Introduction

In February 2026, a single post by Vitalik Buterin set the Ethereum ecosystem on fire. The rollup-centric roadmap the architectural vision that had defined Ethereum's scaling strategy for half a decade needed to change. L2s had failed to decentralise. L1 was scaling on its own. The original deal no longer made sense.

What followed was weeks of loud, emotional debate. Founders were defending their chains. Researchers were dissecting the failure. Investors were questioning their bets.

Most of it missed the point.

This article is not about who was right in that debate. It is about what the data actually shows and why the path forward is considerably clearer than three years of ideological argument would suggest. We examine how L2s bootstrapped Ethereum through its most critical era, why generic L2s captured value that was supposed to flow back to Ethereum, which L2s built something genuinely differentiated and why they survive, and what the L1-L2 relationship structurally looks like from 2026 onward.

1. Ethereum Needed L2s to Survive And L2s Needed Ethereum to Exist

In 2021 and 2022, Ethereum was technically the most secure, decentralised smart contract platform in the world. It was also, for most practical purposes, not very usable. Average gas fees regularly hit $50 to $200 per transaction during periods of peak demand. NFT mints, DeFi interactions, basic token transfers, all of them priced out ordinary users and made the network inaccessible to anyone who wasn't moving large enough sums to justify the cost. Ethereum had won the credibility race. It was losing usability.

L2s arrived as emergency infrastructure at precisely the right moment. The economic logic behind why they succeeded is worth stating plainly. As per Decentralised Co article Large proof-of-stake L1s spend billions of dollars annually simply to keep validators producing blocks Ethereum itself spends roughly $4.5 billion per year on validator security with approximately $125 billion staked at around 3.7% APR, while Solana spends around $3.9 billion per year.

An independent chain attempting to rival Ethereum's security model faces that cost from day one, before acquiring a single user or developer. Running an L2 sequencer, by contrast, is cheap. L2s inherited Ethereum's security and credibility, the hardest and most expensive things to build in this industry without bearing their cost. Ethereum, in return, got the scale and usability it could not build fast enough on its own. The deal was asymmetric by design, and correctly so. The scale of what that arrangement produced is significant.

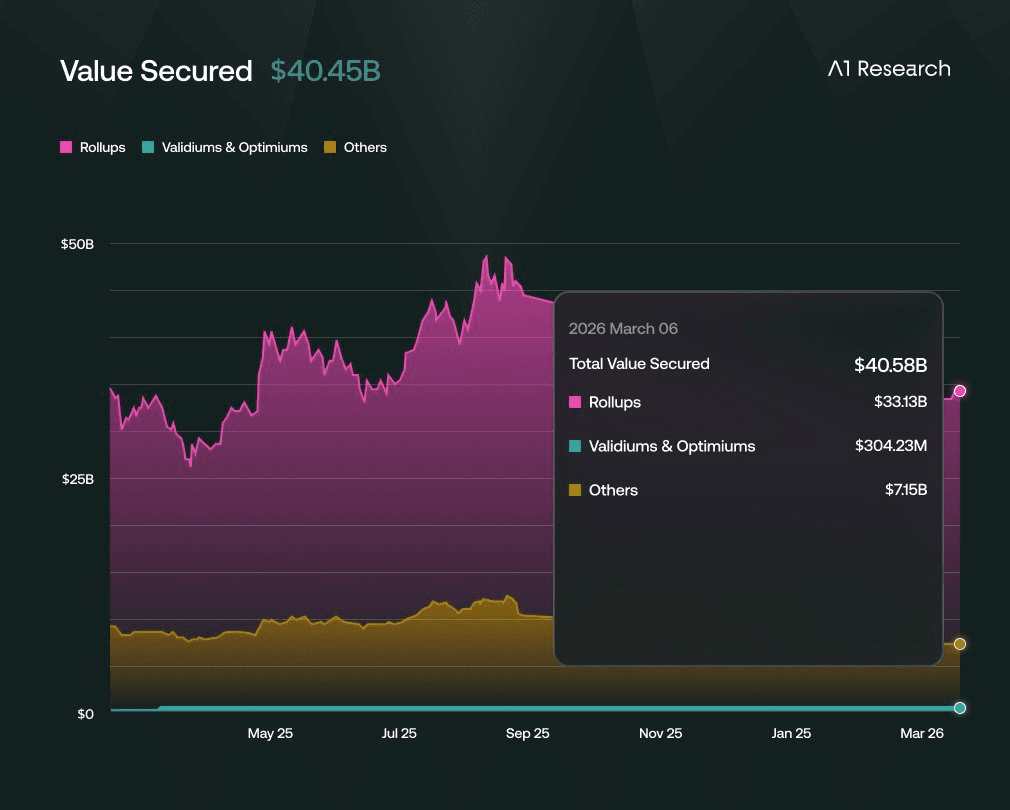

According to L2Beat and data compiled through 2025, L2 total value locked grew from under $4 billion in 2023 to roughly $47 billion by October 2025 more than a tenfold increase in under three years. Daily transactions on L2s climbed to as high as 1.9 million per day, eclipsing Ethereum mainnet transaction volume entirely. In Q1 2025 alone, L2 rollups secured over $40 billion in assets and processed nearly half of Ethereum's total DEX volume.

Meanwhile, Ethereum's own monthly transaction count climbed to 50 million-plus even as average fees fell well below prior cycles because heavy activity had migrated to L2s, freeing L1 to function as the high-integrity settlement layer it was designed to be. As Blockworks noted in their September 2025 analysis, the value of Ethereum's base layer increasingly derives from demand for its credible neutrality, security, and settlement across L2s not from maximising L1 fees directly.

Steven Goldfeder, CEO of Offchain Labs, provides the most concrete snapshot of what this produced at scale. During peak market volatility in early 2026, Arbitrum and Base both exceeded 1,000 TPS while Ethereum L1 sat at 40 TPS. His framing is precise: this is not a criticism of Ethereum. Arbitrum and Base would not exist without Ethereum's security foundation. That is the rollup-centric roadmap working exactly as designed, Ethereum providing settlement integrity while L2s absorb transaction volume at a scale L1 was never architected to handle directly.

Although, it is true that bootstrapping the Ethereum network to be used at scale was done by rollups. The numbers confirm it. Ethereum survived its scaling only because L2s absorbed the demand while L1 continued to develop. Currently, Ethereum holds just over $55 billion in DeFi TVL, far outpacing Solana at $6.76 billion and BNB Chain at $5.96 billion with $166 billion in Ethereum-based stablecoins, a reserve pool larger than the foreign exchange holdings of countries like Singapore and India.

A meaningful portion of that dominance was built on the back of an ecosystem made usable by L2s during the years when L1 alone could not carry it. At the time of writing, the approximate value secured by L2s and others is around $40 Billion.

The deal worked. Ethereum survived its most vulnerable era. L2s grew into commercially significant businesses with real users and real institutional partnerships. And that commercial success is precisely where the next problem began

Because what happens when an emergency contractor becomes a permanent tenant and starts optimising for their own revenue rather than the house they were called in to fix?

2. Generic L2s Solved the Capacity Crisis While Deepening the Identity Crisis

What played out between 2023 and 2025 was not a moral failure. It was incentive physics. But to understand why it damaged Ethereum specifically, we first need to understand exactly how value flows in a rollup-centric ecosystem and where it was supposed to go.

