L 95.453 19.546 L 95.453 9.076 L 64.915 9.076 L 64.915 1.196 L 103.691 1.196 Z M 80.888 26.926 C 78.879 26.926 77.037 27.359 75.363 28.223 C 73.688 29.021 72.382 30.151 71.445 31.613 C 70.507 33.009 70.038 34.605 70.038 36.401 C 70.038 38.129 70.507 39.724 71.445 41.187 C 72.382 42.649 73.688 43.814 75.363 44.677 C 77.037 45.476 78.879 45.874 80.888 45.874 C 83.768 45.874 86.279 45.443 88.422 44.578 C 90.632 43.648 92.34 42.417 93.545 40.888 C 94.818 39.292 95.453 37.463 95.453 35.402 L 95.453 26.926 Z" fill="rgb(255, 255, 255)" height="53.254000000000005px" id="J9sNA1zvT" transform="translate(296.5 19.5)" width="110.52200054931643px"/><path d="M 472.484 17.603 C 476.837 17.603 480.856 18.467 484.539 20.196 C 488.222 21.858 491.302 24.218 493.78 27.276 C 496.325 30.334 498.034 33.792 498.904 37.648 L 490.164 37.648 C 488.825 33.991 486.581 31.066 483.434 28.872 C 480.286 26.678 476.636 25.581 472.484 25.581 C 469.002 25.581 465.82 26.411 462.94 28.074 C 460.128 29.669 457.884 31.897 456.21 34.755 C 454.603 37.615 453.8 40.773 453.8 44.23 C 453.8 47.687 454.603 50.845 456.21 53.704 C 457.884 56.562 460.128 58.824 462.94 60.486 C 465.82 62.082 469.002 62.879 472.484 62.879 C 476.636 62.879 480.286 61.781 483.434 59.587 C 486.581 57.393 488.825 54.469 490.164 50.812 L 498.904 50.812 C 498.034 54.668 496.325 58.125 493.78 61.183 C 491.302 64.241 488.222 66.635 484.539 68.363 C 480.856 70.027 476.837 70.857 472.484 70.857 C 467.395 70.857 462.773 69.694 458.621 67.367 C 454.469 65.04 451.187 61.848 448.776 57.792 C 446.433 53.737 445.261 49.216 445.261 44.23 C 445.261 39.244 446.433 34.723 448.776 30.667 C 451.187 26.612 454.469 23.42 458.621 21.093 C 462.773 18.766 467.395 17.603 472.484 17.603 Z M 68.395 70.021 L 58.566 70.021 L 34.197 10.609 L 9.83 70.021 L 0 70.021 L 28.873 0 L 39.522 0 Z M 96.18 70.021 L 87.443 70.021 L 87.443 10.047 L 71.775 10.047 L 71.775 0 L 96.181 0 L 96.181 70.021 Z" fill="rgb(255, 255, 255)" height="70.85700064086915px" id="XyVzovWZk" transform="translate(0 2)" width="498.90398632812503px"/><path d="M 22.401 0 C 26.419 0 30.036 0.93 33.251 2.792 C 36.532 4.587 39.11 7.081 40.985 10.272 C 42.86 13.396 43.799 16.92 43.799 20.843 C 43.799 24.699 42.86 28.189 40.985 31.313 C 39.11 34.372 36.566 36.799 33.351 38.593 C 31.265 39.754 28.996 40.549 26.642 40.943 L 45.205 68.812 L 34.557 68.812 L 16.616 41.286 L 8.84 41.286 L 8.84 68.812 L 0 68.812 L 0 0 Z M 8.84 33.608 L 22.2 33.608 C 24.544 33.608 26.688 33.076 28.63 32.012 C 30.572 30.882 32.079 29.352 33.15 27.425 C 34.222 25.497 34.758 23.336 34.758 20.943 C 34.758 18.549 34.222 16.388 33.15 14.46 C 32.079 12.532 30.572 11.003 28.63 9.873 C 26.688 8.743 24.544 8.177 22.2 8.177 L 8.84 8.177 Z" fill="rgb(255, 255, 255)" height="68.812px" id="tX8m5fMcV" transform="translate(141 3)" width="45.20500000000001px"/><path d="M 25.215 28.622 C 21.732 28.622 18.685 29.352 16.073 30.815 C 13.528 32.278 11.586 34.34 10.247 36.999 C 8.908 39.592 8.237 42.65 8.237 46.174 L 8.237 71.804 L 0 71.804 L 0 20.942 L 8.237 20.942 L 8.237 30.4 C 10.035 27.253 12.277 24.798 14.969 23.037 C 17.982 21.109 21.397 20.145 25.215 20.145 Z M 102.415 29.563 C 104.366 26.491 106.844 24.116 109.848 22.439 C 113.13 20.643 116.88 19.746 121.099 19.746 C 125.185 19.746 128.801 20.61 131.948 22.339 C 135.163 24.001 137.64 26.428 139.382 29.619 C 141.123 32.744 141.994 36.367 141.994 40.489 L 141.994 71.804 L 133.757 71.804 L 133.757 42.982 C 133.757 38.395 132.351 34.705 129.538 31.912 C 126.792 29.12 123.108 27.724 