How Ethereum Was Supposed to Capture Value From L2s

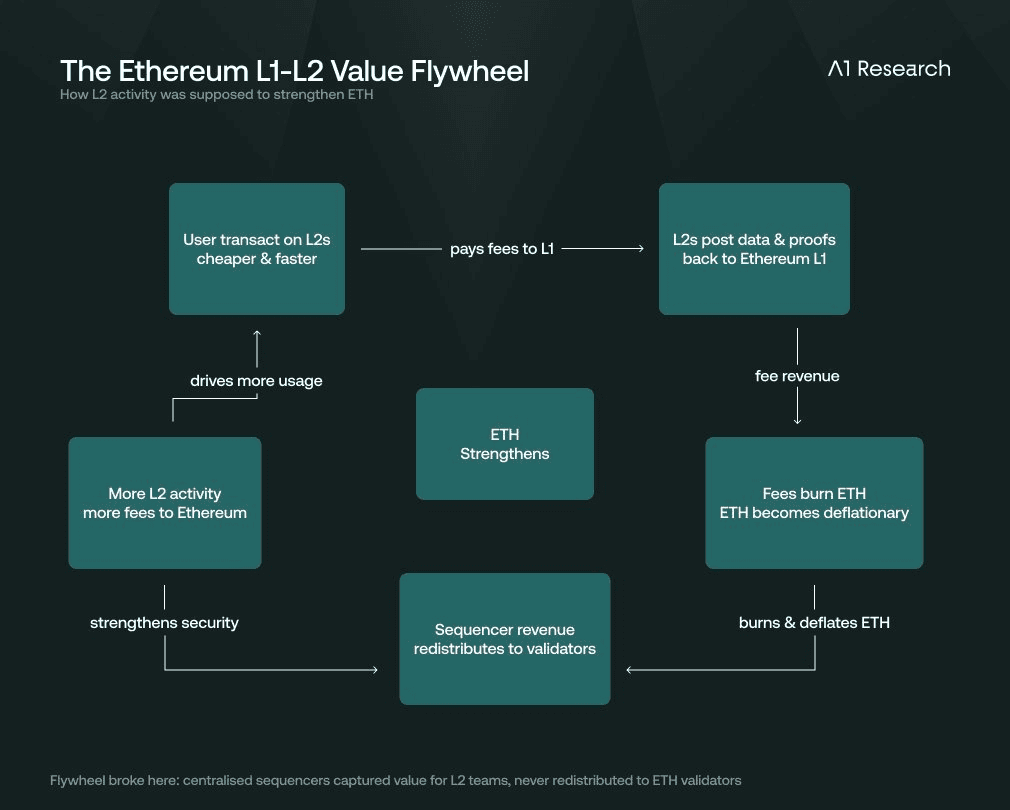

The rollup-centric roadmap was an economic model. The logic ran as follows:

Users transact on L2s; cheaper, faster

L2s post transaction data and proofs back to Ethereum L1, paying fees to do so

Those fees burn ETH, making ETH deflationary and accruing value to ETH holders

L2 sequencers, who order transactions, earn revenue but as L2s decentralised their sequencers, that revenue would redistribute toward validators and ultimately strengthen Ethereum's economic security

The more activity on L2s, the more fees flow to Ethereum, the stronger ETH becomes as an asset

This was the flywheel. L2 activity was supposed to translate into Ethereum value capture. The key words in that entire model are “supposed to”.

What Actually Happened: The Value Capture Problem

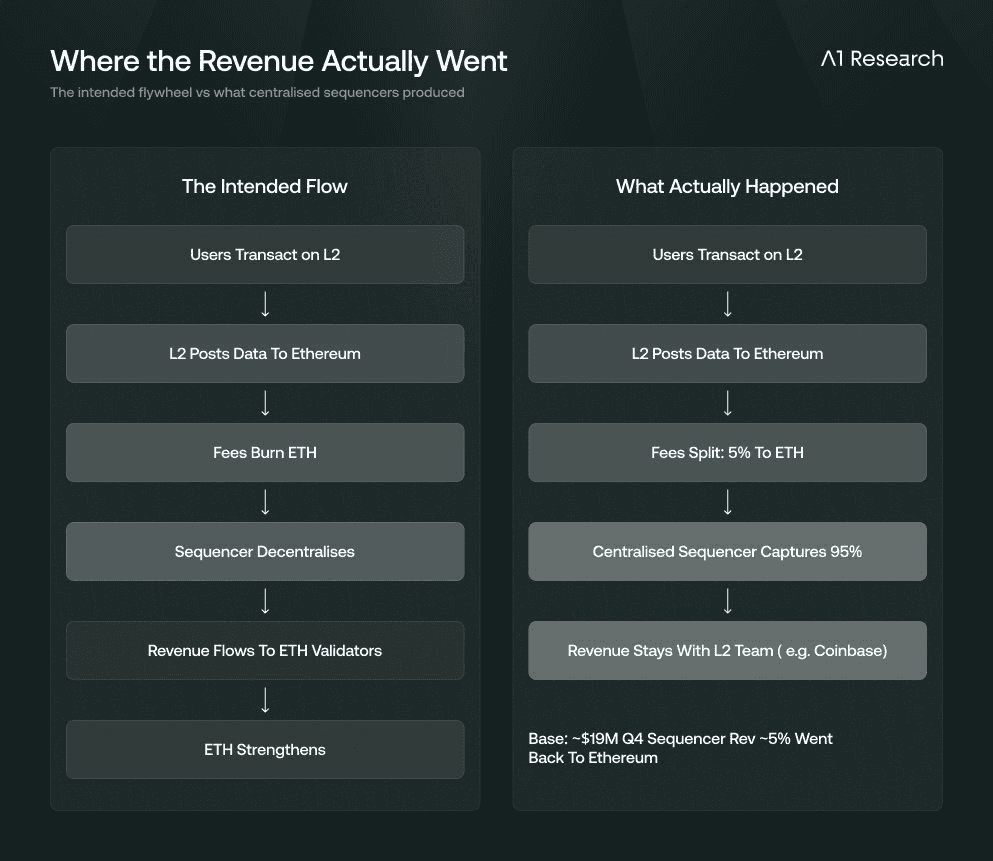

The flywheel broke at the sequencer. Every major L2 – Arbitrum, Base, Optimism, zkSync, etc. – operates a centralized sequencer. That sequencer is the entity that orders transactions on the L2, and it earns the revenue from doing so. In a centralized sequencer model, that revenue goes entirely to the L2 team.

The numbers make the scale of this visible:

Approximately 5% of Base's total revenue flows back to Ethereum through blob fees. From 2025 to 2026 Base generated $90M+ in revenue through the chain revenue itself

The remaining 95% stays with Coinbase, contributing just $4.9 million to the mainnet in blob fees out of $90M+generated revenue.

Priority fees on Base averaged $156,138 per day, approximately 86% of total daily revenue

In Q1 2025, L2 rollups processed nearly half of Ethereum's DEX volume while securing over $40B in assets, yet L1 daily gas revenue had already fallen from ~$23M at peak to ~$6.3M.

Ethereum provided the security. Ethereum provided credibility. Ethereum absorbed the reputational risk of being the settlement layer. And L2 sequencers captured the overwhelming majority of the transaction revenue that activity produced.

This is the actual betrayal the community was sensing not an ideological one, but an economic one. Ethereum became the infrastructure that made L2 businesses possible while those businesses captured the value.

Why Stage 2 Decentralisation Was the Specific Fix

This is the part of the debate that got almost entirely lost in the noise about alignment and ideology. Stage 2 decentralisation was not a philosophical goal. It was the specific mechanism that would have changed the value flow.

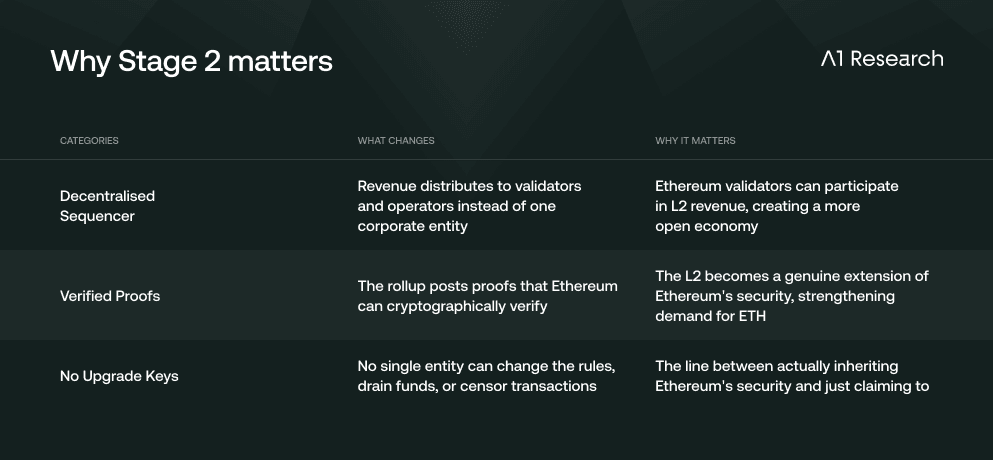

Here is what the stage progression actually means:

Stage 0: Fully centralised sequencer and upgrade keys; one entity controls everything, including the ability to rewrite the chain

Stage 1: Proof system live but a security council can override it; partial decentralisation with training wheels

Stage 2: Proof system fully trustless, no override possible, sequencer decentralised; the chain operates as a true extension of Ethereum's security guarantees

Stage 2 matters economically for Ethereum in three specific ways:

A Stage 2 rollup's sequencer is decentralised, meaning sequencer revenue is no longer captured by a single corporate entity. It distributes to validators and sequencer operators, creating a more open economic system where Ethereum's own validators can participate in capturing L2 revenue.

A Stage 2 rollup posts valid proofs to Ethereum that Ethereum can cryptographically verify making the L2 a genuine extension of Ethereum's security rather than a chain with a marketing relationship to Ethereum. This increases demand for ETH as the asset that backs that security, strengthening ETH's value proposition.

A Stage 2 removes the upgrade key, meaning no single entity can unilaterally change the L2's rules, drain user funds, or censor transactions. This is the difference between an L2 that genuinely inherits Ethereum's security properties and one that merely claims to.

Not a single economically important L2 reached Stage 2. The Block's 2026 analysis confirms decentralisation was treated as a long-term goal rather than an immediate priority throughout 2025. Astria, the most serious shared sequencer effort, shut down entirely. Most L2s continue to rely on trusted operators, upgrade keys, and closed infrastructure.

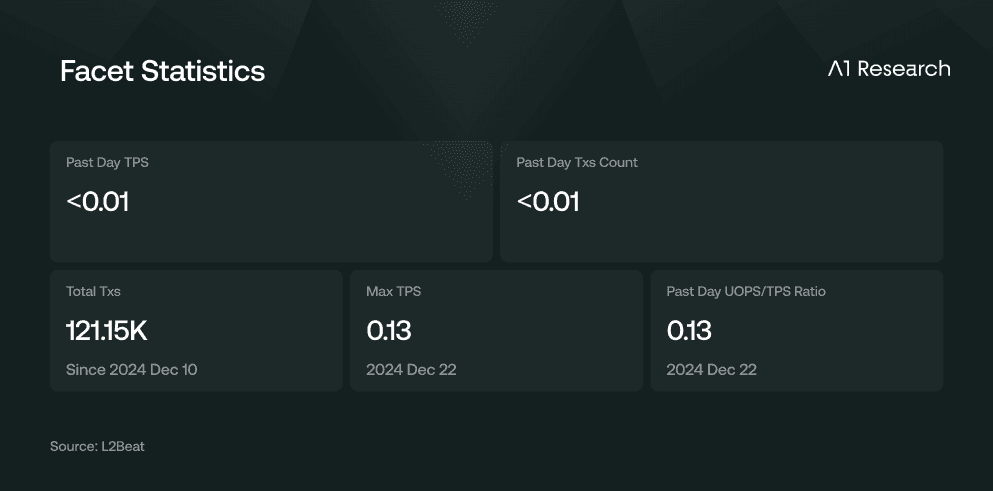

Facet became the first Stage 2 rollup – the only chain in the ecosystem to fully deliver what the community said it valued most. However, it has very few users, and therefore no significant impact on Ethereum.

Stage 2 was valuable to Ethereum. It was not valuable to L2 teams in the way that user growth, sequencer revenue, and token launches were valuable to them.

The Compounding Identity Crisis

The value capture problem had a second-order effect that compounded the damage. Every generic L2 that launched as "cheaper, faster Ethereum" absorbed activity that might otherwise have concentrated on L1 and with it, absorbed a portion of Ethereum's narrative identity.

The cumulative effect of dozens of generic EVM scaling chains was to make "just use Ethereum" seem unnecessary not because Ethereum had failed, but because Ethereum had been successfully replicated at lower cost by its own infrastructure layer. Ethereum became the backend of an ecosystem that users increasingly experienced through interfaces that had nothing to do with Ethereum.

Paramonov captures the identity crisis this produced precisely. Ethereum could not decide what its token was:

A commodity? complicated by dynamic supply changes and staking mechanisms

A tech stock? undermined by insufficient fee revenue

A store of value? the ultrasound money narrative lasted ~3 years before ETH inflation turned positive again in 2024

ETH was never designed to be Bitcoin. But the ultrasound money narrative tried to compete on that axis while ETH was simultaneously a gas asset, a staking asset, and a settlement layer. None of those framings was convincingly satisfied. And every generic L2 that diluted "what Ethereum is for" made answering that question harder.

The Category Error That Cost Three Years

The Ethereum community treated this as a moral failure and that category error made it nearly impossible to fix. L2 teams did not betray Ethereum. They responded rationally to the incentives in front of them:

Sequencer revenue was too valuable to surrender without a mechanism making it worthwhile

Token launches rewarded narrative over execution

The low cost of launching an "Ethereum-aligned" L2, combined with significant upside from token incentives, attracted a wave of opportunistic entrants with little long-term commitment to the ecosystem.

None of this required bad actors. It required a system where incentives pointed in directions the community did not want and then expressed outrage when people followed them.

The fix was always an incentive redesign. And the differentiation era, examined in the next two sections, is the first version of the L1-L2 relationship where the incentives are actually pointing in the right direction.

3. The L2s That Asked "What Can We Do That Ethereum Cannot?" Are the Ones That Matter Now

Vitalik's February 2026 post is being read as a critique of L2s. It is more accurately a selection mechanism.

The spectrum from "branded shards" obligated to return value to Ethereum through ideological loyalty, to a full range of chains at different levels of connection to Ethereum officially releases L2s from the social contract that was never working. In its place, a simpler and more durable question:

What do you do that Ethereum cannot?

The teams that were asking that question from the beginning, often dismissed as insufficiently aligned or too technically divergent, are the ones the data now validates. They cluster into four categories.

Category 1: Privacy-Native Execution

Ethereum's transparent architecture is one of its most important properties. Every transaction, every contract interaction, every wallet balance is publicly visible and independently verifiable. That transparency is foundational to Ethereum's trust model, it is what makes credible neutrality possible at scale.

It is also a structural limitation for an entire class of use cases the next era of blockchain adoption requires:

Financial institutions under regulatory frameworks cannot expose transaction details publicly

Enterprises building supply chain applications cannot broadcast proprietary data on a public ledger

Institutional trading desks cannot afford to have positions, counterparties, and strategies visible on-chain

These are not edge cases. They represent some of the largest potential markets for blockchain technology. These 2 chains also have the highest developer activities of all the L2s.