118.487 27.724 C 115.273 27.724 112.427 28.356 109.949 29.619 C 107.538 30.882 105.663 32.71 104.323 35.103 C 103.051 37.431 102.415 40.123 102.415 43.182 L 102.415 71.804 L 94.178 71.804 L 94.178 0 L 102.415 0 Z" fill="rgb(255, 255, 255)" height="71.80400045776368px" id="YoO0zKl7f" transform="translate(416 0)" width="141.99400140380868px"/></g><g d="M 8.96 4.214 C 9.786 4.214 10.48 4.51 11.042 5.107 C 11.637 5.668 11.936 6.362 11.936 7.189 C 11.936 8.014 11.637 8.725 11.042 9.32 C 10.749 9.613 10.42 9.826 10.055 9.967 L 12.183 13.732 L 10.4 13.732 L 8.453 10.162 L 7.471 10.162 L 7.471 13.734 L 5.884 13.734 L 5.884 4.212 L 8.959 4.212 Z M 7.473 8.725 L 8.86 8.725 C 9.29 8.725 9.638 8.592 9.902 8.328 C 10.201 8.026 10.362 7.614 10.347 7.189 C 10.356 6.779 10.196 6.384 9.904 6.097 C 9.64 5.8 9.258 5.636 8.861 5.651 L 7.473 5.651 Z M 9.026 0 C 10.712 0 12.234 0.396 13.587 1.189 C 14.952 1.926 16.072 3.046 16.81 4.412 C 17.603 5.769 18 7.29 18 8.975 C 18 10.693 17.603 12.23 16.81 13.584 C 16.053 14.937 14.938 16.053 13.587 16.809 C 12.232 17.601 10.712 18 9.026 18 C 7.308 18 5.753 17.618 4.366 16.858 C 3.03 16.084 1.919 14.973 1.143 13.636 C 0.382 12.248 0.002 10.693 0 8.975 C 0 7.29 0.382 5.769 1.143 4.412 C 1.9 3.061 3.015 1.945 4.366 1.189 C 5.753 0.398 7.308 0 9.026 0 Z M 9.026 1.638 C 7.72 1.624 6.435 1.967 5.307 2.628 C 4.216 3.257 3.309 4.164 2.68 5.256 C 2.051 6.379 1.738 7.635 1.738 9.024 C 1.738 10.38 2.051 11.618 2.68 12.742 C 3.328 13.82 4.23 14.722 5.307 15.37 C 6.432 15.999 7.671 16.314 9.026 16.314 C 10.381 16.314 11.605 15.999 12.696 15.37 C 13.766 14.73 14.653 13.825 15.273 12.742 C 15.934 11.618 16.265 10.363 16.265 8.975 C 16.278 7.667 15.935 6.381 15.273 5.255 C 14.662 4.148 13.75 3.237 12.644 2.627 C 11.553 1.967 10.3 1.625 9.026 1.639 Z" fill="transparent" height="18px" id="fDqcVjis4" transform="translate(571 0)" width="18px"><path d="M 3.076 0.002 C 3.902 0.002 4.596 0.298 5.158 0.895 C 5.753 1.456 6.052 2.15 6.052 2.977 C 6.052 3.803 5.753 4.513 5.158 5.108 C 4.865 5.401 4.536 5.614 4.171 5.755 L 6.299 9.521 L 4.516 9.521 L 2.569 5.951 L 1.587 5.951 L 1.587 9.522 L 0 9.522 L 0 0 L 3.075 0 Z M 1.589 4.513 L 2.976 4.513 C 3.406 4.513 3.754 4.38 4.018 4.116 C 4.317 3.814 4.478 3.402 4.463 2.977 C 4.472 2.567 4.312 2.172 4.02 1.885 C 3.756 1.588 3.374 1.424 2.977 1.439 L 1.589 1.439 Z" fill="rgb(255, 255, 255)" height="9.522276301010859px" id="YcHNItJFD" transform="translate(5.884 4.212)" width="6.299243485570059px"/><path d="M 9.026 0 C 10.712 0 12.234 0.396 13.587 1.189 C 14.952 1.926 16.072 3.046 16.81 4.412 C 17.603 5.769 18 7.29 18 8.975 C 18 10.693 17.603 12.23 16.81 13.584 C 16.053 14.937 14.938 16.053 13.587 16.809 C 12.232 17.601 10.712 18 9.026 18 C 7.308 18 5.753 17.618 4.366 16.858 C 3.03 16.084 1.919 14.973 1.143 13.636 C 0.382 12.248 0.002 10.693 0 8.975 C 0 7.29 0.382 5.769 1.143 4.412 C 1.9 3.061 3.015 1.945 4.366 1.189 C 5.753 0.398 7.308 0 9.026 0 Z M 9.026 1.638 C 7.72 1.624 6.435 1.967 5.307 2.628 C 4.216 3.257 3.309 4.164 2.68 5.256 C 2.051 6.379 1.738 7.635 1.738 9.024 C 1.738 10.38 2.051 11.618 2.68 12.742 C 3.328 13.82 4.23 14.722 5.307 15.37 C 6.432 15.999 7.671 16.314 9.026 16.314 C 10.381 16.314 11.605 15.999 12.696 15.37 C 13.766 14.73 14.653 13.825 15.273 12.742 C 15.934 11.618 16.265 10.363 16.265 8.975 C 16.278 7.667 15.935 6.381 15.273 5.255 C 14.662 4.148 13.75 3.237 12.644 2.627 C 11.553 1.967 10.3 1.625 9.026 1.639 Z" fill="rgb(255, 255, 255)" height="18px" id="VlQ3a59vB" width="18px"/></g></svg>)