Aztec uses zero-knowledge proofs to enable private smart contract execution transaction details verifiable without being publicly visible. Fhenix is built on fully homomorphic encryption, enabling computation on encrypted data without ever decrypting it. Both represent computational models categorically unavailable on Ethereum L1 as its design deliberately prioritises transparency over privacy.

Starknet is building into the same space from its ZK-native architecture. Its Privacy Pool, a compliance-compatible privacy feature on Ekubo, is open-sourced and in final development. More concretely, Starknet is launching strkBTC in 2026: a Bitcoin-backed asset enabling shielded balances and confidential DeFi transfers, where transaction amounts and counterparties remain private while auditability is preserved.

The Starknet Foundation's VP of Growth has stated that privacy at the infrastructure level "removes a critical barrier to broader blockchain adoption" particularly for institutional capital that has remained hesitant to participate in public blockchain markets.

Vitalik explicitly validates this category in his post. As regulatory frameworks like MiCA in Europe and evolving SEC guidance in the United States push institutions toward confidential execution environments, privacy-native L2s become more valuable as L1 gets cheaper not less.

Category 2: Alternative Virtual Machines

The EVM is the most battle-tested smart contract execution environment in the industry. It is also a ceiling.

Writing smart contracts in Solidity excludes the overwhelming majority of the world's software developers – those working in Rust, C, C++, Python, and Go. The EVM's execution model limits certain classes of computation; specific application architectures, particularly those requiring different approaches to state management or provability, are simply not well served by EVM design.

Arbitrum's Stylus takes a complementary approach, extending rather than replacing the EVM. Rust, C, and C++ contracts now execute in a WebAssembly environment alongside Solidity on Arbitrum. The developer pool working in those languages dwarfs the Solidity community by orders of magnitude. Stylus opens the ecosystem to entirely different talent pools and existing software libraries deployable on-chain without rewriting in Solidity.

As Goldfeder argues: even infinite L1 scaling would not make these capabilities unnecessary. They serve developers and use cases the EVM structurally cannot reach.

Starknet + Cairo VM is trying to build a better machine from scratch. Starknet is powered by Cairo rather than the EVM, a deliberate choice because Cairo was designed from the ground up to maximize efficiency for STARK-based proving.

Its fundamentally different execution model optimized for ZK provability. The Starknet ecosystem grew 168% in projects in 2024, reaching 193 user-centric projects, with the gaming vertical alone seeing 47 new projects and 29 of them built on Dojo, a Cairo-native game engine.

Starknet is also positioning itself as the execution layer for Bitcoin, targeting a path from Bitcoin's current 13 TPS to thousands with over 1,700 BTC already staked on the network. But it has a tradeoff, Cairo has a steep learning curve, and the ecosystem is smaller. But it's a genuine technical bet. That earns it a place at the table.

Fluent is an Ethereum L2 that combines EVM, SVM, and Wasm into a single unified execution environment, allowing EVM, SVM, and Wasm smart contracts to be atomically composable and accessible through one wallet.

Calling a program in Solidity via a program written in Solana Rust happens in a single call, included in one transaction which requires no bridging and no shared sequencing. This lets developers leverage popular Solidity applications like Aave but also run more complex cryptography, agent orchestration systems, and even website frontends on-chain.

Category 3: Institutional Sovereignty

The third category receives the least technical attention in the ecosystem debate and the one that may have the largest near-term economic impact.

What institutions actually did in 2024–2025:

@RobinhoodApp → integrated @arbitrum for brokerage settlement rails

These decisions were not made on throughput calculations. They were made on sovereignty, the need for a dedicated execution environment that an institution controls, customises for its specific regulatory requirements, and evolves at its own pace without depending on the governance of a shared public chain.

Four institutional requirements Ethereum L1 cannot accommodate by design:

Compliance infrastructure: KYC/AML integration at protocol level is incompatible with Ethereum's permissionless design

Transaction reversibility: Real estate, securities, and legally complex instruments will require reversal mechanisms, Ethereum L1 transactions are immutable by design

Custom ordering policies: Regulated brokerages need environments that prevent specific forms of value extraction unacceptable in a regulated context

Brand and operational control: A regulated financial institution cannot accept the reputational risks of whatever else happens on a shared public chain

None of these requirements disappear as Ethereum L1 scales. They are sovereignty problems, not scaling problems.

Goldfeder's warning is pointed: if institutions on the fence between an Ethereum L2 and an independent L1 conclude the ecosystem does not want their kind of chain, they will not move to the Ethereum L1 – they will build independent L1s. In this scenario, Ethereum loses not just the rollup relationship, but the institutions entirely. Tempo is the most visible current example of that outcome.

Category 4: Extreme Performance

The conventional reading of Vitalik's post that L1 scaling makes L2 scaling redundant is empirically wrong at current and near-term trajectories.

Arbitrum and Base both exceeded 1,000 TPS during peak 2026 volatility

Ethereum L1 sat at 40 TPS during that time

MegaETH is targeting performance ceilings orders of magnitude beyond any L1 scaling roadmap. 100,000 TPS target, 10ms block times, sustained 35,000 TPS in stress tests processing 10.7 billion transactions in a week (more than Ethereum's entire 10-year history).

Base's gigagas target: 1 gigagas/second – processing the entire current Ethereum L1 throughput every few seconds

Gaming studios like Atari, Lotte Group, Nexon, and Sky Mavis have adopted app-specific chains for use cases that cannot operate within L1 constraints

Extreme performance L2s are not doing what L1 does faster. They are enabling application categories including fully on-chain games, high-frequency on-chain order books, real-time settlement that do not exist at lower throughput levels.

Base's departure from the OP Stack is the clearest signal that even the most commercially successful generic L2 has concluded that extreme performance rather than alignment credentials is the differentiator worth building around. The six hardforks per year target, 99.99% non-empty block reliability, and gigagas throughput ambition are not incremental improvements. They are the construction of a genuinely distinct identity around what Base can do that Ethereum L1 cannot.

The data behind this trajectory is now substantial:

$369.9M in ecosystem app revenue in 2025 – 30x growth year-over-year, leading all L2 networks

9.3M Coinbase monthly active trading users – a captive distribution channel no other L2 can replicate

$866.3M in loans applied for through Coinbase via Morpho on Base; Morpho's TVL on Base is up 1,906% year-to-date

Q4 2025 gross sequencer revenue: ~$19M ($15M net after L1 data costs and OP Collective share)

Coinbase holds $6B+ in cash and generated $2.8B in subscription and services revenue in 2025

Source: Base 2025 Report, December 2025; Coinbase Q4 2025 Earnings Outlook;Coinbase 2026 Research, March 2026

That last data point matters specifically. Coinbase is legally obligated to maximise shareholder returns. At Base's current sequencer revenue trajectory, the case for continuing to pay Ethereum's blob fees weakens every quarter. The balance sheet to fund an independent security model exists. Wall Street analysts are already pricing Base's sequencer economics into COIN valuations.

J.P. Morgann and Goldman Sachs recently upgraded COIN to Buy, in part due to Base Network Effects.

None of this means Base will become an L1. But the option is now credible in a way it was not two years ago. And the framing of Base leaving the OP Stack as "fragmentation" misreads what is actually happening: the most commercially successful generic L2 is finally building an identity around what it uniquely can do and that identity has almost nothing to do with scaling Ethereum as the rollup-centric roadmap originally conceived it.

What These Four Categories Share

Privacy chains, alternative VM chains, institutional sovereignty chains, and extreme performance chains share one property that distinguishes them from the generic L2s of the extraction era:

They all have a credible answer to the question Vitalik is now explicitly asking: what do you do that Ethereum cannot?

The L2s that cannot answer that question are generic EVM scaling chains whose entire value proposition was cheaper execution of the same transactions Ethereum processes. These networks face existential pressure as L1 fees fall, L1 throughput increases, and the native rollup precompile makes EVM verification a native Ethereum function available to any L2 for free.

That selection pressure is not Ethereum becoming hostile to L2s. It is Ethereum becoming strong enough that the weakest reason to build an L2 is cheaper EVM execution which no longer justifies an independent chain's existence.

4. What the L1-L2 Relationship Actually Looks Like Now

On February 17, 2026, the Ethereum Foundation announced the formation of a new Platform team with a single mandate: to unify L1 and L2 into a coherent platform. The stated goal was to "deliver the strongest possible Ethereum platform, where L1 and L2s are best positioned to support users, apps, and all organisations building on Ethereum."

The announcement received far less attention than Vitalik's post two weeks earlier. It deserved more.The Ethereum Foundation is catching up organisationally to a structural reality the market had already priced in.

The alignment debate is over.

The initial question was, “are L2s sufficiently loyal to Ethereum?”

But this has been replaced by a more productive one, “how do L1 and L2s together build the strongest possible platform?”

The Technical Mechanism: Native Rollup Precompile

The most consequential proposal in Vitalik's post is the native rollup precompile, a mechanism that would verify ZK-EVM proofs as a native Ethereum function, auto-upgrading with Ethereum and covered by hard-fork remediation if bugs emerge.

Its structural effect is a selection mechanism. For generic EVM L2s, it evaporates their primary technical moat. If Ethereum verifies EVM execution natively and for free, cheaper EVM transactions alone no longer justify an independent chain's existence. For differentiated L2s, it is unambiguously positive. Vitalik's design principle is explicit: if an L2 is "EVM plus other stuff," Ethereum verifies the EVM portion for free, and the L2 only proves its differentiated layer. Aztec's privacy system, Starknet's CairoVM, and Arbitrum's Stylus contracts are examples of the "other stuff" that survives and strengthens.

The precompile also enables synchronous composability between rollups – atomic transactions across different L2s as if on the same chain – laying the technical foundation for a unified Ethereum that finally feels like one ecosystem.

The Economic Logic

Ethereum's value as a settlement layer does not derive primarily from fee revenue. It derives from the scale and trustworthiness of the economic activity that settles on it. Every differentiated L2 that builds a genuinely valuable application increases the total economic surface area Ethereum secures worth considerably more than the marginal blob fees any individual L2 pays.

The numbers reflect this. Ethereum holds $165 billion in stablecoin issuance and $55 billion in DeFi TVL outpacing Solana at $6.76 billion by a factor of seven. Monthly transactions hit all-time highs of 50 million-plus in 2025 even as fees fell to multi-cycle lows while usage was at all-time highs, a settlement layer whose infrastructure costs are falling while demand grows.

L2s that settle on Ethereum inherit proximity to that trust from day one. Independent L1s do not. That cost differential grows over time rather than shrinking. Ethereum's security budget scales with staked value while L2 sequencer costs remain relatively fixed. The economic incentive for differentiated L2s to remain anchored to Ethereum strengthens as the ecosystem matures rather than weakens.

Three Eras, One Coherent Story

The relationship makes most sense as three distinct eras. 1. The bootstrap era (2020 to 2023) was an asymmetric deal, correct for its moment, that produced the ecosystem whose numbers define this piece. 2. The extraction era (2023 to 2025) exposed the incentive misalignments that a social contract without enforcement mechanisms always produces. 3. The differentiation era (2026 and onwards) beginning now is the first version of the relationship where the incentives of every major participant point in the same direction.

Ethereum wants differentiated L2s that expand what the ecosystem can do. Differentiated L2s want Ethereum's security and liquidity. Institutions want dedicated execution environments on Ethereum rails and the enterprise rollup trend confirms they are building them. Generic L2s face a structural choice between finding genuine differentiation or accepting that they are operating in a category the market is exiting.

The Block's 2025 data shows the selection already operating activity concentrated around a small set of ecosystems with genuine differentiation while most new launches became ghost towns after incentive cycles ended.

The Winner-Takes-Most Dynamic Is Already Playing Out

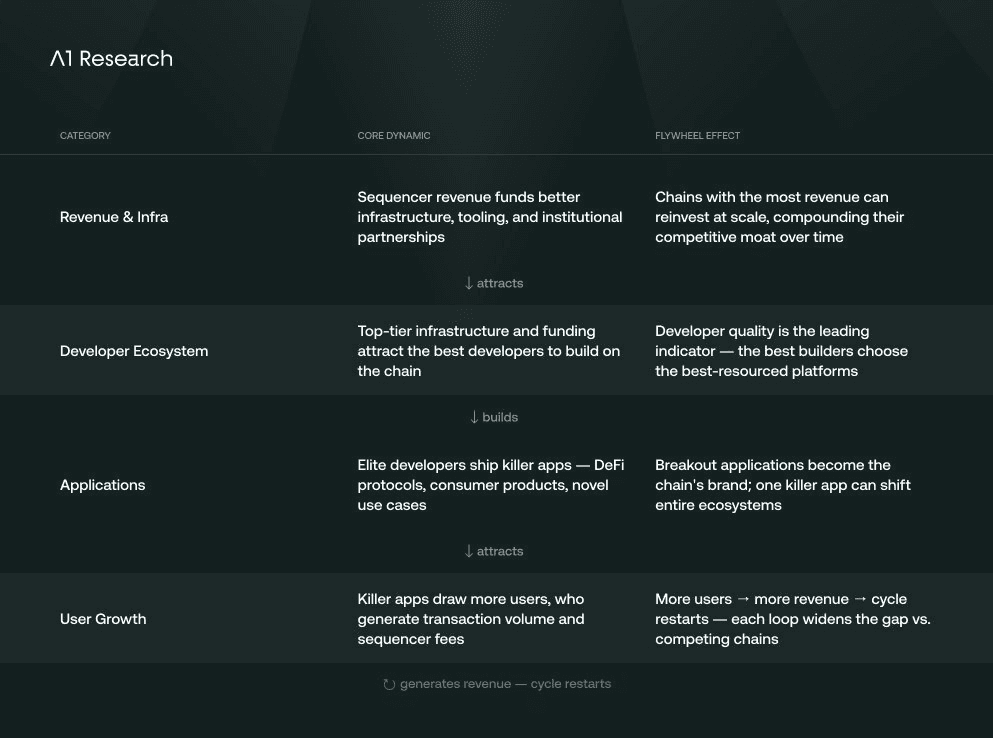

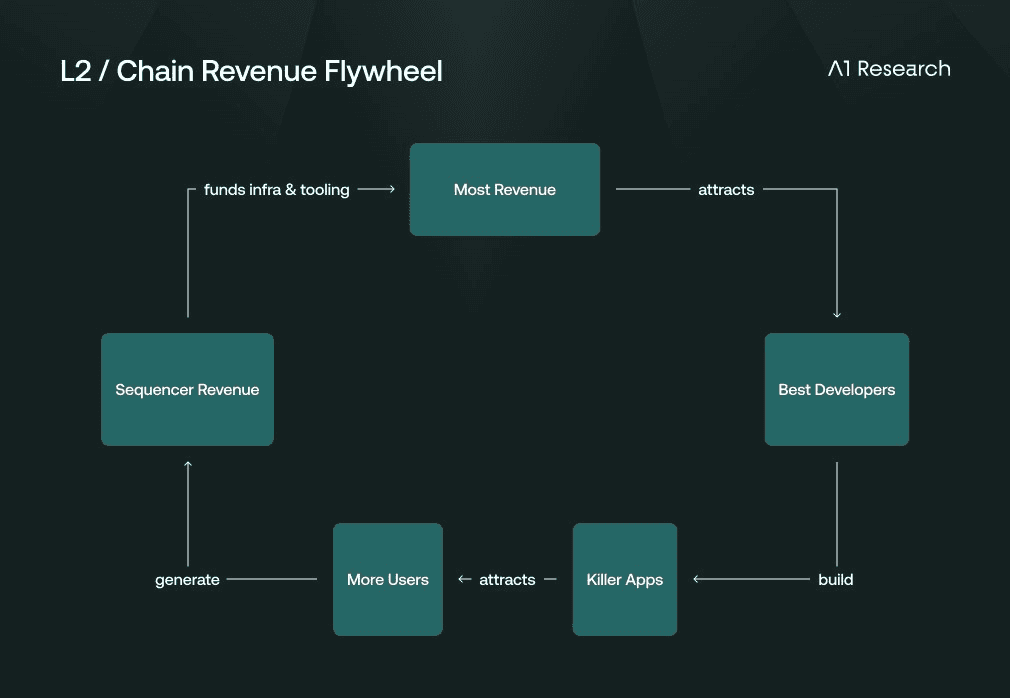

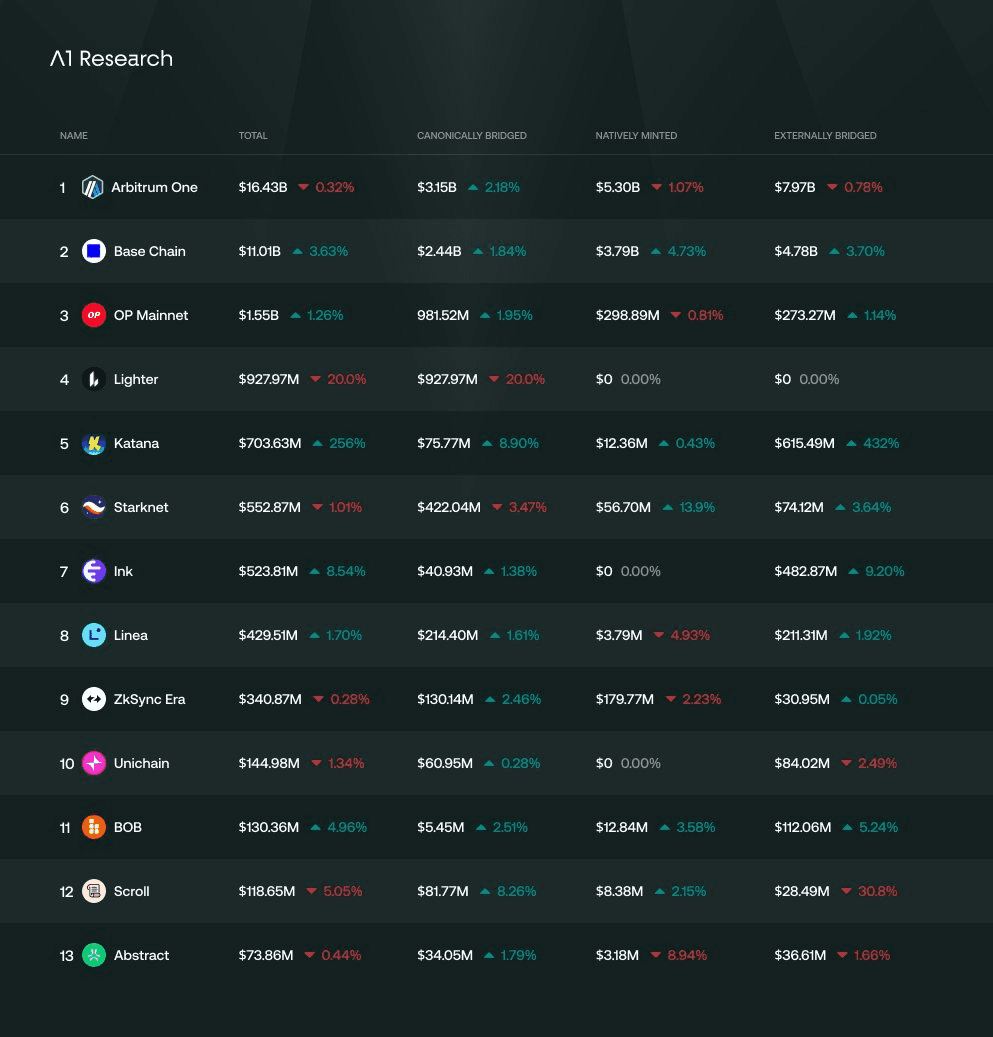

The L2Beat data makes the consolidation trend hard to ignore. Arbitrum One holds $16.43B in total bridged value. Base Chain holds $11.08B. Together they account for roughly 75% of all L2 TVL across the top 13 chains and the gap to the next tier is not incremental. OP Mainnet sits at $1.55B, nearly an order of magnitude behind, while chains like Scroll ($118M) and Abstract ($73M) are competing in a different category entirely.

This distribution reflects the compounding logic of L2 network effects. The chains with the most revenue attract the best developers. The best developers build the killer apps. Killer apps attract more users. More users generate more sequencer revenue. More revenue funds better infrastructure, tooling, and institutional partnerships.

The cycle reinforces itself every quarter. The leaders from the flywheel are already visible in the data:

Arbitrum One: deepest DeFi liquidity, strongest developer ecosystem, Stylus opening the chain to Rust/C++ developers

Base: $369.9M in ecosystem app revenue in 2025, Aerodrome generating $160.5M alone, 9.3M Coinbase users as a captive distribution moat

Starknet: $47.2M annualised fees, $130M in bridged BTC, growing BTCFi and privacy use cases that competitors cannot easily replicate

The challenge for newer entrants is more about the switching costs growing higher every quarter than competing on TVL; liquidity depth on Arbitrum took years to build. The developer relationships, audited protocol deployments, and institutional integrations that make Base's DeFi ecosystem function are not replicable with an incentive programme. Katana's 256% TVL growth and Ink's $523M are genuine signals that niche momentum is still possible. But for any new general-purpose L2, the relevant question is no longer whether it can attract users. It is whether it can attract users away from ecosystems where every month of inactivity widens the gap further.

The chains that survived the extraction era and built genuine differentiation do not just have a head start. They have structural advantages in revenue, tooling, liquidity, and talent that become self-reinforcing. The window for catching them is narrowing.

Conclusion

The path forward was always hiding in plain sight, it was in the incentives. The early bootstrap phase did what it needed to do: it pulled people in, kickstarted activity, and built the foundation. Then came the extraction phase, where the cracks started to show and misaligned incentives became harder to ignore. What we are moving into now is a phase of real differentiation where both the tech and the economics push builders toward creating something meaningfully distinct, not just because they believe in it, but because it actually makes sense.

Ethereum needs chains that expand its surface area doing the things it can’t do itself, while still relying on it for what it does best. That’s where the next wave comes from: privacy-focused chains, alternative VM ecosystems, sovereign institutional chains, ultra-high-performance systems. They don’t matter because they are loyal, they matter because they are useful.

And maybe that’s the point, all the noise, all the hype cycles, it had to play out. Now that it has, what’s left is clearer, the signal was always there.

Disclaimer: This analyst take is produced by A1 Research for informational purposes only. It does not constitute financial advice or an endorsement of any project, token, or protocol mentioned herein.

Recommended Articles

Dive into 'Narratives' that will be important in the next year

" height="53.254000000000005px" id="poHfazHFu" transform="translate(192 19.5)" width="54.447px"/><path d="M 17.077 0 C 20.225 0 23.038 0.665 25.515 1.994 C 28.06 3.324 30.036 5.153 31.442 7.48 C 32.916 9.74 33.652 12.233 33.652 14.96 L 25.114 14.96 C 25.114 12.832 24.344 11.036 22.804 9.573 C 21.263 8.111 19.354 7.38 17.077 7.38 C 14.867 7.38 12.992 8.045 11.452 9.374 C 9.979 10.637 9.242 12.234 9.242 14.161 C 9.242 16.289 10.112 18.051 11.853 19.446 C 13.662 20.843 16.207 21.973 19.488 22.837 C 24.176 24.034 27.826 25.863 30.437 28.322 C 33.049 30.782 34.355 34.007 34.355 37.996 C 34.355 41.054 33.585 43.746 32.045 46.073 C 30.571 48.333 28.53 50.096 25.918 51.36 C 23.306 52.623 20.392 53.254 17.178 53.254 C 13.963 53.254 11.05 52.555 8.438 51.159 C 5.827 49.763 3.75 47.902 2.21 45.575 C 0.736 43.182 0 40.522 0 37.597 L 8.539 37.597 C 8.539 39.924 9.376 41.885 11.05 43.481 C 12.724 45.076 14.8 45.874 17.278 45.874 C 19.622 45.874 21.598 45.209 23.205 43.88 C 24.879 42.484 25.717 40.755 25.717 38.694 C 25.717 36.5 24.845 34.704 23.104 33.309 C 21.363 31.846 18.818 30.683 15.47 29.819 C 10.916 28.689 7.3 26.926 4.621 24.532 C 2.009 22.139 0.703 18.815 0.703 14.56 C 0.703 11.635 1.406 9.075 2.812 6.881 C 4.286 4.687 6.261 2.991 8.739 1.795 C 11.284 0.598 14.063 0 17.077 0 Z" fill="rgb(255, 255, 255)" height="53.25400000000002px" id="dwV_m7WwK" transform="translate(254.5 19.5)" width="34.35500000000002px"/><path d="M 27.223 0 C 32.313 0 36.934 1.163 41.086 3.49 C 45.238 5.817 48.486 9.009 50.83 13.064 C 53.241 17.12 54.447 21.641 54.447 26.627 C 54.447 27.957 54.347 29.12 54.146 30.117 L 8.81 30.117 C 9.154 32.32 9.878 34.446 10.95 36.401 C 12.557 39.259 14.767 41.52 17.579 43.181 C 20.459 44.844 23.674 45.675 27.223 45.675 C 31.107 45.675 34.557 44.778 37.571 42.982 C 40.651 41.187 42.895 38.794 44.301 35.802 L 53.342 35.802 C 51.467 41.054 48.185 45.276 43.497 48.467 C 38.809 51.658 33.384 53.254 27.223 53.254 C 22.133 53.254 17.513 52.091 13.361 49.764 C 9.209 47.437 5.927 44.245 3.516 40.189 C 1.172 36.134 0 31.613 0 26.627 C 0 21.641 1.172 17.12 3.516 13.064 C 5.927 9.009 9.209 5.817 13.361 3.49 C 17.513 1.164 22.133 0 27.223 0 Z M 27.223 7.58 C 23.674 7.58 20.459 8.41 17.579 10.072 C 14.767 11.734 12.557 14.028 10.95 16.953 C 9.958 18.722 9.265 20.643 8.898 22.638 L 45.545 22.638 C 45.137 20.485 44.341 18.424 43.196 16.555 C 41.588 13.762 39.378 11.568 36.566 9.973 C 33.753 8.377 30.638 7.579 27.223 7.579 Z M 103.691 44.578 L 110.522 44.578 L 110.522 52.058 L 96.257 52.058 L 96.257 45.427 C 94.611 47.805 92.401 49.683 89.627 51.06 C 86.748 52.522 83.533 53.254 79.984 53.254 C 76.501 53.254 73.353 52.522 70.54 51.06 C 67.795 49.53 65.585 47.503 63.91 44.977 C 62.303 42.45 61.499 39.592 61.499 36.401 C 61.499 33.209 62.303 30.35 63.91 27.823 C 65.518 25.231 67.728 23.203 70.54 21.74 C 73.353 20.278 76.501 19.546 79.984 19.546 L 95.453 19.546 L 95.453 9.076 L 64.915 9.076 L 64.915 1.196 L 103.691 1.196 Z M 80.888 26.926 C 78.879 26.926 77.037 27.359 75.363 28.223 C 73.688 29.021 72.382 30.151 71.445 31.613 C 70.507 33.009 70.038 34.605 70.038 36.401 C 70.038 38.129 70.507 39.724 71.445 41.187 C 72.382 42.649 73.688 43.814 75.363 44.677 C 77.037 45.476 78.879 45.874 80.888 45.874 C 83.768 45.874 86.279 45.443 88.422 44.578 C 90.632 43.648 92.34 42.417 93.545 40.888 C 94.818 39.292 95.453 37.463 95.453 35.402 L 95.453 26.926 Z" fill="rgb(255, 255, 255)" height="53.254000000000005px" id="J9sNA1zvT" transform="translate(296.5 19.5)" width="110.52200054931643px"/><path d="M 472.484 17.603 C 476.837 17.603 480.856 18.467 484.539 20.196 C 488.222 21.858 491.302 24.218 493.78 27.276 C 496.325 30.334 498.034 33.792 498.904 37.648 L 490.164 37.648 C 488.825 33.991 486.581 31.066 483.434 28.872 C 480.286 26.678 476.636 25.581 472.484 25.581 C 469.002 25.581 465.82 26.411 462.94 28.074 C 460.128 29.669 457.884 31.897 456.21 34.755 C 454.603 37.615 453.8 40.773 453.8 44.23 C 453.8 47.687 454.603 50.845 456.21 53.704 C 457.884 56.562 460.128 58.824 462.94 60.486 C 465.82 62.082 469.002 62.879 472.484 62.879 C 476.636 62.879 480.286 61.781 483.434 59.587 C 486.581 57.393 488.825 54.469 490.164 50.812 L 498.904 50.812 C 498.034 54.668 496.325 58.125 493.78 61.183 C 491.302 64.241 488.222 66.635 484.539 68.363 C 480.856 70.027 476.837 70.857 472.484 70.857 C 467.395 70.857 462.773 69.694 458.621 67.367 C 454.469 65.04 451.187 61.848 448.776 57.792 C 446.433 53.737 445.261 49.216 445.261 44.23 C 445.261 39.244 446.433 34.723 448.776 30.667 C 451.187 26.612 454.469 23.42 458.621 21.093 C 462.773 18.766 467.395 17.603 472.484 17.603 Z M 68.395 70.021 L 58.566 70.021 L 34.197 10.609 L 9.83 70.021 L 0 70.021 L 28.873 0 L 39.522 0 Z M 96.18 70.021 L 87.443 70.021 L 87.443 10.047 L 71.775 10.047 L 71.775 0 L 96.181 0 L 96.181 70.021 Z" fill="rgb(255, 255, 255)" height="70.85700064086915px" id="XyVzovWZk" transform="translate(0 2)" width="498.90398632812503px"/><path d="M 22.401 0 C 26.419 0 30.036 0.93 33.251 2.792 C 36.532 4.587 39.11 7.081 40.985 10.272 C 42.86 13.396 43.799 16.92 43.799 20.843 C 43.799 24.699 42.86 28.189 40.985 31.313 C 39.11 34.372 36.566 36.799 33.351 38.593 C 31.265 39.754 28.996 40.549 26.642 40.943 L 45.205 68.812 L 34.557 68.812 L 16.616 41.286 L 8.84 41.286 L 8.84 68.812 L 0 68.812 L 0 0 Z M 8.84 33.608 L 22.2 33.608 C 24.544 33.608 26.688 33.076 28.63 32.012 C 30.572 30.882 32.079 29.352 33.15 27.425 C 34.222 25.497 34.758 23.336 34.758 20.943 C 34.758 18.549 34.222 16.388 33.15 14.46 C 32.079 12.532 30.572 11.003 28.63 9.873 C 26.688 8.743 24.544 8.177 22.2 8.177 L 8.84 8.177 Z" fill="rgb(255, 255, 255)" height="68.812px" id="tX8m5fMcV" transform="translate(141 3)" width="45.20500000000001px"/><path d="M 25.215 28.622 C 21.732 28.622 18.685 29.352 16.073 30.815 C 13.528 32.278 11.586 34.34 10.247 36.999 C 8.908 39.592 8.237 42.65 8.237 46.174 L 8.237 71.804 L 0 71.804 L 0 20.942 L 8.237 20.942 L 8.237 30.4 C 10.035 27.253 12.277 24.798 14.969 23.037 C 17.982 21.109 21.397 20.145 25.215 20.145 Z M 102.415 29.563 C 104.366 26.491 106.844 24.116 109.848 22.439 C 113.13 20.643 116.88 19.746 121.099 19.746 C 125.185 19.746 128.801 20.61 131.948 22.339 C 135.163 24.001 137.64 26.428 139.382 29.619 C 141.123 32.744 141.994 36.367 141.994 40.489 L 141.994 71.804 L 133.757 71.804 L 133.757 42.982 C 133.757 38.395 132.351 34.705 129.538 31.912 C 126.792 29.12 123.108 27.724 118.487 27.724 C 115.273 27.724 112.427 28.356 109.949 29.619 C 107.538 30.882 105.663 32.71 104.323 35.103 C 103.051 37.431 102.415 40.123 102.415 43.182 L 102.415 71.804 L 94.178 71.804 L 94.178 0 L 102.415 0 Z" fill="rgb(255, 255, 255)" height="71.80400045776368px" id="YoO0zKl7f" transform="translate(416 0)" width="141.99400140380868px"/></g><g d="M 8.96 4.214 C 9.786 4.214 10.48 4.51 11.042 5.107 C 11.637 5.668 11.936 6.362 11.936 7.189 C 11.936 8.014 11.637 8.725 11.042 9.32 C 10.749 9.613 10.42 9.826 10.055 9.967 L 12.183 13.732 L 10.4 13.732 L 8.453 10.162 L 7.471 10.162 L 7.471 13.734 L 5.884 13.734 L 5.884 4.212 L 8.959 4.212 Z M 7.473 8.725 L 8.86 8.725 C 9.29 8.725 9.638 8.592 9.902 8.328 C 10.201 8.026 10.362 7.614 10.347 7.189 C 10.356 6.779 10.196 6.384 9.904 6.097 C 9.64 5.8 9.258 5.636 8.861 5.651 L 7.473 5.651 Z M 9.026 0 C 10.712 0 12.234 0.396 13.587 1.189 C 14.952 1.926 16.072 3.046 16.81 4.412 C 17.603 5.769 18 7.29 18 8.975 C 18 10.693 17.603 12.23 16.81 13.584 C 16.053 14.937 14.938 16.053 13.587 16.809 C 12.232 17.601 10.712 18 9.026 18 C 7.308 18 5.753 17.618 4.366 16.858 C 3.03 16.084 1.919 14.973 1.143 13.636 C 0.382 12.248 0.002 10.693 0 8.975 C 0 7.29 0.382 5.769 1.143 4.412 C 1.9 3.061 3.015 1.945 4.366 1.189 C 5.753 0.398 7.308 0 9.026 0 Z M 9.026 1.638 C 7.72 1.624 6.435 1.967 5.307 2.628 C 4.216 3.257 3.309 4.164 2.68 5.256 C 2.051 6.379 1.738 7.635 1.738 9.024 C 1.738 10.38 2.051 11.618 2.68 12.742 C 3.328 13.82 4.23 14.722 5.307 15.37 C 6.432 15.999 7.671 16.314 9.026 16.314 C 10.381 16.314 11.605 15.999 12.696 15.37 C 13.766 14.73 14.653 13.825 15.273 12.742 C 15.934 11.618 16.265 10.363 16.265 8.975 C 16.278 7.667 15.935 6.381 15.273 5.255 C 14.662 4.148 13.75 3.237 12.644 2.627 C 11.553 1.967 10.3 1.625 9.026 1.639 Z" fill="transparent" height="18px" id="fDqcVjis4" transform="translate(571 0)" width="18px"><path d="M 3.076 0.002 C 3.902 0.002 4.596 0.298 5.158 0.895 C 5.753 1.456 6.052 2.15 6.052 2.977 C 6.052 3.803 5.753 4.513 5.158 5.108 C 4.865 5.401 4.536 5.614 4.171 5.755 L 6.299 9.521 L 4.516 9.521 L 2.569 5.951 L 1.587 5.951 L 1.587 9.522 L 0 9.522 L 0 0 L 3.075 0 Z M 1.589 4.513 L 2.976 4.513 C 3.406 4.513 3.754 4.38 4.018 4.116 C 4.317 3.814 4.478 3.402 4.463 2.977 C 4.472 2.567 4.312 2.172 4.02 1.885 C 3.756 1.588 3.374 1.424 2.977 1.439 L 1.589 1.439 Z" fill="rgb(255, 255, 255)" height="9.522276301010859px" id="YcHNItJFD" transform="translate(5.884 4.212)" width="6.299243485570059px"/><path d="M 9.026 0 C 10.712 0 12.234 0.396 13.587 1.189 C 14.952 1.926 16.072 3.046 16.81 4.412 C 17.603 5.769 18 7.29 18 8.975 C 18 10.693 17.603 12.23 16.81 13.584 C 16.053 14.937 14.938 16.053 13.587 16.809 C 12.232 17.601 10.712 18 9.026 18 C 7.308 18 5.753 17.618 4.366 16.858 C 3.03 16.084 1.919 14.973 1.143 13.636 C 0.382 12.248 0.002 10.693 0 8.975 C 0 7.29 0.382 5.769 1.143 4.412 C 1.9 3.061 3.015 1.945 4.366 1.189 C 5.753 0.398 7.308 0 9.026 0 Z M 9.026 1.638 C 7.72 1.624 6.435 1.967 5.307 2.628 C 4.216 3.257 3.309 4.164 2.68 5.256 C 2.051 6.379 1.738 7.635 1.738 9.024 C 1.738 10.38 2.051 11.618 2.68 12.742 C 3.328 13.82 4.23 14.722 5.307 15.37 C 6.432 15.999 7.671 16.314 9.026 16.314 C 10.381 16.314 11.605 15.999 12.696 15.37 C 13.766 14.73 14.653 13.825 15.273 12.742 C 15.934 11.618 16.265 10.363 16.265 8.975 C 16.278 7.667 15.935 6.381 15.273 5.255 C 14.662 4.148 13.75 3.237 12.644 2.627 C 11.553 1.967 10.3 1.625 9.026 1.639 Z" fill="rgb(255, 255, 255)" height="18px" id="VlQ3a59vB" width="18px"/></g></svg>)